EQUINOR ASA-SPON ADR (NYSE:EQNR) surfaced in our Peter Lynch-inspired screen as a potential candidate for growth-at-a-reasonable-price (GARP) investors. The company, a key player in oil, gas, and renewable energy, demonstrates a balance of profitability, financial health, and valuation that aligns with Lynch’s investment principles. Below, we examine why EQNR fits this strategy.

Key Metrics Supporting EQNR’s GARP Profile

- Earnings Growth: EQNR’s EPS has grown at an average annual rate of 16.8% over the past five years, meeting Lynch’s criteria for sustainable growth (15–30%).

- Attractive Valuation: With a PEG ratio of 0.48 (well below Lynch’s threshold of 1), the stock appears undervalued relative to its growth. The P/E ratio of 8.1 further underscores its reasonable pricing.

- Strong Profitability: The company’s return on equity (ROE) of 19.1% exceeds the 15% minimum Lynch favored, reflecting efficient use of shareholder capital.

- Healthy Balance Sheet: A debt-to-equity ratio of 0.50 and a current ratio of 1.37 indicate manageable leverage and liquidity, aligning with Lynch’s emphasis on financial stability.

Fundamental Highlights

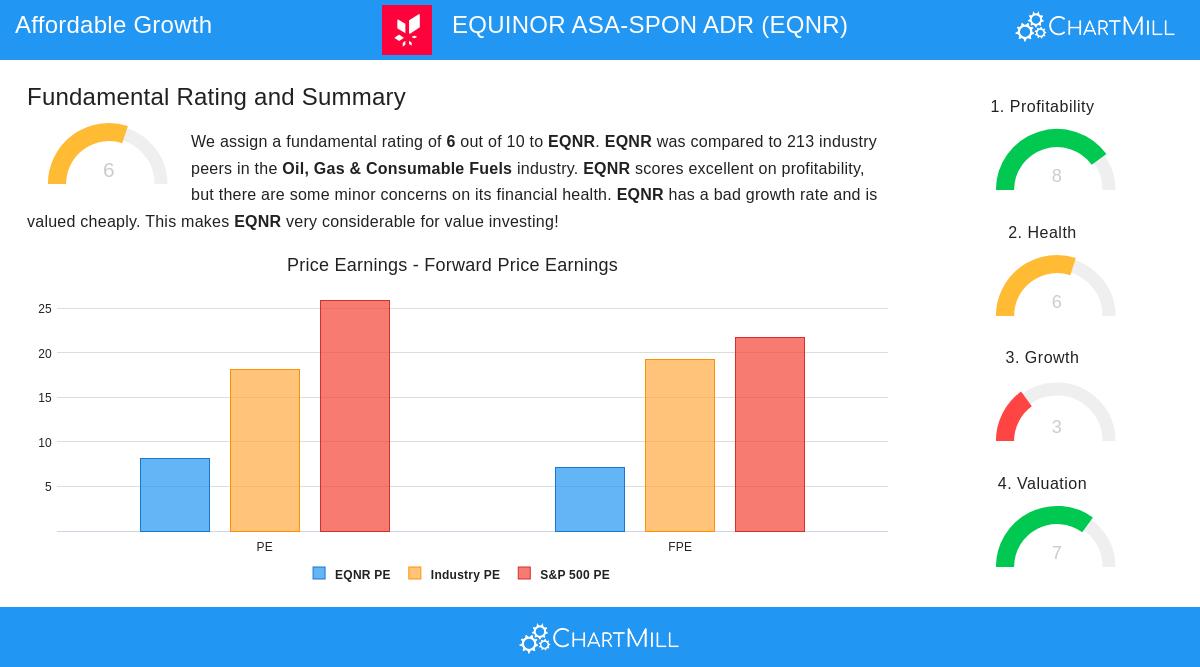

EQNR’s fundamental report rates it 6/10, noting strengths in profitability and valuation but flagging slower future growth expectations. Key takeaways:

- Profitability: High ROE (19.1%) and ROIC (24.3%) outperform most industry peers.

- Dividend: A yield of 5.9% is attractive, though sustainability concerns exist due to a high payout ratio.

- Valuation: Trading at a discount to both industry and S&P 500 averages on P/E and EV/EBITDA metrics.

Risks to Consider

- Energy Sector Volatility: Oil prices and regulatory shifts could impact performance.

- Dividend Sustainability: Earnings growth lags dividend growth, raising payout concerns.

- Slowing Growth: Revenue and EPS growth are projected to decelerate.

Our Peter Lynch Strategy screener lists more stocks meeting these criteria.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own analysis before making investment decisions.