HAMILTON INSURANCE GROUP-CL B (NYSE:HG) stands out as an affordable growth candidate based on our screening criteria. The company combines strong growth metrics with reasonable valuation, while maintaining decent profitability and financial health.

Growth Highlights

- Revenue Growth: Over the past year, revenue increased by 45.20%, with a three-year average annual growth of 176.06%.

- Earnings Growth: EPS grew by 50.66% in the last year, with expected annual growth of 9.50% in the coming years.

- The company’s Growth Rating of 7/10 reflects its ability to expand faster than many industry peers.

Valuation Strengths

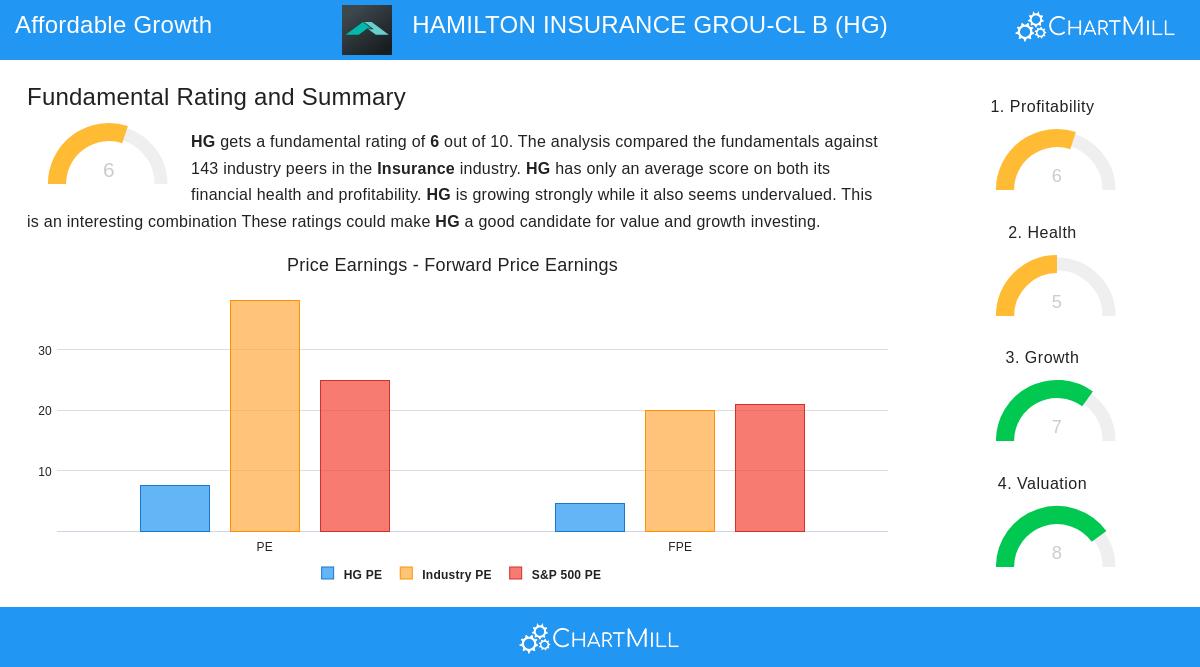

- Attractive P/E Ratio: Trading at a P/E of 7.50, HG is cheaper than 77.62% of its insurance industry peers.

- Forward P/E: At 4.62, the stock appears undervalued compared to both the industry and the S&P 500.

- Enterprise Value/EBITDA: More than 90% of competitors trade at higher multiples.

Profitability & Financial Health

- Strong Margins: Operating margin of 26.38% and profit margin of 17.49% rank in the top tier of the industry.

- ROIC Improvement: Return on invested capital rose to 6.45%, above its three-year average.

- Debt Management: A low debt-to-equity ratio of 0.06 indicates conservative leverage.

- Liquidity Concerns: Current and quick ratios of 0.18 are weak, though still better than many peers.

For a deeper look, review the full fundamental analysis of HG.

Our Affordable Growth screener lists more stocks with similar traits and updates daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own research before making investment decisions.