After Wednesday’s highly negative breadth washout, Thursday brought a clear short-term improvement in participation, especially on a daily and weekly basis. Still, the broader picture did not materially improve: most medium-term breadth readings remain weak, leadership is scarce, and the major indexes are still trading at or near important support zones.

Index Overview (SPY, QQQ, IWM)

Short Term (Daily)

Long Term (Weekly)

Thursday’s index action showed a market trying to stabilize after the heavy internal damage seen on March 18, but the rebound was uneven and still lacked broad conviction.

closed at $659.8 (-0.25%). On the daily chart, price remains below both the EMA9 (668.3) and EMA21 (675.0), which keeps the short-term trend under pressure. More importantly, SPY is now sitting right on top of an important support area around 659-660. That level held into the close, but only barely. On the weekly chart, SPY is also testing a key area and is trading below the long-term trend reference, which suggests that the larger trend has clearly lost momentum.

closed at $593.02 (-0.32%) and continues to look technically weaker than the S&P 500. The ETF remains below both short-term moving averages on the daily chart and finished the session near the lower end of its recent range. On the weekly chart, QQQ is also leaning on support while staying below the overhead resistance zone around 627.6. Relative to earlier weakness in breadth, this confirms that technology-heavy leadership has not yet regained control.

was the notable exception, closing at $247.63 (+0.65%). Small caps showed relative resilience and managed to defend nearby support around 246. Even so, IWM also remains below its EMA9 and EMA21 on the daily chart, so this outperformance should still be viewed as tentative rather than as clear trend repair. On the weekly chart, IWM is hovering around its long-term trend line, which makes this area especially important going forward.

Compared with the previous trading day, the main takeaway is this: Wednesday looked like a broad washout session, and Thursday did indeed produce a bounce attempt in the internals, but price itself has not yet confirmed a meaningful reversal. The market found some footing, but not enough to say the short-term downtrend has ended.

Breadth indicators: a better day, but not yet a healthy market

The most obvious improvement came in the daily breadth figures.

