Halozyme Therapeutics Inc (NASDAQ:HALO) has been recognized through a fundamental screening method aimed at finding undervalued stocks with solid financial strength. The "Decent Value" screen selects companies with a valuation rating above 7, confirming they trade below their true value while showing good profitability, financial stability, and growth potential. This method fits with value investing principles, which target stocks priced lower than their actual worth but supported by strong fundamentals, lowering risk while providing room for gains as the market adjusts.

Why HALO Is a Notable Undervalued Pick

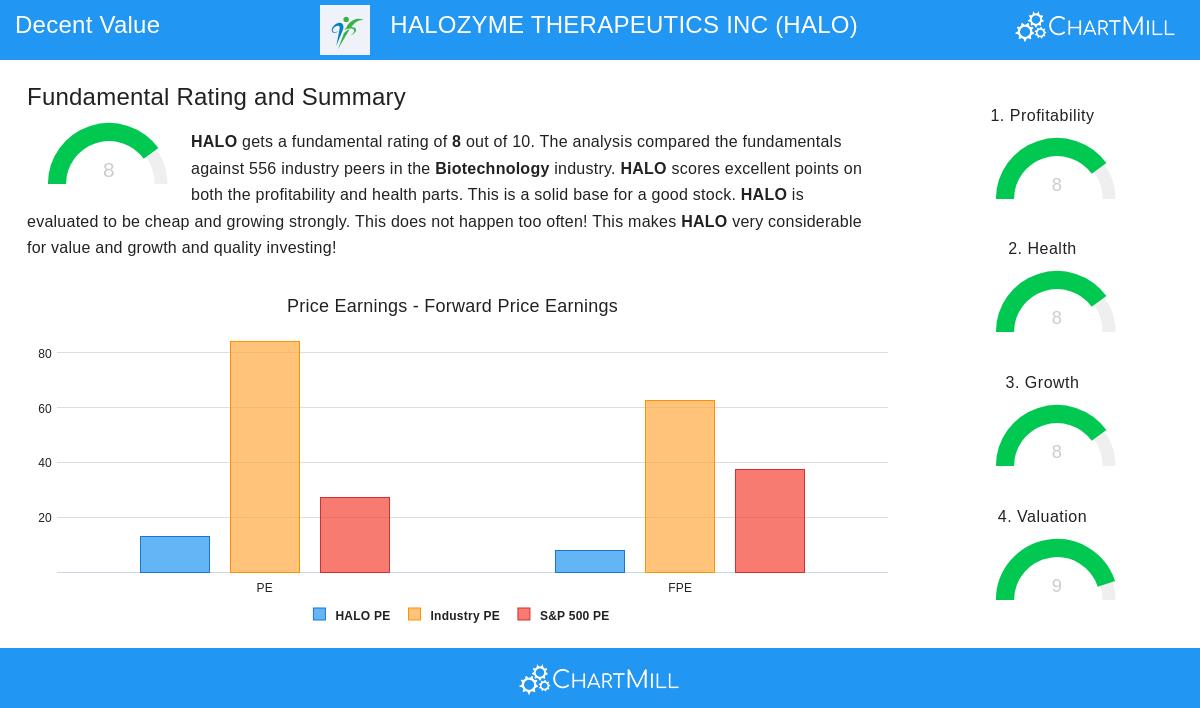

Halozyme’s fundamental analysis report points to several strengths that make it an interesting choice for value investors:

1. Appealing Valuation (Rating: 9/10)

The stock’s low multiples indicate it is priced below its earnings and cash flow:

- P/E Ratio of 12.92: Much lower than the industry average (84.33) and the S&P 500 (27.35), better than 96.6% of biotech competitors.

- Forward P/E of 7.69: Suggests further undervaluation, with HALO cheaper than 98.2% of its sector.

- Solid Free Cash Flow Yield: A low Price/FCF ratio puts it in the top 5% of the industry, confirming its bargain status.

For value investors, these metrics hint at a safety net—a key part of the strategy—as the stock’s price seems out of sync with its earnings potential.

2. Strong Profitability (Rating: 8/10)

Despite its low valuation, HALO shows high-margin results:

- 44.8% Net Profit Margin: Ranks in the top 1% of biotech companies, showing efficient operations and pricing strength.

- ROIC of 23.4%: Higher than its cost of capital, meaning it creates value.

- Steady Earnings Growth: EPS grew 46.8% YoY, with a 5-year annual growth rate of 30.1%.

Such profitability is uncommon in undervalued stocks, often a sign of temporary market oversight rather than weakening fundamentals.

3. Financial Stability (Rating: 8/10)

Halozyme’s balance sheet reduces risk for value investors:

- Good Liquidity: Current and Quick Ratios of 8.4 and 7.3, respectively, well above industry standards.

- Controlled Debt: While its Debt/Equity ratio (3.1) is high, a Debt/FCF ratio of 3.0 shows it can handle obligations.

- Share Reduction: Outstanding shares have dropped YoY, reflecting careful capital use.

Financial health is key for value stocks, as it ensures the company can endure market swings while waiting for price recognition.

4. Growth Potential (Rating: 8/10)

Undervalued stocks with growth prospects offer a "double opportunity":

- Revenue Growth: 25.7% YoY, with a 5-year CAGR of 39%.

- Forward EPS Growth: Projected at 16.8% yearly, backed by its ENHANZE drug-delivery platform and partnerships (e.g., Teva, Idorsia).

Growth at a reasonable price (GARP) is a trait of successful value investing, as it speeds up the alignment of price and true value.

Risks to Watch

- Sector Swings: Biotech stocks face regulatory and R&D challenges.

- Debt Levels: High Debt/Equity could strain margins if interest rates climb.

- Slower Growth: Forward revenue growth (12.6%) trails past performance.

Final Thoughts

Halozyme Therapeutics fits the "decent value" screen’s aim: a financially healthy company trading at a discount. Its mix of low valuation, high profitability, and growth potential matches Benjamin Graham’s ideas of investing with a safety buffer. For investors looking for similar picks, discover more undervalued stocks using the Decent Value Stocks screener.

Disclaimer: This analysis is not investment advice. Do your own research or consult a financial advisor before making decisions.