In the world of long-term investing, few strategies have shown the lasting strength and practical attraction of Peter Lynch’s approach, which highlights finding companies with good growth potential trading at fair prices. This method, often called Growth at a Reasonable Price (GARP), avoids speculative extremes by concentrating on sustainable business performance, sound financials, and operations that are easy to understand. One company that recently appeared through a screen built on Lynch’s criteria is INTERPARFUMS INC (NASDAQ:IPAR), a fragrance and personal care products company with a collection of famous licensed brands.

Financial Health and Stability

A key part of Lynch’s strategy is investing in companies with solid balance sheets and controlled debt, lowering risk while permitting consistent growth. Interparfums does very well in this area, showing several important signs of financial strength:

- Debt-to-Equity Ratio: 0.24, much lower than the strategy’s upper limit of 0.6 and even Lynch’s personal choice of 0.25.

- Current Ratio: 2.96, showing more than enough short-term liquidity to meet obligations.

- Altman-Z Score: 5.61, pointing to a very small chance of financial trouble.

These numbers show a company that is not carrying too much debt and has the steadiness required to withstand market changes, a crucial feature for long-term investors.

Profitability and Efficiency

Lynch favored companies that produce high returns on equity, as this frequently connects with capable management and a market advantage. Interparfums performs strongly here, with a Return on Equity (ROE) of 19.18%, exceeding the 15% minimum Lynch suggested. Also, the company displays very good margins and efficiency:

- Operating Margin of 19.21%, doing better than 94% of industry competitors.

- Return on Invested Capital (ROIC) of 16.62%, also higher than industry averages.

This kind of profitability not only helps reinvestment and growth but also matches Lynch’s focus on companies that benefit shareholders through effective operations.

Growth and Valuation Balance

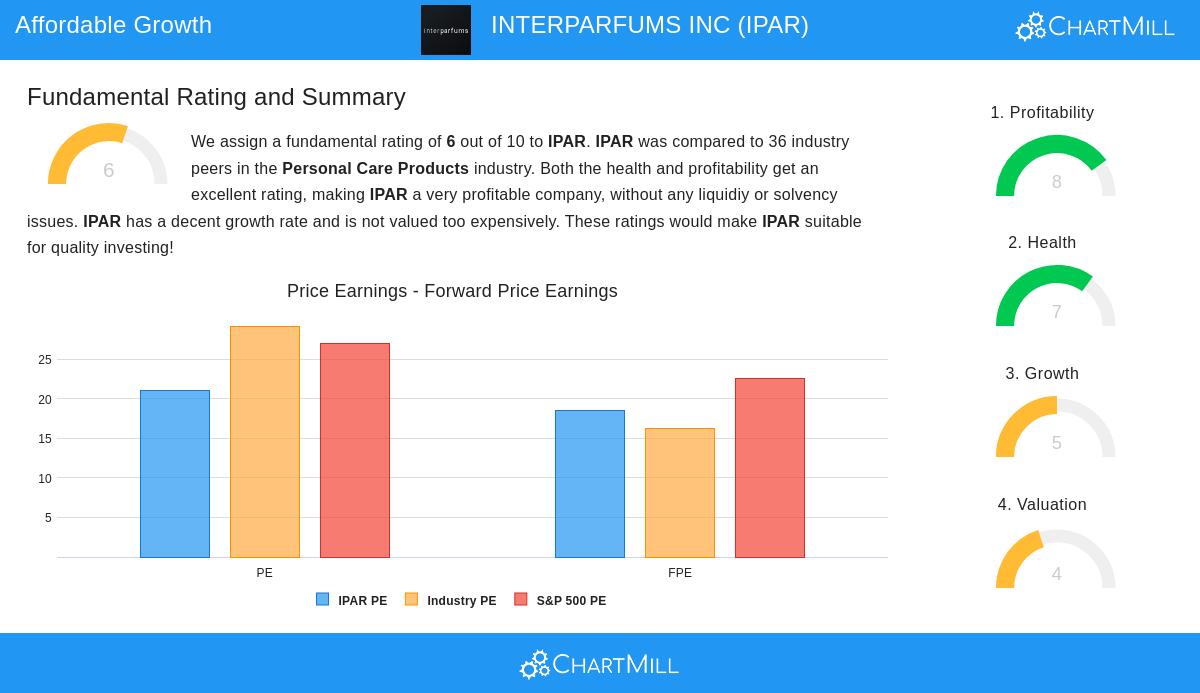

Maybe the most unique part of Lynch’s method is looking for companies with good historical growth that is not too slow or unsustainably fast. Interparfums has reached a 5-year EPS growth rate of 22.27%, fitting well within Lynch’s goal range of 15–30%. This growth is supported by a fair valuation, as shown in a PEG ratio (past 5 years) of 0.95, under the important level of 1. This suggests the stock’s price stays fair compared to its historical earnings growth, a Lynch characteristic for spotting undervalued growth chances.

While future growth estimates are more conservative, the company’s set brand partnerships and global distribution system offer a base for ongoing, stable expansion.

Fundamental Analysis Overview

A detailed fundamental analysis of Interparfums gives it a score of 6 out of 10, showing good points in profitability and financial health, balanced by a high dividend payout ratio and slowing growth forecasts. Important points to note include:

- Very good solvency and liquidity numbers.

- Firm, industry-leading margins.

- A dividend yield of 2.80%, though questions about sustainability exist because of high payout levels.

This outline indicates a company that is fundamentally healthy and well-situated within its sector, even with some areas needing investor attention.

Conclusion

Interparfums represents many features that Peter Lynch thought necessary for profitable long-term investing: operations that are easy to understand, sound financials, profitable growth, and fair valuation. While not free from risks, such as a high dividend payout and reduced future growth forecasts, the company’s fit with Lynch’s strategy makes it an interesting option for investors looking for growth at a reasonable price.

For those wanting to investigate other companies that match similar standards, more outcomes are available using the Peter Lynch Strategy stock screen.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consider their financial situation and risk tolerance before making investment decisions.