-

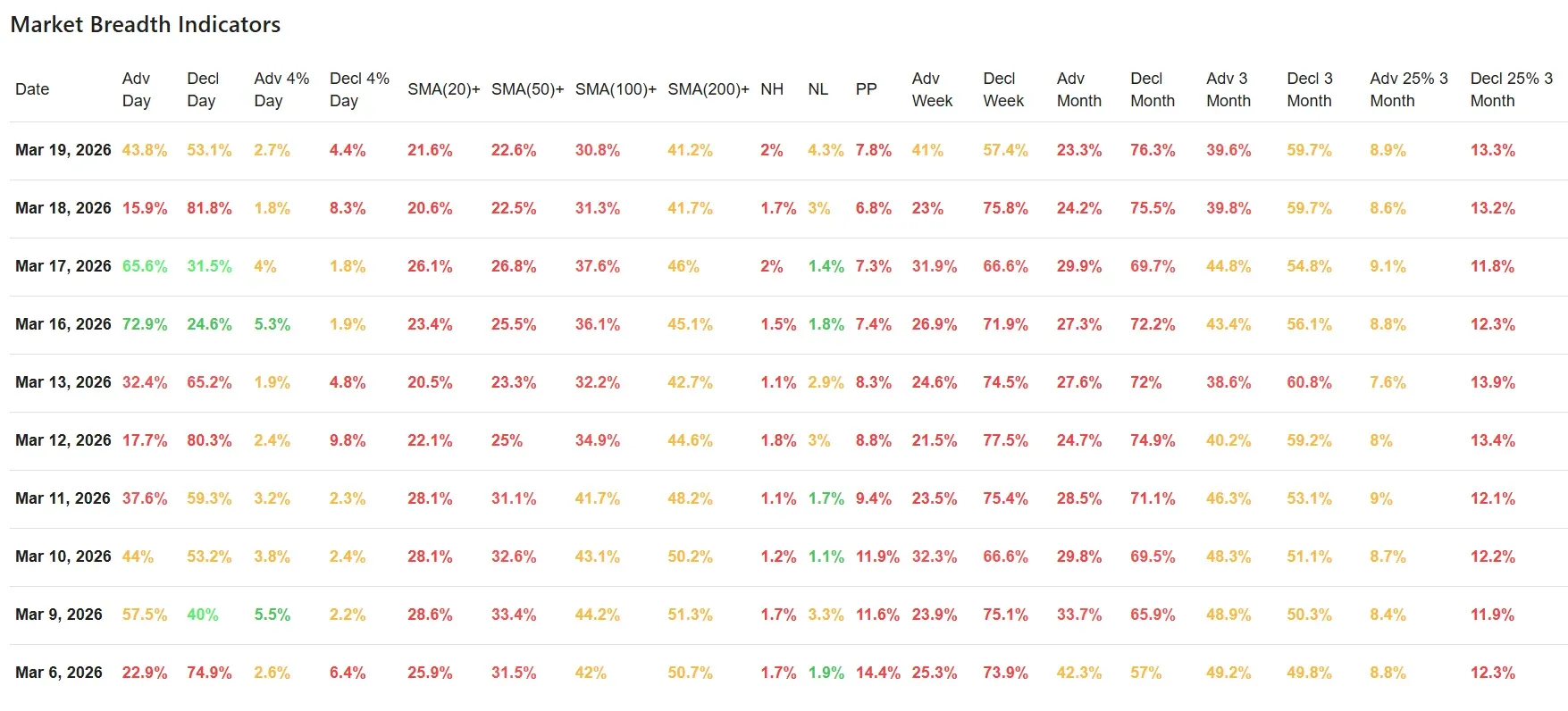

Advancing stocks: 43.8% vs. 15.9% the day before

-

Declining stocks: 53.1% vs. 81.8%

-

Advancers up more than 4%: 2.7% vs. 1.8%

-

Decliners down more than 4%: 4.4% vs. 8.3%

That is a meaningful improvement after Wednesday’s washout. The market clearly experienced less broad selling pressure, and the number of hard decliners dropped sharply. However, this was still not a positive breadth day, because decliners still outnumbered advancers and downside participation remained larger than upside participation.

This distinction matters. Thursday was not a strong thrust day. It was more accurately a stabilization day after internal damage, not a session that resets the trend.

Participation remains weak beneath the surface

The broader participation data continues to send a cautious message.

-

Above SMA(20): 21.6%

-

Above SMA(50): 22.6%

-

Above SMA(100): 30.8%

-

Above SMA(200): 41.2%

These readings remain very weak. Even though the shortest-term measure, the SMA(20)+, ticked up slightly from 20.6% to 21.6%, the market still has only about one in five stocks above the 20-day average. That is not the profile of a healthy uptrend.

The SMA(100)+ and SMA(200)+ readings actually edged lower versus the previous session, showing that Thursday’s better day did not yet translate into meaningful repair in the broader structure. The market may be trying to stabilize at the index level, but internally, a large share of stocks is still stuck in damaged trends.

This is also consistent with what we saw in the previous article: Wednesday’s weak breadth was not just a one-day blip. It came on top of already deteriorated internal conditions. Thursday interrupted the immediate selling pressure, but it did not reverse that larger pattern.

New highs, new lows and pocket pivots

Leadership remains scarce.

-

New Highs: 2.0%

-

New Lows: 4.3%

-

Pocket Pivots: 7.8%

New highs improved only marginally, while new lows actually increased from 3.0% to 4.3%. That is an important negative detail. On a truly constructive recovery day, you would prefer to see new lows contract materially. Instead, there is still ongoing weakness beneath the surface.

Pocket pivots rose to 7.8% from 6.8%, which is mildly encouraging and suggests some individual stocks are trying to regain momentum. Still, this is not yet enough to suggest that leadership is broadening in a convincing way.

Weekly breadth improved, but monthly breadth is still poor

One of the more constructive changes on Thursday was in the weekly breadth data.

-

Adv Week: 41.0% vs. 23.0%

-

Decl Week: 57.4% vs. 75.8%

That is a clear improvement and tells us the one-day rebound had enough impact to soften the most immediate weekly damage. But zooming out a bit further, the monthly data remains decisively weak:

-

Adv Month: 23.3%

-

Decl Month: 76.3%

Those numbers are still extremely poor and even slightly worse than the previous day. That tells us the market’s medium-term condition remains under pressure, despite Thursday’s better tape.

