In long-term investing, few strategies have earned as much respect as the method supported by Peter Lynch. His system, described in One Up on Wall Street, highlights finding companies with lasting growth, fair valuations, and good financial condition, essentially, businesses that provide growth at a fair price (GARP). Lynch’s structure avoids speculative trends and market timing, instead concentrating on basic measures that show durability and value. This method has shown its worth over time, and it remains a solid tool for investors looking for consistent, long-term returns.

Company Overview

DHT HOLDINGS INC (NYSE:DHT) runs a group of crude oil tankers, mainly Very Large Crude Carriers (VLCCs), with a worldwide reach. The company’s business plan centers on the ownership and running of these ships, aided by technical management services. With a group of about 28 tankers, DHT has an important part in the international crude oil transportation market, a sector that, while changing, stays vital to global energy supply chains.

Alignment with Peter Lynch Criteria

Lynch’s method needs companies to show controlled growth, good valuation, and financial steadiness. DHT Holdings fits these standards through several main measures:

- Earnings Per Share (EPS) Growth: Over the last five years, DHT has reached an average yearly EPS growth of 16.14%, which matches Lynch’s liking for lasting growth, above his 15% lowest limit but much lower than the 30% top he sets to prevent overheating.

- PEG Ratio: The PEG ratio, which changes the price-to-earnings ratio for growth, is 0.81 for DHT. Lynch liked PEG ratios under 1, as they show that a stock might be priced low compared to its growth chances.

- Debt-to-Equity Ratio: At 0.23, DHT’s debt-to-equity ratio is not only under Lynch’s general limit of 0.6 but also below his stricter choice of 0.25, showing a careful capital structure with little need for debt.

- Current Ratio: DHT’s current ratio of 2.33 is higher than Lynch’s need of 1, showing good short-term cash flow and the skill to easily meet its duties.

- Return on Equity (ROE): With an ROE of 17.48%, DHT goes beyond Lynch’s 15% mark, showing good use of equity and firm profitability.

These measures together imply that DHT is not growing without care but at a steady speed, with a valuation that does not overvalue its future possibility. This middle ground is key to Lynch’s thinking, as it lowers investment risk while still getting growth.

Fundamental Health and Performance

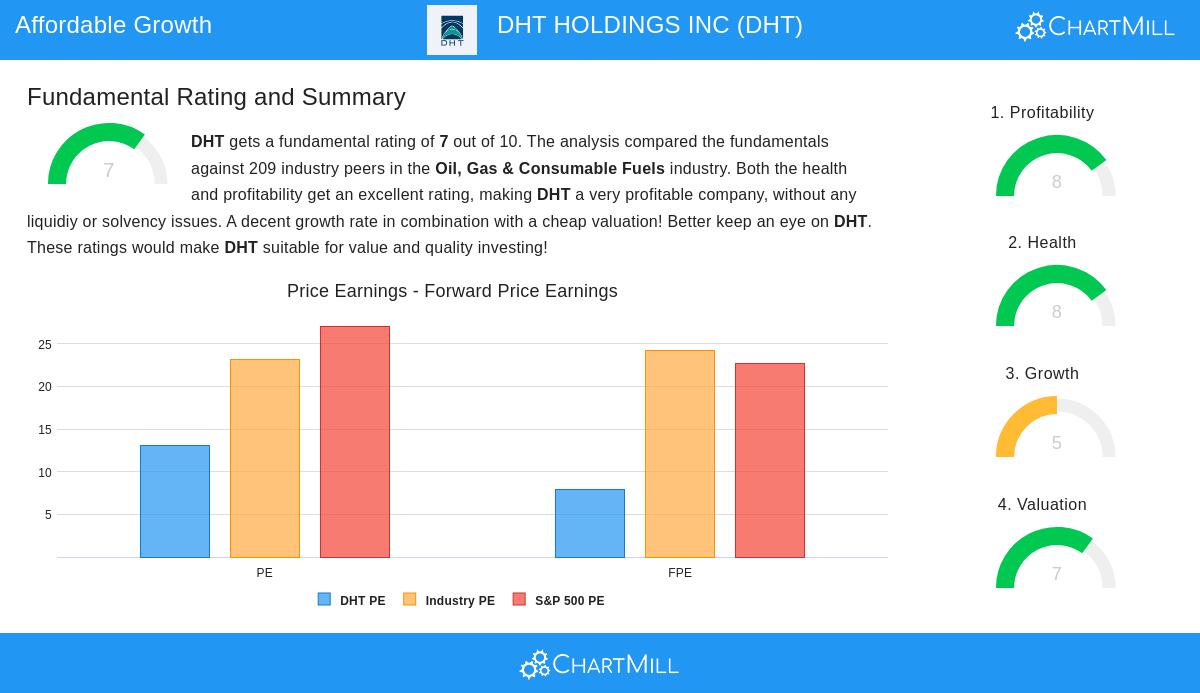

A look at DHT’s wider basic profile supports its appeal. The company has a basic rating of 7 out of 10, putting it well in the oil, gas, and consumable fuels industry. Main strong points include:

- Profitability: DHT does very well in profitability measures, with a high profit margin of 36.58% and good returns on assets and equity, doing better than most industry rivals.

- Financial Health: The company keeps a firm solvency position, shown by a good Altman-Z score and low debt amounts compared to cash flow. Its cash flow is also better, with current and quick ratios much above industry averages.

- Valuation: DHT seems priced low on several points, including a forward P/E ratio of 7.90, which is under both industry and S&P 500 averages. This hints at chance for price growth as the market sees its value.

- Dividend Yield: Giving a yield of 6.65%, DHT gives an income part, though investors should know that the payout ratio is high, which might influence sustainability if earnings change.

For a complete breakdown, readers can see the full fundamental analysis report.

Growth Path and Outlook

While past income growth has been moderate, analysts forecast a speed-up in both income and earnings over the next years, with EPS expected to grow at over 20% each year. This expected gain, joined with the company’s firm operational base, places DHT as a possibility for continued importance and results in the energy sector. Lynch’s method values such forward movement, if it is supported by firm basics, a point that DHT seems to meet.

Conclusion

DHT Holdings shows a strong case for investors matching the GARP ideas of Peter Lynch. It joins fair growth with good valuation and financial condition, lowering downside risk while giving contact with global energy infrastructure. As with any investment, careful study is needed, especially given the changing nature of the shipping industry and wider economic factors that might affect crude oil demand.

For those wanting to find other companies that meet similar standards, the Peter Lynch strategy screen gives more investment options that suit this careful method.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making any investment decisions.