DR HORTON INC (NYSE:DHI) - A Strong Contender for Long-Term Growth Investors

By Mill Chart

Last update:

DR HORTON INC (NYSE:DHI) stands out as a potential candidate for investors seeking long-term growth at a reasonable price. The company meets key criteria from Peter Lynch’s investment strategy, combining solid earnings growth, strong profitability, and a healthy balance sheet—all while trading at an attractive valuation.

Why DHI Fits the Peter Lynch Strategy

- Earnings Growth: DHI has delivered an impressive 5-year average EPS growth of 27.63%, well above the 15% minimum threshold Lynch prefers. While recent earnings have softened, the long-term trend remains strong.

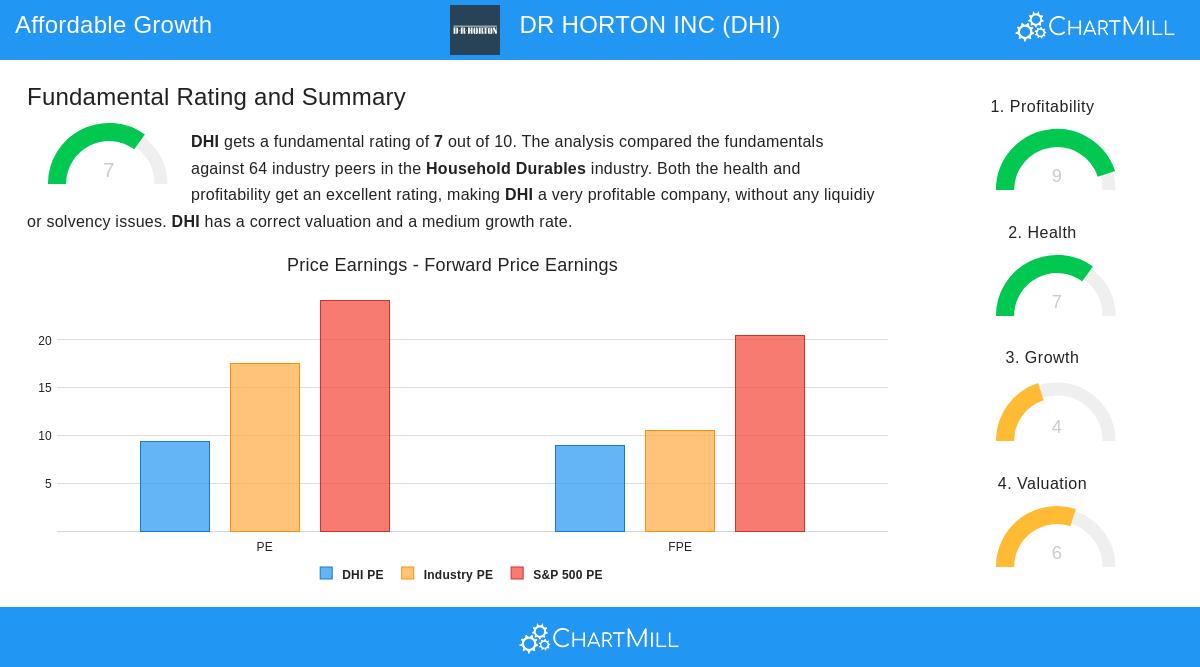

- Reasonable Valuation: The stock trades at a P/E ratio of 9.37, below both the industry and S&P 500 averages. Its PEG ratio (factoring in growth) is also favorable, indicating the stock is not overpriced relative to its earnings potential.

- Strong Profitability: With a Return on Equity (ROE) of 17.64%, DHI outperforms most peers in the household durables sector. Margins are healthy, with operating and profit margins ranking among the best in the industry.

- Financial Health: The company maintains a conservative debt profile, with a Debt/Equity ratio of 0.27, well below Lynch’s preferred threshold of 0.6. Liquidity is also robust, with a current ratio of 6.71, ensuring short-term obligations are easily covered.

Fundamental Highlights

DHI earns a solid 7/10 in our fundamental analysis, scoring particularly well in profitability and financial health. Key strengths include:

- High ROIC (13.95%) and consistent cash flow generation.

- A track record of dividend growth, with a 14.84% annual increase over the past decade.

- A strong Altman-Z score (5.51), indicating low bankruptcy risk.

For a deeper dive, review the full fundamental report on DHI.

Our Peter Lynch Strategy screener lists more stocks that fit this investment approach and is updated regularly.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own analysis before making investment decisions.

127.29

-2.34 (-1.81%)

Find more stocks in the Stock Screener

DHI Latest News and Analysis

12 days ago - ChartmillDR HORTON INC (NYSE:DHI) – A Strong Candidate for GARP Investors

12 days ago - ChartmillDR HORTON INC (NYSE:DHI) – A Strong Candidate for GARP InvestorsDR Horton (DHI) offers strong growth, solid profitability, and an attractive valuation, making it a standout for GARP investors following Peter Lynch's principles.