EXELIXIS INC (NASDAQ:EXEL) stands out as an affordable growth candidate based on our screening criteria. The company combines solid growth prospects with reasonable valuation metrics, while maintaining strong financial health and profitability.

Growth Prospects

- Strong Historical Growth: EXEL has demonstrated impressive growth, with earnings per share (EPS) increasing by 205.56% over the past year and revenue growing by 24.50%.

- Sustained Expansion: Over the last several years, EPS and revenue have grown at annualized rates of 12.65% and 17.51%, respectively.

- Positive Outlook: Analysts expect EPS to grow by 25.80% annually in the coming years, with revenue projected to increase by 11.19% per year.

Valuation

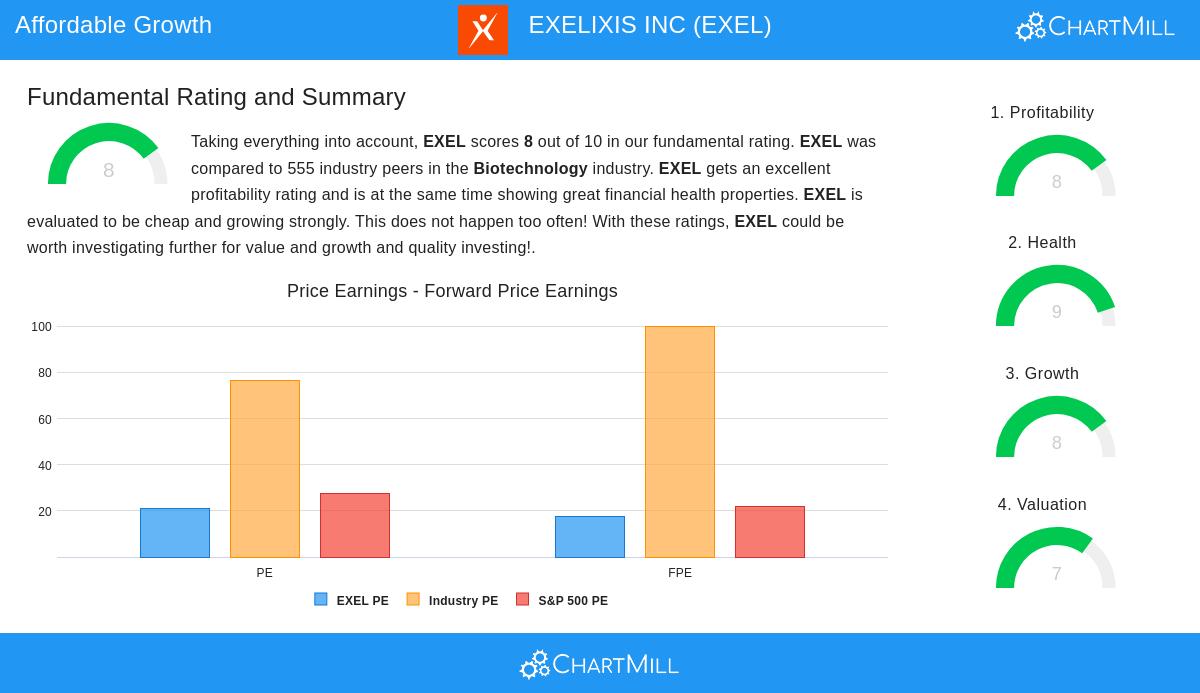

- Attractive Multiples: Despite its growth, EXEL trades at a Price/Earnings (P/E) ratio of 20.98, which is below the industry average and cheaper than 95% of its biotechnology peers.

- Forward P/E of 17.39 suggests the stock remains reasonably priced relative to future earnings expectations.

- Enterprise Value to EBITDA and Price/Free Cash Flow ratios also indicate the stock is undervalued compared to industry standards.

Financial Health & Profitability

- No Debt: EXEL has no outstanding debt, contributing to a strong financial position.

- High Profit Margins: The company boasts a 27.99% profit margin and a 35.43% operating margin, ranking among the top performers in its sector.

- Strong Returns: Return on Assets (22.68%) and Return on Equity (30.20%) are well above industry averages.

For a deeper look at EXEL’s fundamentals, review the full analysis report.

Our Affordable Growth screener lists more stocks with similar characteristics and is updated daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own research before making investment decisions.