Harmony Biosciences Holdings (NASDAQ:HRMY) stands out as an affordable growth stock based on our fundamental screening criteria. The company, focused on treatments for neurological disorders, combines strong growth prospects with solid financial health and profitability—all while trading at a reasonable valuation.

Growth Potential

HRMY has demonstrated impressive growth metrics:

- Revenue surged 20.62% over the past year, with an average annual growth rate of 160.13% in recent years.

- Earnings per share (EPS) grew at an average annual rate of 44.61% historically, with expectations for 35.76% annual growth in the coming years.

- The company’s primary product, WAKIX, addresses narcolepsy, a market with limited competition, supporting sustained revenue expansion.

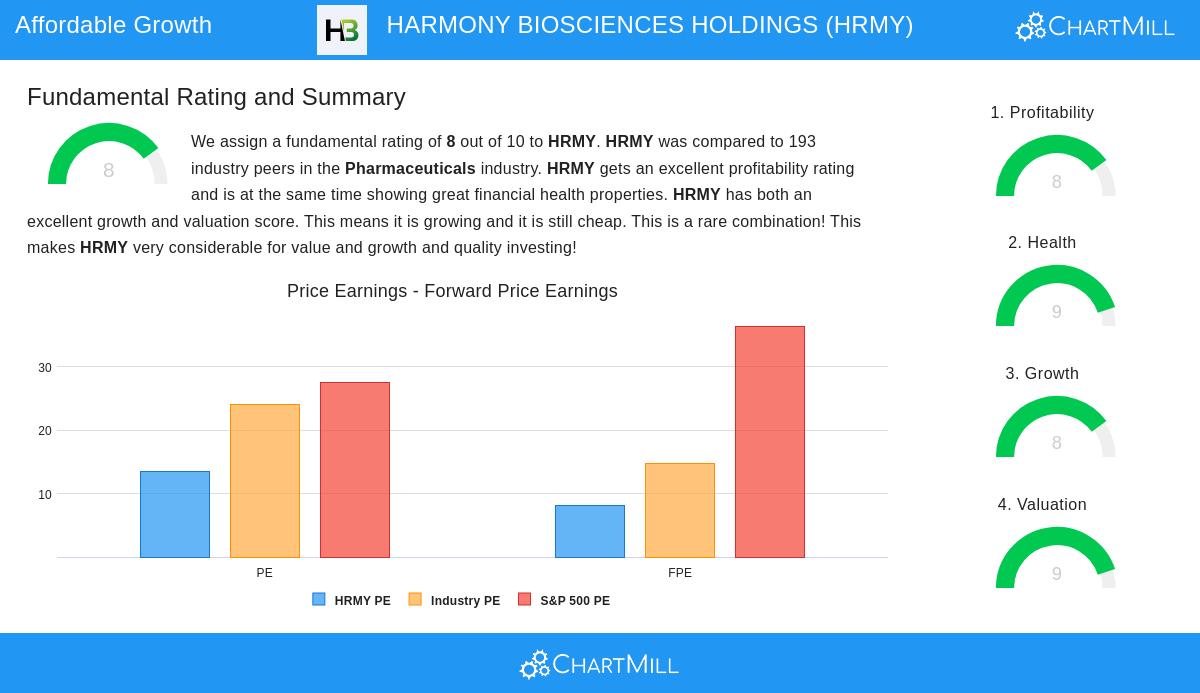

Valuation Appeal

Despite its strong growth, HRMY remains reasonably priced:

- A P/E ratio of 13.44 is below the industry average (24.04) and significantly lower than the S&P 500 average (27.50).

- The forward P/E of 8.12 suggests further upside potential.

- 90.67% of pharmaceutical industry peers trade at higher enterprise value-to-EBITDA multiples.

Financial Health & Profitability

The company maintains a strong balance sheet:

- Altman-Z score of 5.71 indicates low bankruptcy risk.

- Debt-to-equity ratio of 0.22 reflects prudent leverage.

- Return on equity (21.22%) and operating margin (28.46%) rank in the top tier of the industry.

For a deeper look at HRMY’s fundamentals, review the full analysis report.

Our Affordable Growth screener lists more stocks with similar characteristics and is updated daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own research before making investment decisions.