Twenty-six years. That's how long it took Intel to take out the record it set at the peak of the dot-com bubble. On Friday, in a single session, it did exactly that and dragged the entire semiconductor sector along for one of the most remarkable weeks in the index's history.

But markets don't exist in a vacuum, and the weekend brought three separate developments that will matter just as much to portfolios as any earnings report.

The Rundown

- The semiconductor sector closed its longest consecutive winning streak on record, fueled by a blowout earnings report from a major chipmaker

- Two of the world's largest tech companies announced a major AI infrastructure deal, signaling continued acceleration in private AI investment

- US-Iran peace talks collapsed before they even began, leaving the Middle East conflict unresolved heading into this week

- The path to a new Federal Reserve chairman cleared over the weekend, with the last Senate holdout dropping his opposition

When Chips Are Flying

INTEL CORP (INTC | ▲23.60%) had the kind of Friday that makes you check the ticker twice.

First-quarter results came in well above what Wall Street was expecting: strong datacenter CPU demand - driven by the AI buildout that companies keep actually funding - translated into revenue and earnings beats, plus an optimistic forward outlook. The stock broke through the all-time high set in August 2000. A record that had stood for 26 years, gone in one session.

The rest of the chip sector didn't need a second invitation.

ADVANCED MICRO DEVICES (AMD | ▲13.91%) jumped 14%, QUALCOMM INC (QCOM | ▲11.12%) added 11%, and NVIDIA CORP (NVDA | ▲4.32%), no longer a member of the Dow Jones after replacing Intel there in 2024, gained 4.3%.

The ISHARES SEMICONDUCTOR ETF (SOXX | ▲4.67%) tracking the 100 largest US semiconductor stocks, closed its 18th consecutive positive session.

- Weekly gain: nearly 10%.

- Monthly gain: around 40%.

To find comparable numbers in such a short window, you'd have to go back to the dot-com era. That's the company this rally is now keeping.

The Nasdaq Composite (COMPX | ▲1.63%) settled at 24,836, exactly 20% above its March 30 low. The Dow Jones (DJI | ▼0.16%) dipped 0.2%, the irony being that it swapped Intel for Nvidia two years ago and missed the historic session its former component just had.

The obvious question for the week ahead: do the chip names hold after reporting? All five major tech companies - including several of the above - report next week. One disappointing print could shift the tone fast.

AI Money Keeps Moving

ALPHABET INC-CL A (GOOGL | ▲1.63%) confirmed it will invest up to $40 billion in Anthropic, the AI startup behind Claude. The stock opened lower on Friday before reversing to close nearly 2% higher. The market hesitated, then decided the bet makes sense. Worth watching what that says about sentiment around large AI capital commitments, investors are clearly running the numbers now rather than just applauding the headline.

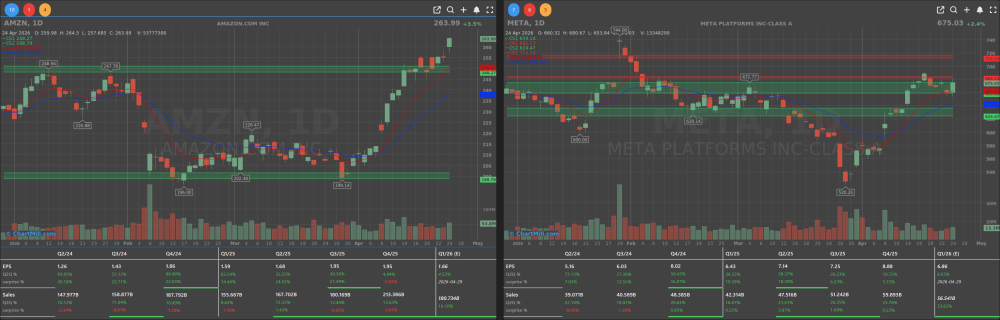

AMAZON.COM INC (AMZN | ▲3.49%) and META PLATFORMS INC-CLASS A (META | ▲2.41%) went further.

Meta will rent hundreds of thousands of Amazon Graviton chips for AI inference work, running models, not training them. It's a deal that tells you exactly where private AI infrastructure spending is right now: massive, accelerating, and flowing between the same handful of players. Amazon gained 3.5% on the news, Meta 2.4%.

Meta also confirmed internally that it plans to cut its workforce by 10% as it shifts more resources toward AI. That combination - headcount reduction plus multi-billion chip orders - is a pretty clear statement about where the company thinks value will come from.

The notable exception in all of this was APPLE INC (AAPL | ▼0.87%), which closed lower on a day when AI enthusiasm was carrying most of tech. The market has a short memory for many things, but it hasn't forgotten that Apple is still playing catch-up here.

