CIA ENERGETICA DE-SPON ADR (NYSE:CIG) surfaced in our Peter Lynch-inspired screen as a potential candidate for growth at a reasonable price (GARP) investors. The Brazilian utility company demonstrates a mix of solid historical growth, strong profitability, and an attractive valuation. Below, we examine why CIG fits the criteria for long-term investors seeking sustainable growth without overpaying.

Key Strengths

- Earnings Growth: Over the past five years, CIG has delivered an impressive average annual EPS growth of 26.4%, comfortably within Lynch’s preferred range of 15-30%. This suggests the company has expanded earnings at a sustainable pace.

- Profitability: With a Return on Equity (ROE) of 25.1%, CIG outperforms 95% of its peers in the electric utilities industry. High ROE indicates efficient use of shareholder capital.

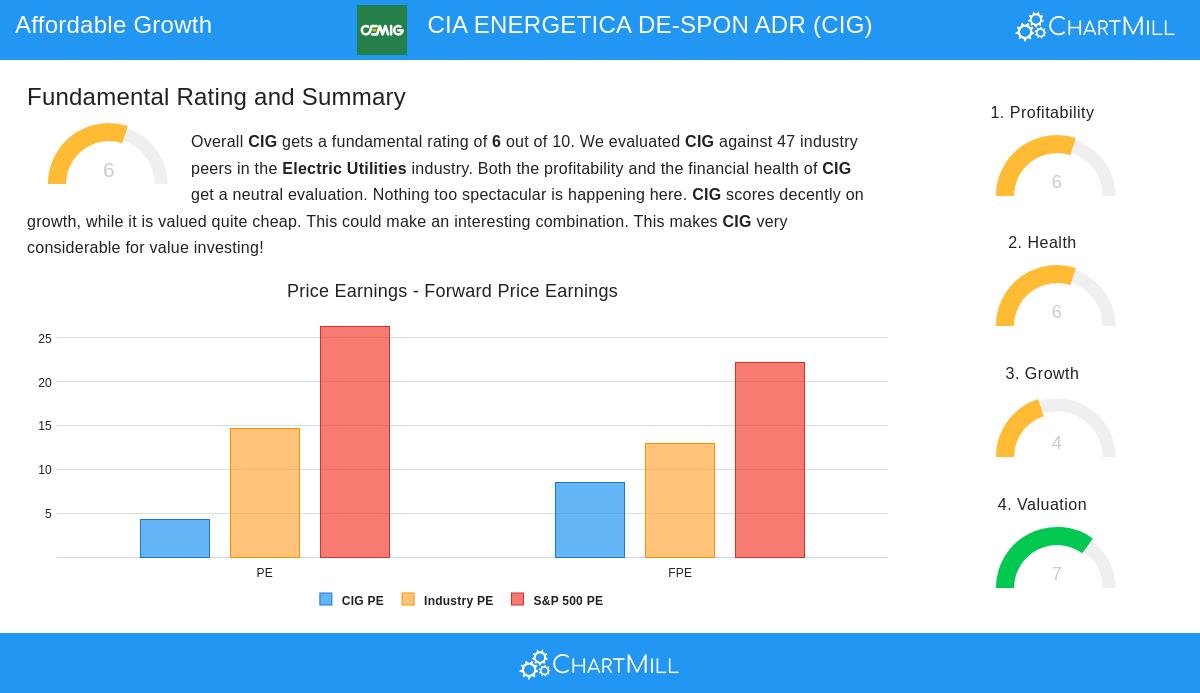

- Valuation: The stock trades at a P/E ratio of 4.3, well below both the industry average (14.7) and the S&P 500 (26.3). Its PEG ratio (5Y) of 0.16—far below Lynch’s threshold of 1—suggests the stock is undervalued relative to its growth.

- Financial Health: A Debt/Equity ratio of 0.46 and a Current Ratio of 1.06 reflect a balanced capital structure and adequate liquidity to meet short-term obligations.

Considerations

- Dividend Sustainability: While CIG offers a 3.1% dividend yield, its payout ratio of 61% and recent earnings declines raise questions about long-term sustainability.

- Future Growth Concerns: Analysts expect EPS to decline by 25.5% annually in the coming years, which could pressure performance unless trends reverse.

Fundamental Summary

CIG earns a fundamental rating of 6/10, with strengths in valuation and profitability offset by weaker growth projections. For a deeper dive, review the full fundamental analysis here.

Our Peter Lynch Strategy screener lists more stocks matching these criteria and is updated regularly.

Disclaimer

This is not investment advice. Always conduct your own research before making investment decisions.