Value investing focuses on finding stocks priced below their true worth while having solid financial foundations. This approach, based on Benjamin Graham’s ideas, targets firms with steady profits, sound finances, and room for growth, but trading at a discount because of short-term market imbalances. Lantheus Holdings Inc (NASDAQ:LNTH) stands out as a potential fit for this method, performing well in ChartMill’s fundamental review.

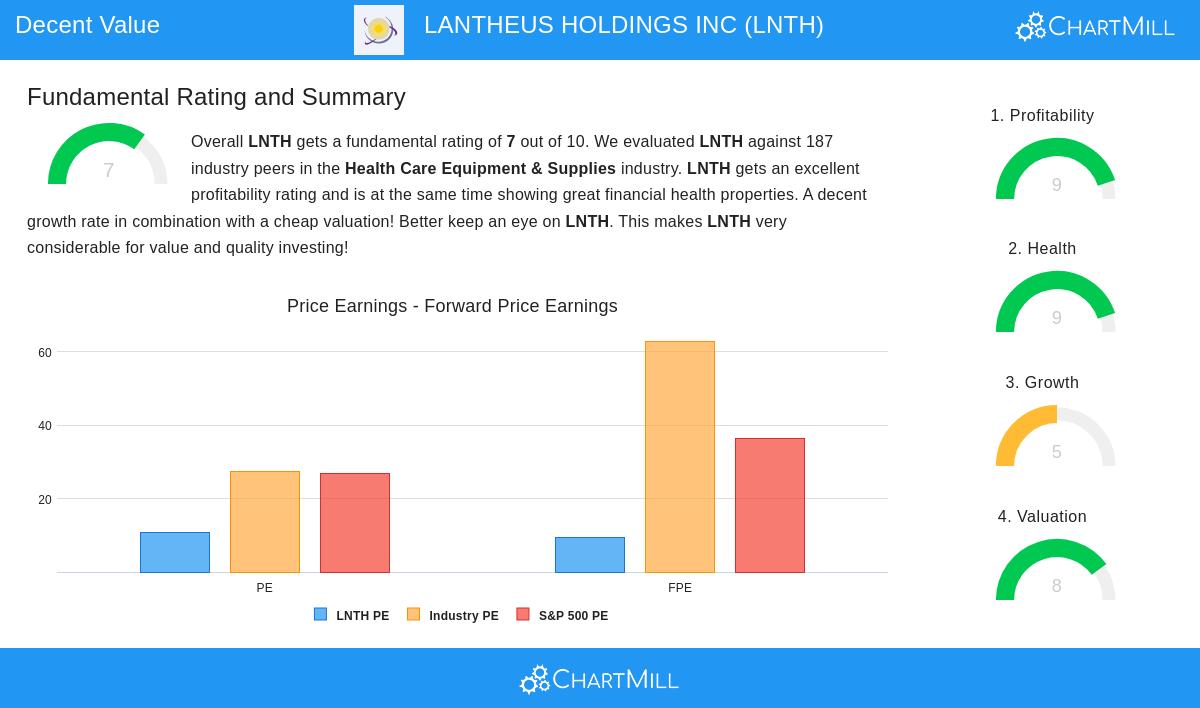

Valuation: An Attractive Opportunity

Lantheus’ valuation numbers suggest it may be priced lower than similar companies and major market benchmarks:

- Price/Earnings (P/E) Ratio: At 10.66, LNTH is much cheaper than the S&P 500 average (26.82) and its industry peers (27.26). This makes it more affordable than 92% of Health Care Equipment & Supplies sector stocks.

- Forward P/E: The ratio of 9.34 adds to its appeal, sitting below the sector’s forward average of 62.86.

- Enterprise Value/EBITDA and Price/FCF: Both ratios show LNTH is priced well, doing better than 92% and 95% of industry peers, respectively.

For value investors, these figures suggest a safety net—a key part of Graham’s strategy. The gap between price and true value might point to market neglect, especially given the company’s strong financials.

Financial Health: A Stable Foundation

LNTH’s financial strength is notable, with a Health Rating of 9/10:

- Liquidity: Current and Quick Ratios of 5.74 and 5.46 show it can easily cover short-term debts, ranking in the top 20% of the industry.

- Solvency: A Debt-to-Equity ratio of 0.49 and Debt/FCF of 1.2 reflect careful borrowing. The Altman-Z score of 5.80 (higher than 81% of peers) further lowers bankruptcy risk.

Solid financial metrics reduce potential losses, matching value investing’s emphasis on protecting capital.

Profitability: Strong Earnings

With a Profitability Rating of 9/10, LNTH shows impressive earnings:

- Margins: Operating Margin (29.3%) and Profit Margin (16.55%) rank in the top 7% and 6% of the industry, respectively.

- Returns: ROIC (18.93%) and ROE (21.85%) beat over 96% and 93% of peers, showing efficient use of capital.

Consistent cash flow and better margins point to lasting advantages—a priority for value investors looking for stable businesses.

Growth: Consistent Progress

While growth isn’t the main focus for value strategies, LNTH’s Growth Rating of 5/10 shows steady performance:

- Historical Growth: Revenue rose 34.6% yearly over the past five years, with EPS up 42.1%. Recent revenue growth (12.5% YoY) remains solid.

- Future Expectations: Modest forward EPS (7.2%) and revenue (7.7%) growth estimates suggest stability rather than decline.

The slowdown in growth rates needs watching, but LNTH’s valuation seems to account for this, offering some protection.

Conclusion: A Strong Case for Value

Lantheus Holdings Inc pairs low pricing with solid financials—a sign of value opportunities. Its low P/E, high profitability, and sturdy balance sheet make a persuasive argument for investors hunting for undervalued quality. While growth is slowing, the safety margin from its valuation may balance this out.

For those searching for similar options, check out more Decent Value Stocks using ChartMill’s predefined screener.

Disclaimer: This analysis is not investment advice. Do your own research or consult a financial advisor before making investment decisions.