Other Movers Worth Noting

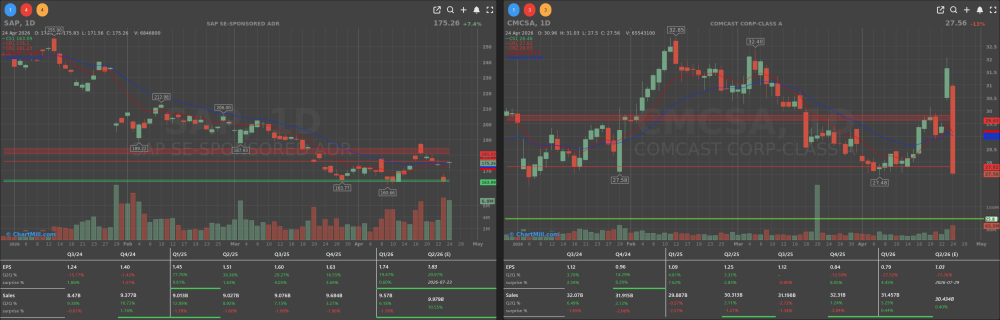

SAP SE-SPONSORED ADR (SAP | ▲7.36%) delivered strong quarterly results, with cloud revenue growing 19%. The German software giant doesn't get the same airtime as its US counterparts, but a 7.4% jump in the American listing is hard to overlook, especially in a quarter where cloud growth is still the metric investors care most about.

COMCAST CORP-CLASS A (CMCSA | ▼12.90%) had a rough one. Deutsche Bank cut the stock from buy to hold, citing no clear path to further value creation at the NBCUniversal parent. Thirteen percent in a single session is the kind of drop that forces a decision for anyone holding: is this an overreaction, or did the analyst just say what the market already knew?

In the weight-loss drug space, ELI LILLY & CO (LLY | ▼3.67%) fell nearly 4% on disappointing prescription data for its new GLP-1 pill Foundayo. NOVO NORDISK A/S B SHRS ADRH (NVOH | ▲6.47%) absorbed that anxiety and then some, gaining 6.8%. The competition between these two remains one of the more consequential ongoing stories in healthcare, every data point gets traded immediately.

HIMS & HERS HEALTH INC (HIMS | ▲8.56%) got a boost from a JPMorgan buy rating, adding 8.6%. COURSERA INC (COUR | ▼11.56%) dropped 11.6% after first-quarter results fell short of expectations.

The Macro Picture: Oil Up, Confidence Down

-

Oil ended the week at elevated levels. WTI crude settled at $94.40 per barrel on Friday, down 1.5% on the day, but up more than 14% over the week. Brent closed at $105.33, essentially flat Friday but 16% higher week-on-week. Those are not small moves. They're feeding directly into what consumers expect prices to do next.

-

The University of Michigan consumer confidence index fell from 53.3 in March to 49.8 in April. Economist Joanne Hsu pointed specifically to the Middle East conflict as the main transmission mechanism, through gasoline prices. US consumers now expect inflation to run at 4.7% over the next year, up from 3.8% in March. The Fed will be reading that number carefully, it complicates any argument for near-term rate cuts.

-

The euro-dollar pair ended the week flat at 1.1717.

Iran-US: Talks That Never Happened

This was the story that looked like progress on Friday and collapsed by Saturday. The US had been set to send Special Envoy Steve Witkoff and Jared Kushner to Islamabad for direct talks with Iran's Foreign Minister Abbas Araghchi. By Saturday morning, Trump announced the delegation wasn't going. The flight would be a waste of time, he said, adding that the US holds "all the cards."

Araghchi had already arrived in Pakistan. He met with officials, declared the visit "very fruitful," and left for Oman. Russia is next on his itinerary.

Whether this is posturing ahead of a deal or a genuine breakdown isn't clear. What is clear: the Strait of Hormuz remains a live risk, Trump has publicly said it stays "sealed shut," and oil at $94–105 per barrel is the market's current read on that situation. Anyone with energy exposure should treat this as unresolved, because it is.

Fed Chair: The Last Vote Falls Into Place

Kevin Warsh's path to the Federal Reserve chairmanship got easier over the weekend. Republican Senator Thom Tillis had been blocking Warsh's nomination, refusing to support it until a criminal investigation into current chair Jerome Powell was closed. On Friday, federal prosecutor Jeanine Pirro announced the investigation's closure, the probe related to cost overruns in the Fed's Washington headquarters renovation, now estimated at $2.5 billion against an original $1.9 billion budget. Tillis announced his support on Sunday.

Powell's term ends May 15. Warsh appeared before the Senate earlier in the week and made his position on independence clear. The political timeline is tight, and the confirmation vote is now the next thing to watch.

Washington: An Incident Nobody Wanted

Late Saturday, a 31-year-old California teacher named Cole Tomas Allen opened fire at the White House Correspondents' Dinner at the Washington Hilton. No one was critically hurt, one Secret Service agent was struck but his vest absorbed the bullet, and Trump was evacuated from the venue. Allen was arrested; he reportedly told authorities he intended to target Trump administration officials. He had no prior criminal record.

Trump held a press conference at the White House around 10:30 PM, praised the response of law enforcement, and attributed the apparent lone-wolf attack to a troubled individual. World leaders, including UK Prime Minister Starmer, European Commission President von der Leyen, and President Macron, condemned the incident.

It follows the July 2024 assassination attempt in Pennsylvania. The security questions it raises are ones the administration will have to answer publicly this week, and the political tone heading into the trading week is heavier for it.

Bottom line

The chip story was genuinely impressive, Intel's numbers, the SOXX streak, the AI capital flowing between Alphabet, Amazon, and Meta all confirm that the technology investment cycle is alive. But I'd be cautious about reading Friday's close as a clean signal.

The Iran talks fell apart, consumer confidence is slipping, oil is expensive, and earnings season is about to deliver several tests at once. A rally that's come this far, this fast, needs solid results to hold. We'll find out soon enough.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.