FLEX LTD (NASDAQ:FLEX) stands out as a potential candidate for long-term investors seeking growth at a reasonable price (GARP). The company, a global manufacturing services provider, meets key criteria from Peter Lynch’s investment strategy, balancing solid growth with sound financial health and valuation.

Key Strengths

- Earnings Growth: FLEX has delivered a 5-year average EPS growth of 16.4%, aligning with Lynch’s preference for sustainable but not excessive growth (15-30% range).

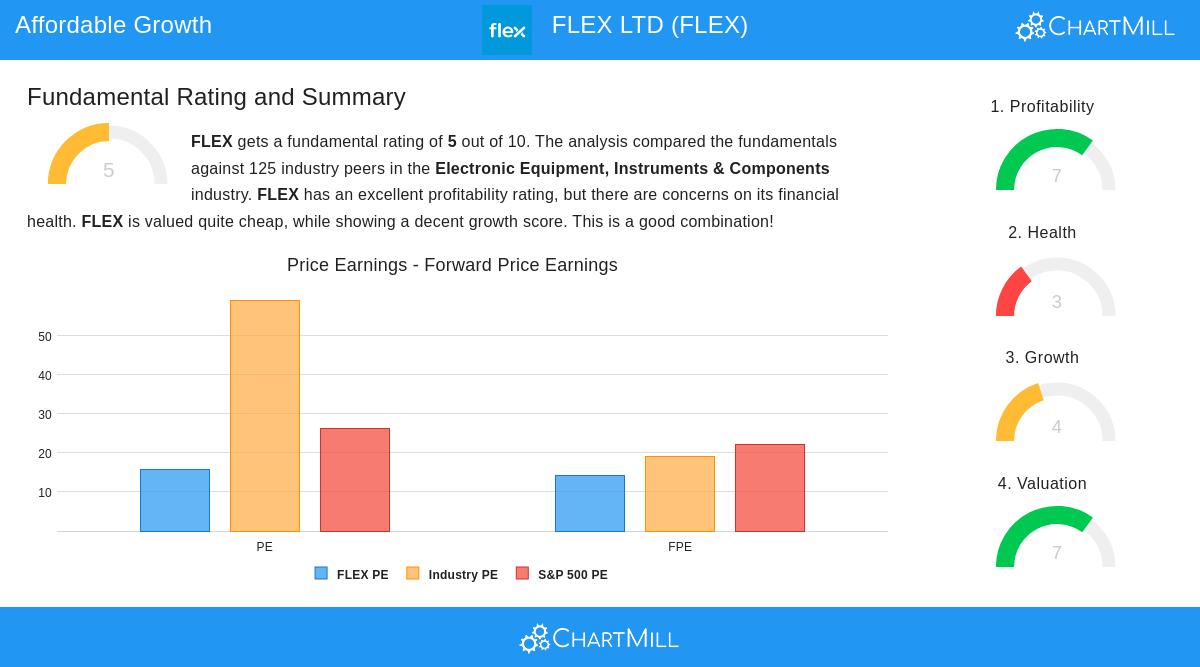

- Attractive Valuation: With a PEG ratio of 0.97 (below 1), the stock appears reasonably priced relative to its growth. The P/E ratio of 15.88 is also below both the industry and S&P 500 averages.

- Strong Profitability: The company’s Return on Equity (ROE) of 16.77% exceeds Lynch’s 15% threshold, indicating efficient use of shareholder capital.

- Financial Health: FLEX maintains a manageable Debt/Equity ratio of 0.53, though slightly above Lynch’s stricter preference of 0.25. The Current Ratio of 1.40 suggests adequate liquidity.

Fundamental Highlights

FLEX earns a 5/10 fundamental rating, with strengths in profitability and valuation but some concerns in financial health, particularly liquidity metrics. The company outperforms most peers in ROE and ROIC but lags in gross margins. Revenue growth has been modest, though future EPS growth is projected at 9.38% annually.

For a deeper dive, review the full fundamental analysis of FLEX.

Our Peter Lynch Strategy screener lists more stocks fitting this strategy and updates daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own research before making investment decisions.