Peter Lynch’s investment strategy, described in One Up on Wall Street, centers on finding companies with consistent growth at fair prices. His method combines aspects of growth and value investing, focusing on financial stability, earnings strength, and reasonable debt. The approach steers clear of overly hyped or rapidly expanding businesses, preferring those with steady, reliable progress. Important measures include a PEG ratio under 1, a debt-to-equity ratio below 0.6, a current ratio over 1, and a return on equity (ROE) above 15%. These filters help identify firms that are both financially healthy and priced well compared to their growth prospects.

How Donnelley Financial Solutions (NYSE:DFIN) Matches the Lynch Approach

1. Consistent Earnings Growth

Lynch looks for companies with earnings per share (EPS) growth between 15% and 30% over five years, balancing speed and sustainability. Donnelley Financial Solutions (DFIN) fits this with a 24.57% annualized EPS growth over the past five years. This pace suggests the company has grown effectively without overreaching, fitting Lynch’s "stalwart" classification.

2. Fair Valuation Using PEG Ratio

The PEG ratio (Price/Earnings to Growth) is key in Lynch’s strategy, adjusting the P/E ratio for growth. A PEG under 1 suggests the stock may be undervalued relative to its growth. DFIN’s PEG of 0.59 falls within this range, indicating the market may not fully reflect its earnings potential. This matches Lynch’s idea of "buying growth at a sensible price."

3. Sound Financial Position

Lynch avoids companies with high debt, preferring those with debt-to-equity ratios below 0.6. DFIN’s ratio of 0.44 shows a cautious approach to borrowing, lowering risk and maintaining flexibility. Its current ratio of 1.24 also confirms it can meet short-term obligations, another Lynch priority.

4. Strong Profitability (ROE > 15%)

ROE measures how well a company turns shareholder equity into profits. DFIN’s ROE of 21.46% not only exceeds Lynch’s 15% benchmark but also places it in the top 12% of its industry. This signals efficient capital use, a trait Lynch linked to lasting success.

Additional Strengths

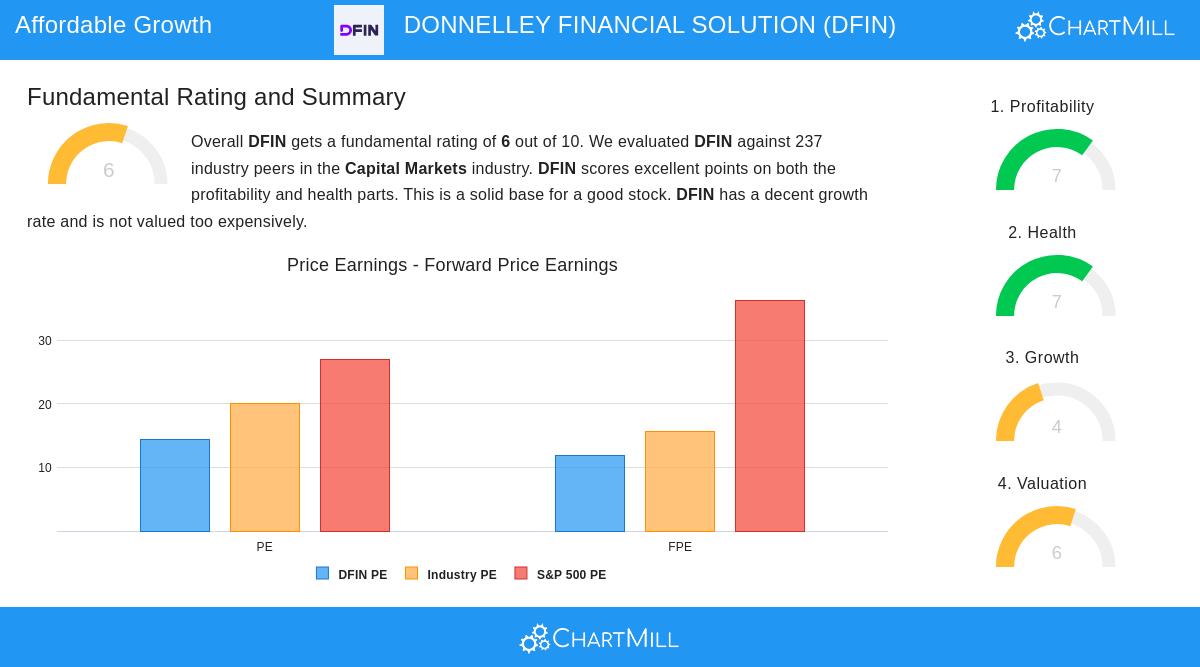

ChartMill’s fundamental report gives DFIN a score of 6/10, noting its strong profitability and financial health. Key points:

- Profitability: High ROE and Return on Invested Capital (ROIC) of 17.70%, beating 93% of industry peers.

- Valuation: Trades at a P/E of 14.4, below the S&P 500 average (26.99), with a forward P/E of 11.82, hinting at potential upside.

- Growth Outlook: Analysts forecast 13.99% annual EPS growth, with revenue growth expected to pick up.

Points to Watch

While DFIN meets Lynch’s main criteria, its revenue dropped 1.92% YoY, and EPS growth fell 7.44% last year. Still, improving margins and a solid industry standing suggest a rebound is possible.

Finding Similar Opportunities

For investors looking for comparable stocks, this Peter Lynch screen filters for stocks matching these standards. DFIN’s presence highlights its fit with a disciplined, long-term growth plan.

Disclaimer: This analysis is not investment advice. Do your own research or consult a financial advisor before making decisions.