MAGIC SOFTWARE ENTERPRISES (NASDAQ:MGIC) was identified as a potential quality investment through our Caviar Cruise stock screener. The company demonstrates strong profitability, efficient capital allocation, and solid financial health, making it an interesting candidate for long-term investors. Below, we examine why MGIC fits the criteria of a quality stock.

Key Strengths of MGIC

- High Return on Invested Capital (ROIC) – MGIC’s ROIC (excluding cash and goodwill) stands at 32.29%, well above the 15% threshold for quality stocks. This indicates the company efficiently generates profits from its capital investments.

- Strong EBIT Growth – Over the past five years, MGIC has delivered an annual EBIT growth rate of 12.60%, exceeding the 5% minimum requirement. This suggests improving operational efficiency.

- Low Debt Burden – The company’s debt-to-free cash flow ratio is 1.21, meaning it could repay all its debt in just over a year using current cash flows. This reflects a conservative balance sheet.

- Exceptional Profit Quality – MGIC’s five-year average profit quality (free cash flow to net income) is 160.05%, far surpassing the 75% benchmark. This indicates strong cash conversion from reported earnings.

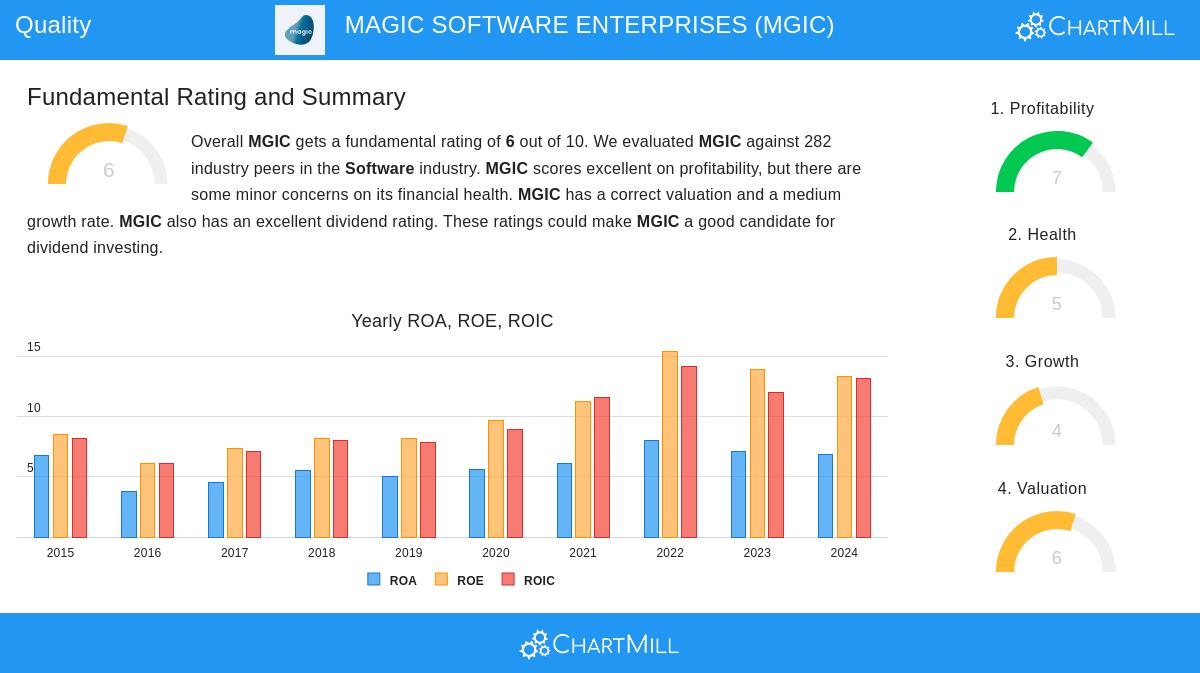

Fundamental Analysis Summary

Our fundamental report assigns MGIC a score of 6 out of 10, with notable strengths in profitability and dividends. Key takeaways:

- Profitability – The company outperforms most peers in ROIC (90.78% percentile) and operating margin (77.66% percentile).

- Dividend – MGIC offers a 4.25% dividend yield, higher than both industry and S&P 500 averages.

- Valuation – The stock appears reasonably priced, with a P/E ratio of 15.74, below industry and market averages.

- Growth – While past revenue growth has been steady (11.18% CAGR), future revenue growth is expected to moderate to 7.16% annually.

Why Quality Investors Should Take Note

MGIC meets several hallmarks of a quality investment: consistent profitability, high returns on capital, and a manageable debt load. Its ability to convert earnings into cash efficiently further supports its appeal. While growth may slow slightly, the company’s strong fundamentals and attractive dividend make it a candidate for further research.

For more quality stock ideas, explore our Caviar Cruise screener.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should always conduct your own analysis before making investment decisions.