BOOT BARN HOLDINGS INC (NYSE:BOOT) emerged from our Peter Lynch-inspired screen as a potential candidate for growth at a reasonable price (GARP) investors. The company demonstrates strong historical growth, solid profitability, and a manageable valuation, aligning well with Lynch’s investment principles. Below, we break down why BOOT stands out.

Key Metrics Supporting BOOT’s GARP Profile

- Earnings Growth: BOOT has delivered an impressive 5-year EPS growth rate of 28.69%, well above the minimum 15% threshold in Lynch’s strategy. While growth is expected to moderate slightly to 13.54% in the coming years, it remains robust.

- Reasonable Valuation: The PEG ratio (5-year) of 0.97 suggests the stock is reasonably priced relative to its growth, fitting Lynch’s preference for PEG ratios below 1.

- Strong Profitability: With a return on equity (ROE) of 16.01%, BOOT exceeds Lynch’s 15% benchmark, indicating efficient use of shareholder capital.

- Healthy Balance Sheet: A debt-to-equity ratio of 0.01 and a current ratio of 2.45 reflect a financially stable company with ample liquidity to meet short-term obligations.

Fundamental Snapshot

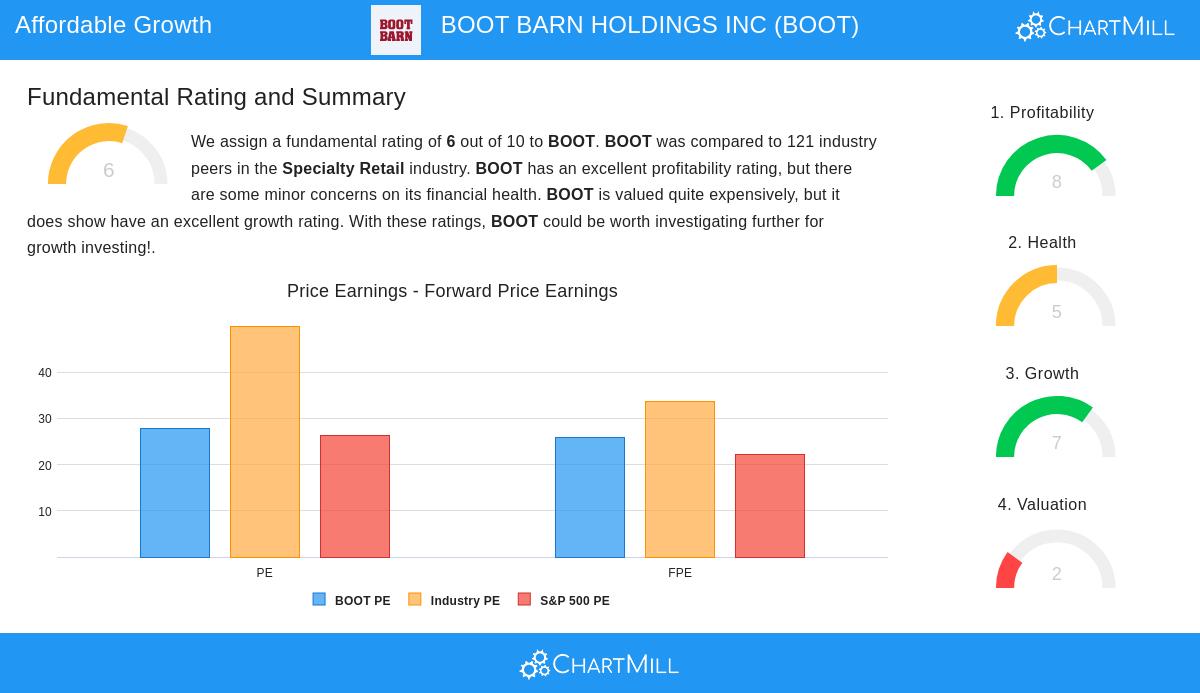

Our fundamental analysis report rates BOOT a 6 out of 10, highlighting its strengths in profitability and growth, though noting some concerns about valuation. Key takeaways:

- Profit Margins: BOOT’s operating margin of 12.53% and profit margin of 9.47% rank in the top tier of its industry.

- Revenue Growth: Historical revenue growth of 17.71% annually underscores the company’s ability to expand its business.

- Valuation: While the P/E ratio of 27.87 is elevated, the PEG ratio suggests growth may justify the premium.

For investors seeking similar opportunities, our Peter Lynch Strategy screener provides a curated list of stocks meeting these criteria.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should always conduct your own analysis before making investment decisions.