DORMAN PRODUCTS INC (NASDAQ:DORM) stands out as a compelling pick for investors seeking long-term growth at a reasonable price (GARP). The company, which supplies automotive replacement and upgrade parts, meets key criteria from Peter Lynch’s investment strategy, balancing solid growth with sound financial health and valuation.

Why DORM Fits the GARP Approach

- Sustainable Growth: DORM has delivered an impressive 5-year average EPS growth of 21.83%, well within Lynch’s preferred range of 15-30%. This indicates steady, manageable expansion rather than overheated growth.

- Attractive Valuation: With a PEG ratio (5Y) of 0.73, the stock is priced below Lynch’s threshold of 1, suggesting it’s undervalued relative to its growth potential.

- Strong Profitability: The company’s Return on Equity (ROE) of 16.05% exceeds Lynch’s 15% benchmark, reflecting efficient use of shareholder capital.

- Healthy Balance Sheet: A Debt/Equity ratio of 0.33 and a Current Ratio of 2.62 highlight financial stability, with manageable leverage and ample liquidity.

Fundamental Strengths

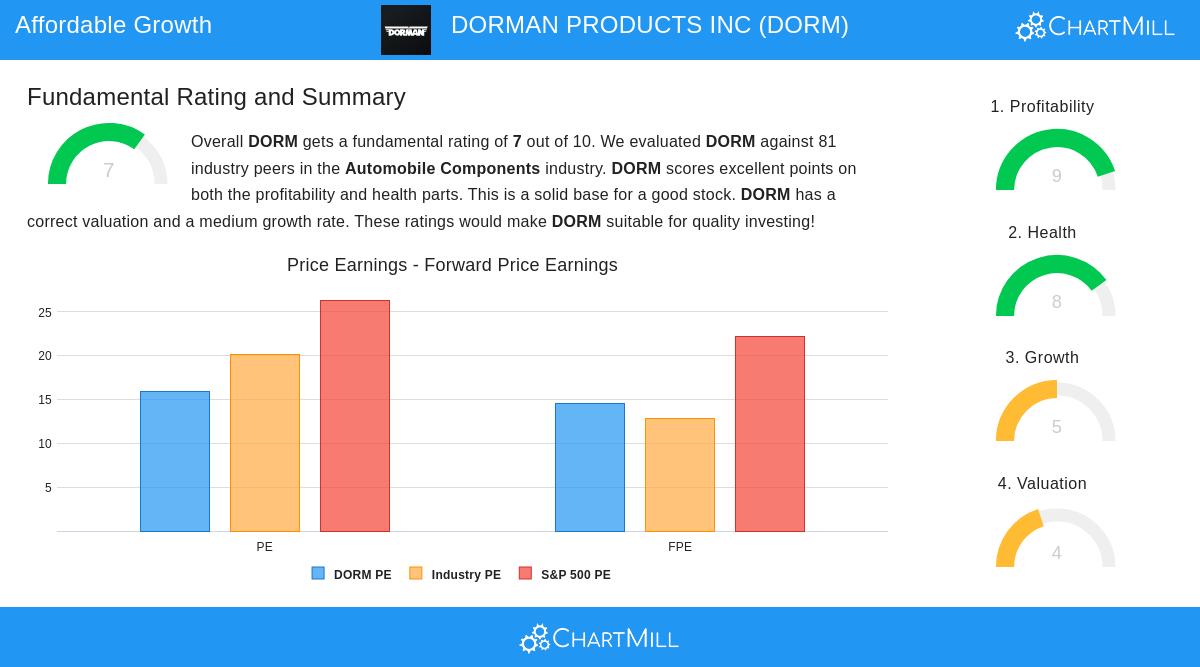

DORM earns a fundamental rating of 7/10, excelling in profitability and financial health. Key takeaways:

- Profit Margins: Gross (40.65%), Operating (15.55%), and Net (10.48%) margins outperform most industry peers.

- Efficiency: ROIC (12.64%) and ROA (8.84%) rank in the top 8% of the sector.

- Valuation: Trading at a P/E of 15.87, DORM is priced below the S&P 500 average (26.31).

For a deeper dive, review the full fundamental analysis here.

Our Peter Lynch Strategy screener lists more stocks aligned with this strategy and updates daily.

Disclaimer

This is not investing advice. The observations here are based on current data, but investors should conduct their own research before making decisions.