BAKER HUGHES CO (NASDAQ:BKR) emerged from our Peter Lynch-inspired screen as a potential candidate for long-term investors seeking growth at a reasonable price. The company, a provider of oilfield services and energy technology solutions, meets several key criteria for sustainable growth and sound financial health.

Why BKR Fits the GARP Approach

- Strong Earnings Growth: BKR has delivered a 5-year average EPS growth of 23.35%, comfortably within Lynch’s preferred range of 15-30%. This indicates steady, sustainable expansion rather than overheated growth.

- Attractive Valuation: With a PEG ratio (5-year) of 0.67, well below the threshold of 1, the stock appears reasonably priced relative to its growth trajectory.

- Healthy Profitability: The company’s Return on Equity (ROE) stands at 17.17%, exceeding Lynch’s 15% benchmark, reflecting efficient use of shareholder capital.

- Conservative Leverage: A Debt/Equity ratio of 0.35 suggests a balanced capital structure, aligning with Lynch’s preference for low debt.

- Liquidity Check: The Current Ratio of 1.34 indicates sufficient short-term financial flexibility.

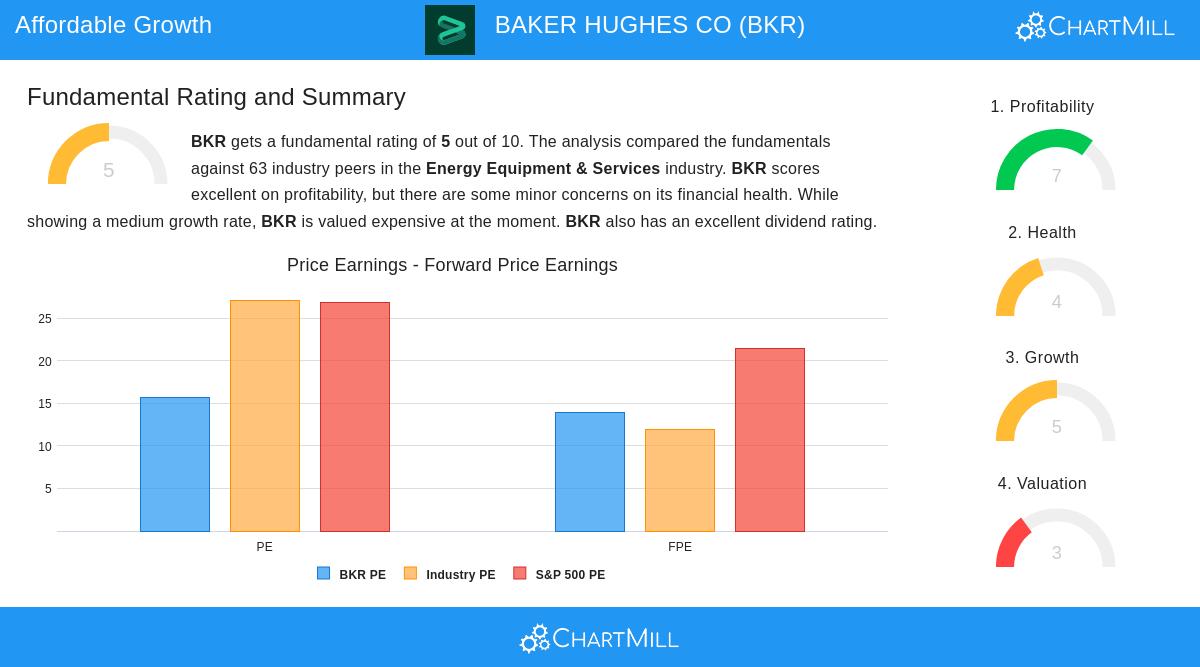

Fundamental Snapshot

Our analysis rates BKR 5/10 overall, with strengths in profitability (7/10) and dividends (7/10), though liquidity (4/10) and valuation (3/10) show room for improvement. Key positives include:

- ROE and ROIC above industry averages.

- Stable dividend history with a 10-year track record and a sustainable payout ratio of 29%.

- Improving margins, particularly in operating and profit margins.

For a deeper dive, review the full fundamental report.

The Peter Lynch Strategy screener updates daily with more candidates fitting this disciplined approach.

Disclaimer

This is not investing advice. Always conduct your own research before making investment decisions.