Investors looking for growth chances at fair prices often use screening methods that find companies with good basics trading at appealing prices. The "Affordable Growth" method looks for stocks showing solid growth paths while keeping good financial condition and profit measures, all without high price tags. This system helps investors prevent paying too much for growth while still finding companies with room to expand.

Halozyme Therapeutics Inc (NASDAQ:HALO) offers a notable example for affordable growth investing, receiving an overall fundamental score of 8 out of 10 from ChartMill's detailed analysis system. The company's biotechnology work centers on ENHANZE drug delivery technology, which enables subcutaneous delivery of injected drugs and fluids using its special enzyme rHuPH20.

Growth Profile

Halozyme shows notable growth features that fit well with affordable growth standards. The company has achieved significant increases in important financial measures:

- Revenue growth of 34.97% over the past year, with an average yearly growth rate of 38.95% over recent years

- Earnings Per Share growth of 58.41% in the last year, keeping a good 30.12% average yearly growth rate

- Future estimates point to continued growth with EPS predicted to rise 18.27% each year and revenue expected to grow 13.85% per year

These growth figures are much higher than industry standards and back the company's status as a true growth stock. The mix of past results and future estimates gives assurance about the durability of Halozyme's expansion path.

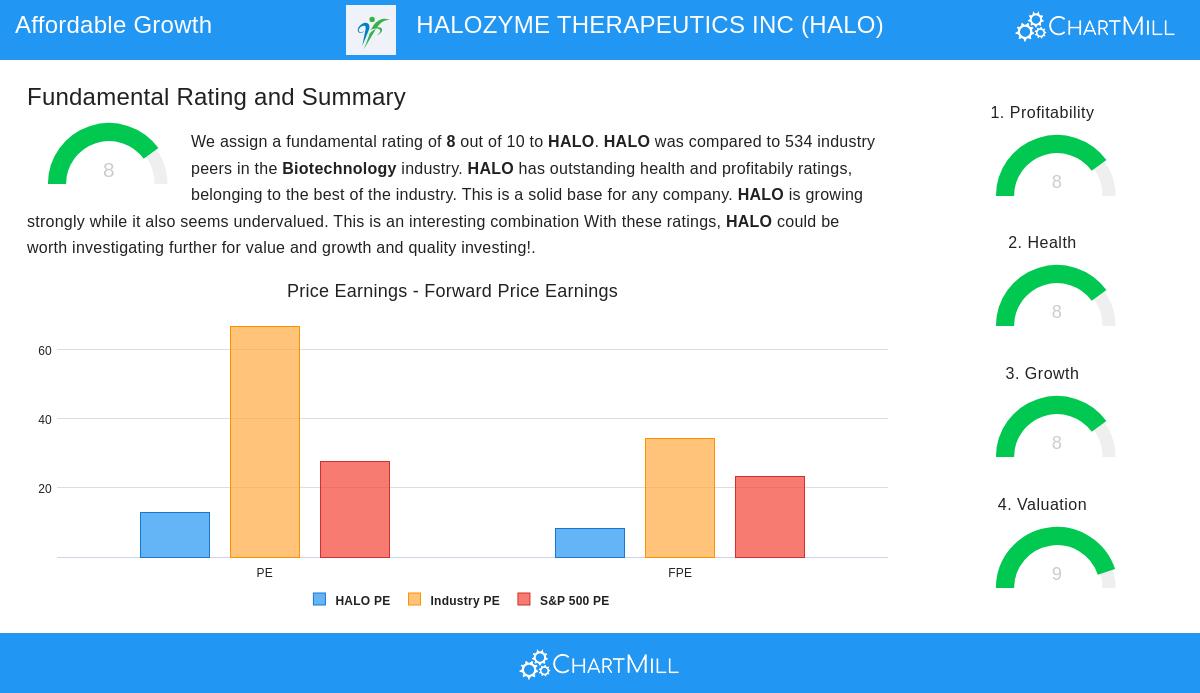

Valuation Assessment

Halozyme's valuation measures present a strong case for being affordable within the growth stock field:

- Price/Earnings ratio of 12.83, much lower than the S&P 500 average of 27.69

- Price/Forward Earnings ratio of 8.18, well under the industry average of 34.27

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios more affordable than 96% of industry competitors

- PEG ratio suggesting fair valuation when considering growth prospects

The company's valuation standing is especially significant given its good growth profile, implying the market may not completely recognize Halozyme's growth possibility or the quality of its earnings.

Profitability and Financial Health

Beyond growth and valuation, Halozyme displays good core business basics that support its affordable growth idea:

Profitability positives include:

- Excellent Return on Assets of 27.13%, doing better than 97.75% of biotechnology rivals

- Superior Return on Equity of 167.48%, with the industry's top performers

- Good profit margin of 47.28% and operating margin of 57.92%

- Steady profitability and positive cash flow production over several years

Financial condition signs show stability:

- Current ratio of 8.36 and quick ratio of 7.01 point to a good cash position

- Altman-Z score of 5.20 indicates minimal bankruptcy danger

- Acceptable debt levels compared to free cash flow production

- Share count decrease through buybacks improving shareholder value

Investment Considerations

Halozyme's mix of good growth, fair valuation, and sound financial basics places it as a strong option for investors searching for affordable growth chances. The company's ENHANZE technology work provides a lasting market edge, while its partnership approach with biopharmaceutical companies builds varied income sources.

While the company holds a somewhat high debt-to-equity ratio, this seems acceptable considering its good cash flow production and profit measures. The anticipated slowing in growth rates from past levels shows a normal progression for a developing growth company rather than a basic worsening of business outlook.

For investors wanting to review comparable affordable growth chances, more screening results are available using this customized stock screener that uses similar fundamental standards.

Disclaimer: This analysis uses fundamental data and scores given by ChartMill and should not be taken as investment advice. Investors should perform their own review and think about their personal financial situation before making investment choices. Past results do not ensure future outcomes, and all investments have built-in risks.