Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with steady growth at fair prices, commonly known as the Growth at a Reasonable Price (GARP) method. The approach prioritizes strong fundamentals, consistent profits, and controlled debt, steering clear of overly hyped or rapidly expanding businesses that might not last. By looking for firms with stable earnings growth, healthy financials, and good valuations, Lynch’s strategy seeks to identify long-term performers capable of delivering steady returns.

One company that aligns with this model is EnerSys (NYSE:ENS), a leader in stored energy solutions for industrial use. The stock checks multiple boxes from the Peter Lynch criteria, positioning it as a possible choice for GARP-focused investors.

How EnerSys Matches the Peter Lynch Criteria

-

Steady Earnings Growth

Lynch preferred companies with reliable earnings growth, usually between 15% and 30% per year. EnerSys has achieved a five-year EPS growth rate of 16.84%, fitting comfortably within this range. This reflects stable, sustainable progress rather than erratic surges. -

Fair Valuation (PEG Ratio ≤ 1)

The PEG ratio (Price/Earnings to Growth) is a critical measure in Lynch’s strategy, balancing price and growth. A PEG under 1 suggests a stock may be undervalued relative to its earnings potential. EnerSys’s PEG ratio of 0.52, significantly below the benchmark, implies the stock is priced favorably compared to its growth outlook. -

Solid Profitability (ROE > 15%)

Return on Equity (ROE) gauges how well a company turns equity into profits. Lynch sought ROE above 15%, and EnerSys meets this with an 18.98% ROE, showing efficient use of shareholder capital. -

Stable Balance Sheet (Debt/Equity < 0.6)

Financial soundness is key in Lynch’s framework. EnerSys holds a Debt/Equity ratio of 0.57, under the 0.6 limit, reflecting a cautious approach to borrowing. -

Strong Liquidity (Current Ratio ≥ 1)

The Current Ratio evaluates short-term financial stability, and EnerSys performs well with a ratio of 2.70, far exceeding the minimum. This signals sufficient resources to cover near-term liabilities.

Key Strengths and Points to Watch

EnerSys’s fundamental report reveals further positives:

- High Profit Margins: The company leads its peers in operating margin (13.37%) and profit margin (10.05%).

- Effective Capital Use: A Return on Invested Capital (ROIC) of 13.74% ranks it among the best in its sector.

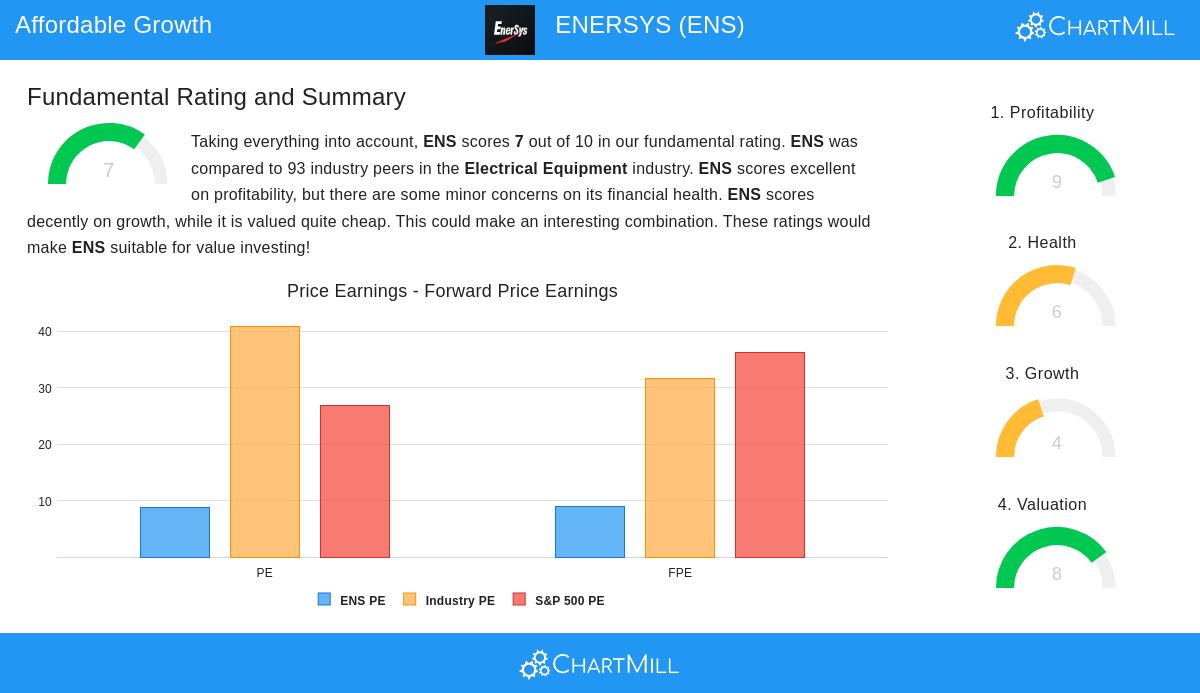

- Reasonable Price: With a P/E of 8.75, EnerSys is more affordable than 94.6% of industry rivals.

Still, there are minor issues, such as an increasing debt/assets ratio and slower projected earnings growth (2.14% per year). These factors deserve attention but don’t overshadow the stock’s broader appeal for patient investors.

Conclusion

EnerSys fits Peter Lynch’s criteria—profitable, fairly priced, and financially stable with consistent growth. For investors interested in more stocks that match this strategy, review the complete Peter Lynch screen results here.

Disclaimer: This article is not investment advice. Conduct your own research or consult a financial advisor before making investment decisions.