Value investing remains one of the most lasting strategies in equity markets, focusing on finding companies trading below their intrinsic worth while keeping solid basic fundamentals. This method, started by Benjamin Graham and later improved by investors like Warren Buffett, stresses buying securities with a margin of safety, where market price sits meaningfully below calculated fair value, to protect against estimation mistakes or market swings. Stocks chosen through this view usually show strong profitability, healthy balance sheets, reasonable growth outlooks, and, importantly, appealing valuations compared to their peers and historical averages.

BARRICK MINING CORP (NYSE:B) appears as a noteworthy candidate under this structure, especially after a screen for "decent value" traits, prioritizing good valuation numbers without giving up financial health, profitability, or growth. The company’s latest fundamental analysis report shows an overall rating of 7 out of 10, pointing to a balanced profile with several notable qualities important to value-focused investors.

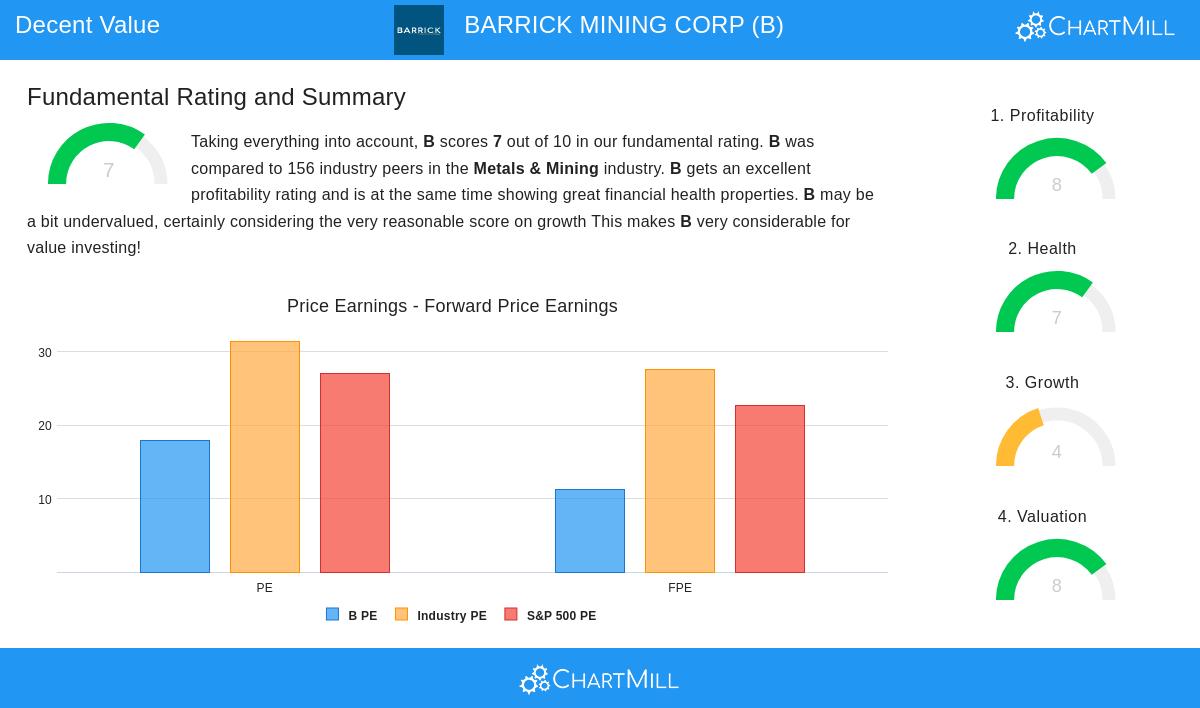

Valuation Metrics

Barrick’s valuation numbers are especially notable, scoring 8 out of 10 and placing it well against industry peers and wider market indices:

- Price-to-Earnings (P/E) Ratio: At 17.98, it is cheaper than 83.33% of metals and mining companies, even though the industry average is near 31.46.

- Forward P/E Ratio: 11.25 is much lower than the S&P 500 average of 22.69, hinting at expectations of continued earnings.

- Enterprise Value to EBITDA: The company is more affordable than 87.82% of industry rivals based on this measure.

- PEG Ratio: Accounting for growth, the low PEG shows the stock isn’t overvalued relative to its earnings path.

These numbers are key to value investing, as they help spot differences between market price and intrinsic value. A lower P/E, along with strong forward earnings estimates, often means the market has not fully priced in the company’s earnings potential or stability.

Financial Health

Scoring 7 out of 10 for financial health, Barrick shows strength through several solvency and liquidity measures:

- Debt Management: A debt-to-equity ratio of 0.19 shows a careful capital structure, with less leverage than many industry peers.

- Liquidity Position: Current and quick ratios of 3.21 and 2.53, respectively, show enough short-term asset coverage for liabilities, doing better than two-thirds of the sector.

- Free Cash Flow: A debt-to-FCF ratio of 2.76 implies the company could pay off all outstanding debt in under three years using current cash flow levels.

For value investors, financial health lowers the chance of permanent capital loss. A solid balance sheet makes sure the company can survive economic slumps, operational issues, or times of low commodity prices without risking its ongoing activities or dividend payments.

Profitability Strengths

With a profitability rating of 8 out of 10, Barrick does well in creating returns from its assets and operations:

- Margin Performance: Operating margin of 39.96% and profit margin of 19.99% put it in the top ten percent of its industry.

- Return Metrics: Return on equity (11.13%) and return on invested capital (8.42%) both exceed 75% of sector rivals.

- Historical Consistency: The company has been profitable with positive operating cash flow in each of the last five years.

High profitability is a sign of good value investments, as it often links to lasting competitive edges and efficient management. Steady cash generation backs reinvestment, debt paydown, and shareholder returns, supporting the margin of safety.

Growth Considerations

Even though growth is rated modestly at 4 out of 10, there are positive past trends mixed with careful forward estimates:

- Past Performance: EPS grew 54.9% over the past year and averaged 19.55% yearly in recent years, while revenue rose 16.86% last year.

- Future Expectations: Analysts predict a small EPS growth of 5.71% per year, though revenue might see a slight drop.

While not a high-growth stock, Barrick’s historical growth and profitability suggest it is not shrinking. For value investors, moderate growth together with low valuation multiples can still present appealing risk-adjusted returns, especially when combined with solid fundamentals elsewhere.

Conclusion

Barrick Mining Corp represents a possibly undervalued chance based on a strict value investing structure. Its noteworthy valuation, strong financial health, and high profitability form a profile that fits well with the strategy’s main ideas, looking for margin of safety through numerical strength and operational steadiness. While growth expectations are mild, the company’s ability to create cash, handle debt, and keep industry-leading margins offers a cushion against doubt and matches with long-term value creation.

For investors curious about finding similar chances, more results from the "Decent Value" screen can be found here.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making investment decisions.