Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with steady growth at fair prices, commonly known as Growth at a Reasonable Price (GARP). His method relies on fundamental analysis, selecting firms with solid profits, low debt, and reliable earnings growth, while steering clear of overvalued or highly leveraged businesses. The strategy targets companies in good financial shape, trading at appealing prices compared to their growth prospects, and able to generate lasting returns without depending on short-term speculation.

One stock that fits these standards is HARMONIC INC (NASDAQ:HLIT), a company specializing in video delivery software and broadband solutions. It meets multiple criteria from Lynch’s approach, making it worth considering for investors focused on GARP.

Why Harmonic Matches the Peter Lynch Approach

-

Steady Earnings Growth (EPS 5Y: 23.05%)

Lynch looked for companies with reliable earnings growth, typically between 15% and 30% per year—enough to deliver returns without being unrealistic. Harmonic’s five-year EPS growth of 23.05% fits this range, showing the company has increased profits at a sustainable rate. -

Fair Pricing (PEG Ratio: 0.43)

The PEG ratio, which accounts for growth when evaluating price, is key to Lynch’s strategy. A PEG below 1 suggests a stock may be undervalued given its growth potential. Harmonic’s PEG of 0.43 indicates the market might not fully recognize its earnings growth. -

Good Financial Standing (Debt/Equity: 0.27, Current Ratio: 1.99)

Lynch favored companies with little debt, as high leverage can increase risk during tough times. Harmonic’s Debt/Equity ratio of 0.27 is below the screener’s limit of 0.6 and close to Lynch’s ideal of under 0.25. Its Current Ratio of 1.99 also shows it has enough liquidity to cover short-term needs. -

Strong Return on Equity (ROE: 15.38%)

A high ROE signals effective use of shareholder funds, another priority for Lynch. Harmonic’s 15.38% ROE is better than 83% of its peers in the Communications Equipment sector, highlighting its profitability.

Key Strengths and Points to Watch

Harmonic’s fundamental report reveals a balanced yet encouraging picture:

- Profitability: Strong margins (Operating Margin of 15.93% tops 87.5% of peers) and returns (ROIC of 12.16%).

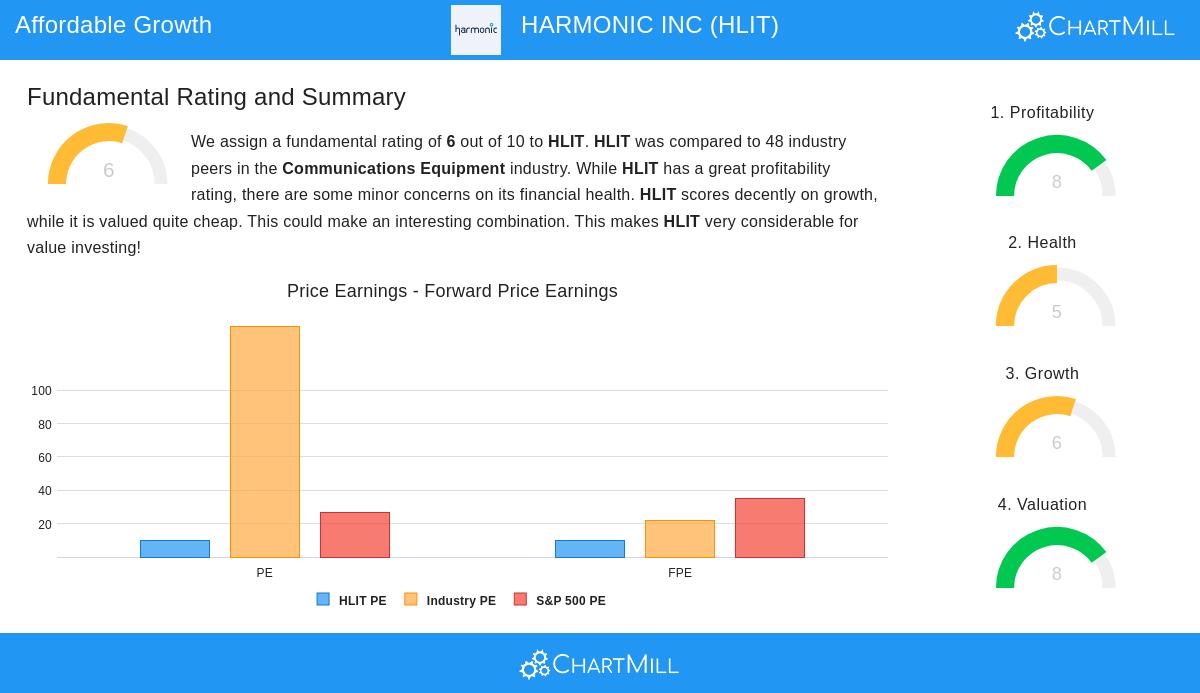

- Valuation: With a P/E of 9.86, it’s priced lower than 95.8% of industry rivals.

- Growth: Revenue rose 24.14% YoY, though future growth may slow.

- Risks: A low Altman-Z score (-0.17) points to potential solvency issues, but manageable debt and healthy cash flow lessen this concern.

What Investors Should Do Next

While Harmonic meets many of Lynch’s criteria, more research is needed—especially on its financial stability and industry position. For those looking for other stocks that align with this strategy, the Peter Lynch screen provides additional options.

Disclaimer: This article is not investment advice. Do your own research or consult a financial advisor before making investment decisions.