For investors looking for chances where a company's market price may not completely show its basic business quality, a systematic value investing method can be a practical structure. This plan focuses on finding stocks that seem priced below their worth using core measures, such as earnings, cash flow, and balance sheet condition, while also showing good operational results. One way to find these possibilities is by looking for companies with good valuation scores together with acceptable marks for earnings power, balance sheet strength, and expansion. This mix points to a business that is both operationally healthy and possibly available for less than its true worth.

Expedia Group Inc (NASDAQ:EXPE) recently appeared from such a search. As a top online travel company running brands like Expedia.com, Hotels.com, and Vrbo, its operations are closely linked to worldwide travel activity. The core review indicates it may show a situation where the market's present price does not completely account for the company's operational positives.

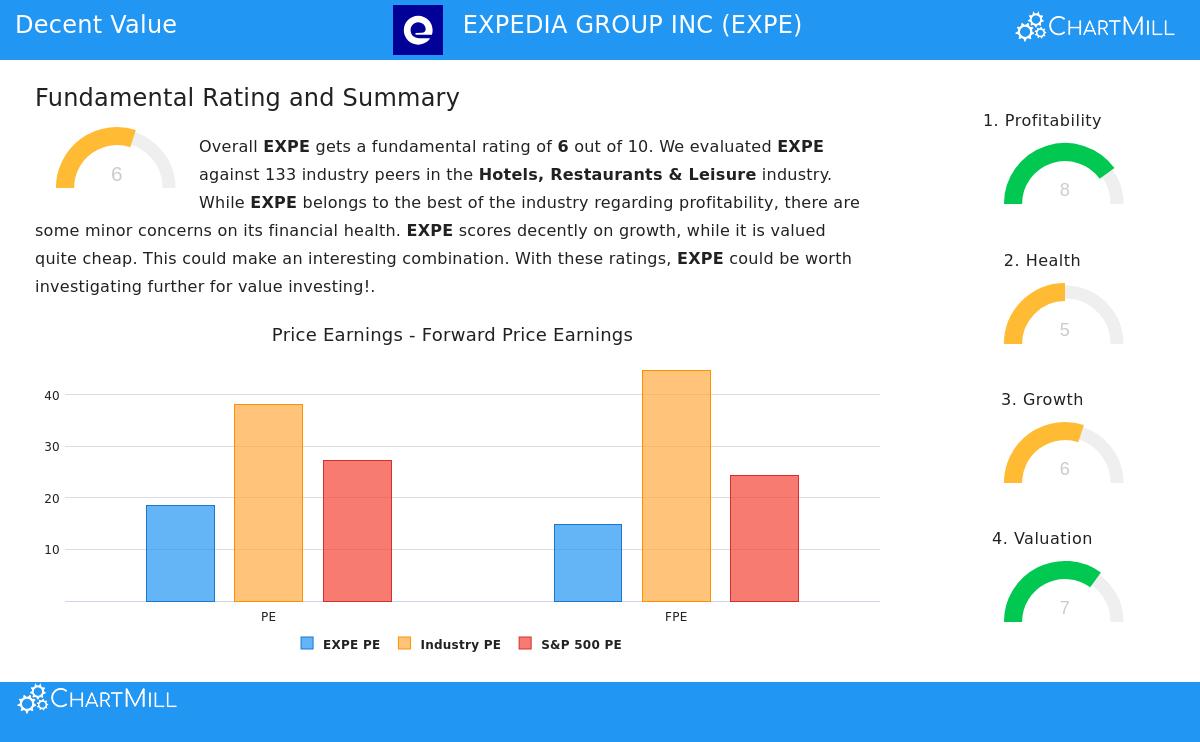

Valuation: A Central Support for Value Investors

The main filter for a "reasonable value" stock depends on a good price, which is the essential idea of value investing. The aim is to pay less than the business is truly worth. Expedia’s core report gives it a Valuation Score of 7 out of 10, showing a relatively low price within its field.

Important price measures from the report are:

- Price-to-Earnings (P/E) Ratio: At 18.60, EXPE’s P/E is lower than 73.68% of similar companies in the Hotels, Restaurants & Leisure industry and is under the S&P 500 average.

- Forward P/E Ratio: A better number of 14.89 indicates the price seems even more sensible based on future profit forecasts, putting it lower than 75% of industry rivals.

- Price-to-Free Cash Flow: This is a especially good point, with EXPE priced lower than 93% of its industry using this measure, pointing to good cash creation compared to its market price.

For a value investor, these measures are important. They give number-based proof that the stock is not selling at a high price, making a possible "margin of safety"—a cushion between the price paid and the calculated real worth of the business.

Earnings Power and Expansion: Confirming Quality at a Lower Price

A low-priced stock is only a worthwhile investment if the basic company is stable and earns money. A pure value trap—a stock that is cheap for a clear cause—often does not have these traits. Expedia’s core report shows good earnings power, with a score of 8/10.

The company shows high-grade profits:

- It has notable return measures, including a Return on Equity of 103.81% and a Return on Invested Capital of 18.46%, doing better than most of its industry.

- Profit margins are good and getting better, with a Gross Margin of almost 90% and a firm Operating Margin of 13.72%.

Also, with an Expansion Score of 6/10, EXPE is not standing still. The report notes a good past EPS growth rate of almost 15% per year, with forecasts for that growth to increase to about 18% in the next few years. This pairing of high earnings power and positive expansion path is necessary; it indicates the company has the operational strength to possibly develop into and support a higher price later.

Balance Sheet Strength: Reviewing the Financial Risk

Balance sheet strength is the base that holds up everything else. A company with excessive debt or weak cash availability can have its good core measures fall apart. Expedia’s Strength Score is a middle 5/10, showing a varied situation that needs detailed examination.

The review shows both positives and points to watch:

- Good Indicators: The company produces plenty of free cash flow, with a low Debt-to-Free Cash Flow ratio of 2.07 years, showing a good ability to handle its debts. It is also producing value, as its ROIC is above its cost of capital.

- Points to Watch: The report notes a low Current Ratio and Quick Ratio (both 0.74), hinting at possible issues in paying near-term bills. Its Altman-Z score also signals financial risk, although it is similar to many industry peers.

For a value investor, this detailed strength profile is a main part of the review. The good cash flow creation is a important positive that lessens some of the balance sheet worries, but it stays an area to watch carefully.

Conclusion: A Possibility for More Value Study

Based on the core review given by ChartMill’s report, Expedia Group shows a profile that matches several value investing ideas. It sells at price levels that are good compared to both its industry and the wider market, while also displaying high earnings power and acceptable forecasted expansion. The balance sheet strength score adds a point of care, but the company’s strong free cash flow gives a meaningful offset.

This mix of a good price with otherwise firm core measures makes EXPE an interesting possibility for investors using a value-focused plan to examine more. It shows the kind of chance filters try to locate: a possibly under-priced stock that is not a value trap, but a profitable business selling at a sensible price.

Disclaimer: This article is for information only and does not make up financial guidance, a suggestion, or an offer to buy or sell any security. Investing has risk, including the chance of losing the original investment. You should do your own study and talk with a certified financial consultant before making any investment choices.