Value investing remains one of the most enduring investment strategies, focusing on identifying stocks trading below their intrinsic worth. The approach, pioneered by Benjamin Graham and later refined by investors like Warren Buffett, emphasizes purchasing securities that appear undervalued by the market based on fundamental analysis. This method relies on metrics such as price-to-earnings ratios, profitability margins, financial health indicators, and growth projections to find opportunities where the market price does not fully reflect a company’s true value. By targeting firms with strong fundamentals that are temporarily priced below their fair value, investors aim to achieve returns as the market corrects its mispricing over time.

BIOMARIN PHARMACEUTICAL INC (NASDAQ:BMRN) is a noteworthy candidate from a value investing perspective, particularly when evaluated through a fundamental lens. The company, which focuses on developing therapies for rare genetic diseases, demonstrates several characteristics that align with the criteria value investors typically prioritize. A detailed fundamental analysis report highlights its ratings across valuation, health, profitability, and growth, key pillars in assessing whether a stock is undervalued yet fundamentally sound.

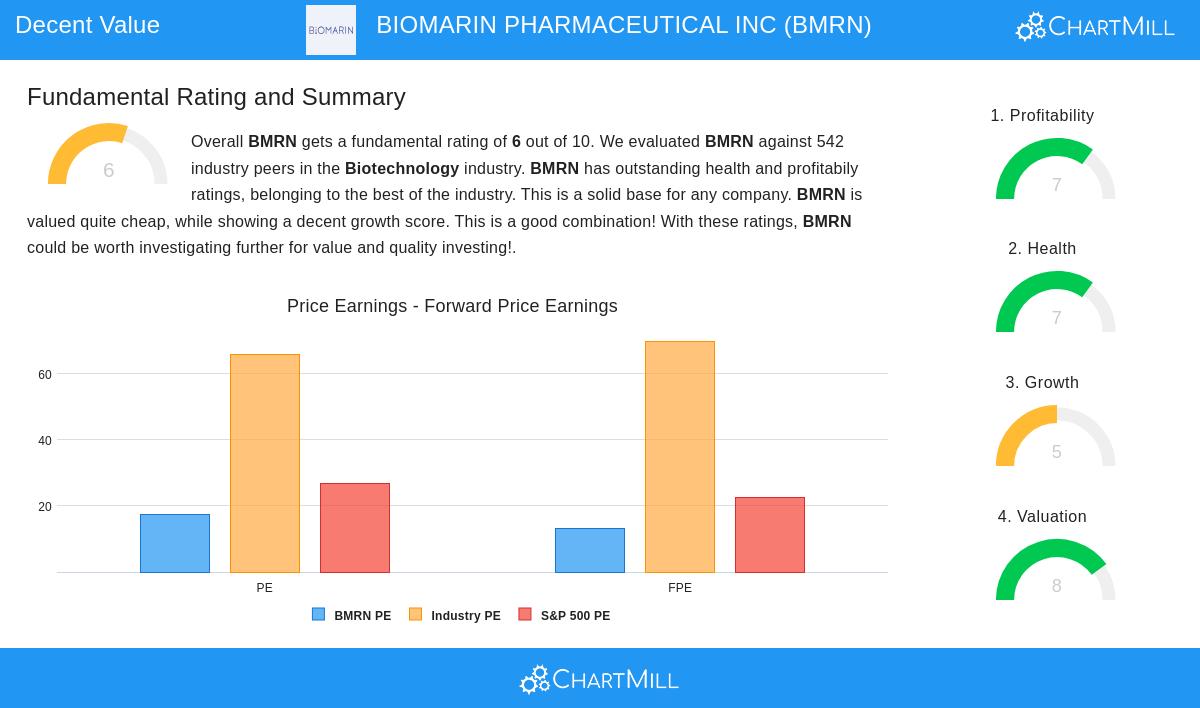

Valuation Strengths Support Undervaluation Thesis A core tenet of value investing is identifying stocks trading at a discount to their intrinsic value, often measured through valuation multiples. BioMarin’s valuation rating of 8 out of 10 indicates it is priced attractively relative to both its industry and broader market benchmarks. Notably, its forward price-to-earnings ratio of 13.29 is not only below the industry average but also cheaper than 95% of its biotechnology peers. This is significant because value investors seek margins of safety, buying at a price sufficiently below estimated intrinsic value to allow for errors in estimation or market volatility. The company’s enterprise value to EBITDA and price-to-free-cash-flow ratios further support this undervaluation, trading at levels more favorable than nearly 96% of industry competitors. Such metrics are critical in value investing, as they suggest the market may be overlooking BioMarin’s earnings potential and cash generation capabilities.

Strong Financial Health Reduces Downside Risk Financial health is another cornerstone of value investing, as it ensures a company can withstand economic downturns without jeopardizing its operations. BioMarin scores a solid 7 out of 10 in this category, with particularly strong solvency and liquidity indicators. The company’s Altman-Z score of 6.09 signals a low risk of bankruptcy, outperforming almost 79% of its peers. Additionally, its debt-to-free-cash-flow ratio of 0.86 is exceptional, indicating it could pay off all outstanding debt in less than a year using its cash flows. This level of financial stability is vital for value investors, as it provides a buffer against operational setbacks and economic cycles, aligning with the strategy’s emphasis on capital preservation and reduced risk.

High Profitability Supports Intrinsic Value Profitability metrics are essential in value investing because they reflect a company’s ability to generate returns on invested capital, a key component of intrinsic value. BioMarin earns a profitability rating of 7 out of 10, with standout performance in margins and returns. Its profit margin of 21.45% and operating margin of 27.07% rank in the top percentiles of the biotechnology industry, outperforming over 94% and 96% of peers, respectively. High margins like these often indicate pricing power, efficient operations, and a competitive moat, all traits value investors favor when estimating a company’s durable earning power. Strong returns on assets and equity further validate the company’s effective deployment of capital, reinforcing the thesis that its current market price may not fully capture its profit-generating capability.

Growth Prospects Enhance Long-Term Appeal While pure value investing sometimes prioritizes low valuation over growth, combining both can lead to superior returns, an approach sometimes termed "growth at a reasonable price." BioMarin’s growth rating of 5 out of 10 reflects a mixed but promising trajectory. Past growth has been strong, with revenue increasing 18.36% over the last year and earnings per surging 139.01%. Looking ahead, analysts project annual EPS growth of nearly 28.5%, though revenue growth is expected to moderate to around 7.65%. For value investors, this growth profile is important because it suggests the company is not stagnant; future earnings expansions could catalyze a reevaluation by the market, narrowing the gap between price and intrinsic value.

Conclusion BioMarin Pharmaceutical represents a noteworthy case study in value investing principles applied to the biotechnology sector. Its combination of low valuation multiples, strong financial health, high profitability, and respectable growth prospects positions it as a potential undervalued opportunity. These attributes align closely with the value investing strategy’s focus on buying fundamentally sound companies at a discount to their true worth, thereby offering a margin of safety and potential for capital appreciation as the market recognizes their intrinsic value.

For investors interested in exploring similar opportunities, more results from the "Decent Value" screen can be found here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making any investment decisions.