The 3-month breadth also barely changed:

-

Adv 3 Month: 39.6%

-

Decl 3 Month: 59.7%

That lack of improvement reinforces the same conclusion: Thursday helped stop the bleeding temporarily, but the broader trend remains negative.

10-day perspective: the trend is still damaged

Looking across the last 10 trading days, the market continues to show a pattern of unstable rebounds inside a weakening breadth backdrop.

A few observations stand out:

-

Only a handful of sessions produced clearly positive daily breadth.

-

Several days showed very heavy downside participation, including March 12 and especially March 18.

-

The percentages of stocks above their short- and medium-term moving averages remain persistently low.

-

Monthly and 3-month breadth never recovered enough to suggest durable internal strength.

So while Thursday was better than Wednesday, it fits more into the category of reactionary relief than of trend repair.

That also lines up well with the index charts. The major ETFs are testing support, but none of them has yet reclaimed key short-term moving averages. Until that happens, better breadth on a single day should be treated carefully.

Final conclusion

Thursday’s session brought a welcome improvement after Wednesday’s washout, especially in daily and weekly breadth. That suggests selling pressure eased and that the market is at least trying to stabilize near important support levels.

Still, the broader message remains cautious. Most stocks are still below key moving averages, new lows remain too elevated, and monthly breadth continues to show a market with very limited participation. In other words, the market stopped getting worse for a day, but it has not yet become healthy again.

The next few sessions will be crucial. If SPY and QQQ can hold support and reclaim their short-term moving averages while breadth continues to improve, this could become the start of a more meaningful repair phase. But if support breaks again, Thursday’s improvement will likely be remembered as only a brief pause within a still-fragile market environment.

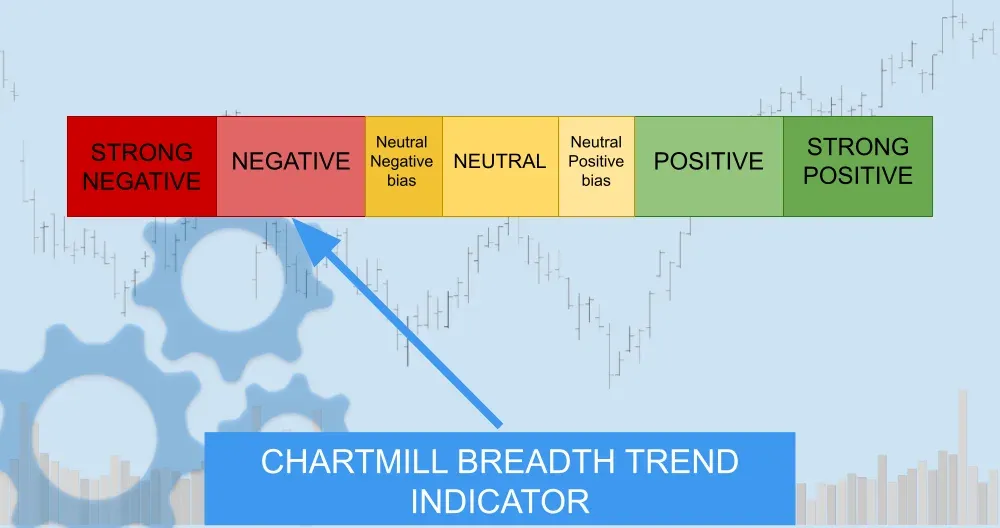

Breadth trend rating: 2/7 — Negative

The rating remains negative, not because Thursday was weak in isolation, but because the improvement was not broad or deep enough to change the larger picture. Relative to the previous day, the internals clearly improved, but the overall breadth trend still reflects a market with damaged participation, weak leadership, and major indexes that remain technically vulnerable.

ChartMill Market Desk

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Oil Diplomacy Rescues Wall Street From a Deeper Sell-Off — But the Hormuz Knot Remains Untied