If you blinked, you might’ve missed it, the S&P 500 came within a hair’s breadth of a new record high yesterday, buoyed by a surprising rally in tech and financials.

But let’s not kid ourselves: this market is balancing on a knife’s edge, caught between bullish earnings from AI-driven semiconductors and political intrigue surrounding the Fed.

The drama is real, and investors are watching every move like hawks.

Markets Flirt with All-Time Highs – Again

It was a strong close for U.S. equities on Thursday. The S&P 500 gained 0.8% to finish at 6,141.02, brushing up against its all-time high of 6,144.15 set back in February.

The Dow Jones (+0.9%) and Nasdaq (+1.0%) followed suit, fueled by strong showings in tech and financials.

What’s driving this recent strength? A mix of softening fears around trade tensions (yes, Trump’s tariffs again), robust earnings in key sectors, and hopes - however tentative - that the Fed might eventually play ball on rate cuts.

Since the market's April low at 4,982, the S&P has rebounded over 23%, shrugging off geopolitical risks and inflation anxiety like a seasoned prizefighter.

Powell Holds the Line, Trump Sharpening His Knives

Fed Chair Jerome Powell isn’t blinking. Despite mounting pressure from the White House, he reiterated in his latest Congressional appearance that the Fed sees "no rush" to cut rates.

Inflation remains a concern, especially as Trump's tariff policies loom over global supply chains. Powell warned that a significant price bump is expected from these trade moves, and the Fed "can’t ignore that."

Naturally, this didn’t sit well with President Trump. In classic Trump fashion, he teased replacing Powell well ahead of the end of his term in May 2026, saying, "I know three or four people who can do the job." Names like Kevin Warsh and Treasury Secretary Scott Bessent are being floated.

"I know three or four people who can do the job." - President Trump, hinting at the possibility of replacing Fed Chairman Powell.

Wall Street is now betting that a more dovish Fed chair could send the dollar even lower... and it’s already at its weakest in three years, with the euro at 1.1726.

Chips and AI, The Story That Won’t Quit

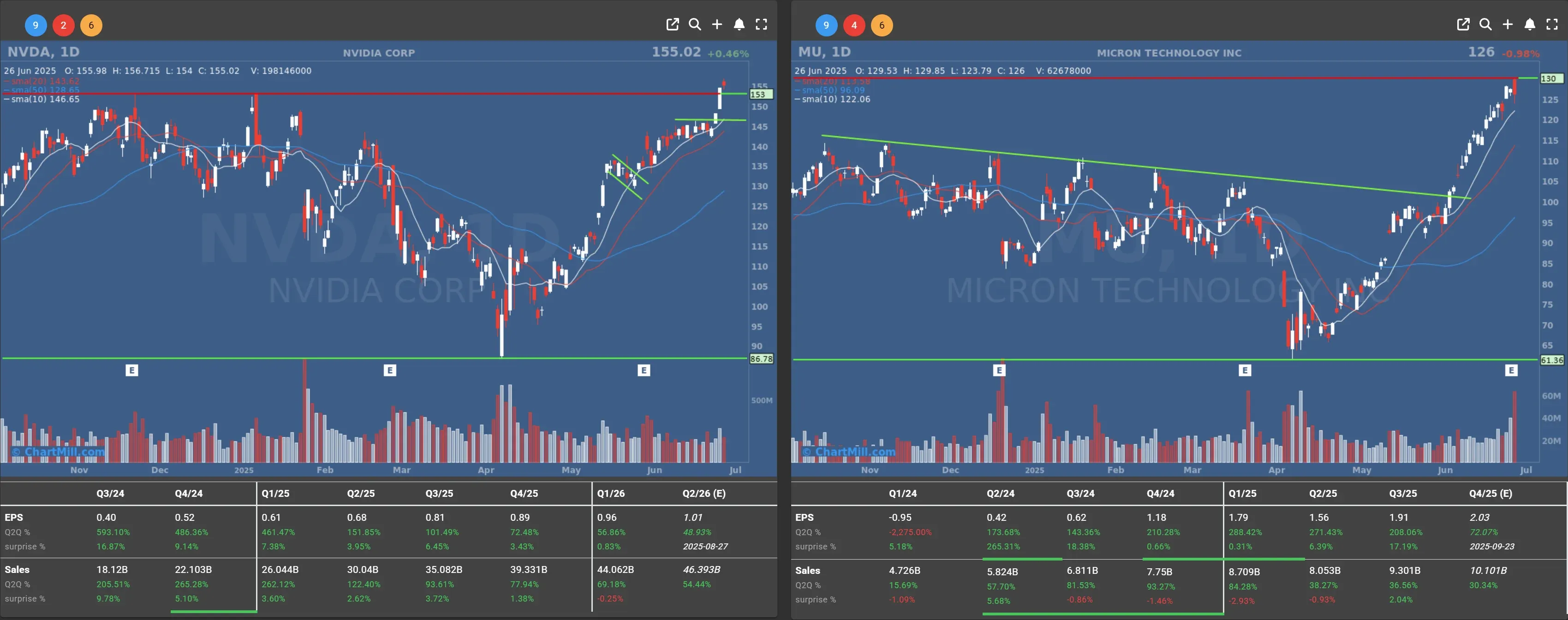

Nvidia (NVDA | +0.46%) continued its seemingly unstoppable climb, hitting a fresh record at $155.02. It now comfortably wears the crown as the most valuable public company in the world.

But let’s give some love to Micron Technology (MU | -0.98%), even if the stock slipped on some profit-taking.

Micron crushed expectations with Q3 revenue jumping 37% YoY to $9.3 billion (vs. $8.85B expected) and EPS of $1.91 (vs. $1.60 expected).

-

The real kicker? Q4 guidance. Micron sees $10.7 billion in sales and $2.50 EPS, both well above consensus.

-

The driver? Surging demand for High Bandwidth Memory (HBM), which is critical for AI models and datacenters.

Still, not everyone’s sold.

While Piper Sandler and JPMorgan upped their price targets to $165, citing strength in HBM and DRAM chips, others like Morgan Stanley's Joseph Moore struck a more cautious tone. His concern? Samsung is staging a comeback in the HBM race with plans for mass-producing HBM4 chips later this year. Micron may be winning now, but the war is far from over.

Economy: Confusing Signals, but Resilient Data

Macro data painted a mixed picture.

The U.S. economy contracted more than expected in Q1 by 0.5% (vs. -0.2% forecast), raising some eyebrows. At the same time, PCE Prices in the United States increased 3.7% in Q1 2025 (consensus at 3.6%).

On the brighter side, durable goods orders surged 16% in May, driven by a 48% jump in transportation equipment.

Initial jobless claims dropped, and the Chicago Fed index ticked up modestly, not exactly a booming economy, but not collapsing either.

Oh, and keep an eye on Friday’s PCE inflation data, the Fed's favorite gauge. That one could stir the pot.

Geopolitics: Europe Tries to Woo Trump, Middle East Tensions Simmer

Trade worries eased a touch after the White House downplayed the July 9 deadline for new EU tariffs, calling it "not crucial." Europe is scrambling to prevent a tariff war, with German Chancellor Merz urging diplomacy over confrontation.

Meanwhile, the uneasy ceasefire between Israel and Iran remains fragile. No news may be good news for now, but investors are keeping one hand near the sell button just in case.

Earnings Highlights: Nike, Worthington Steel, and More

-

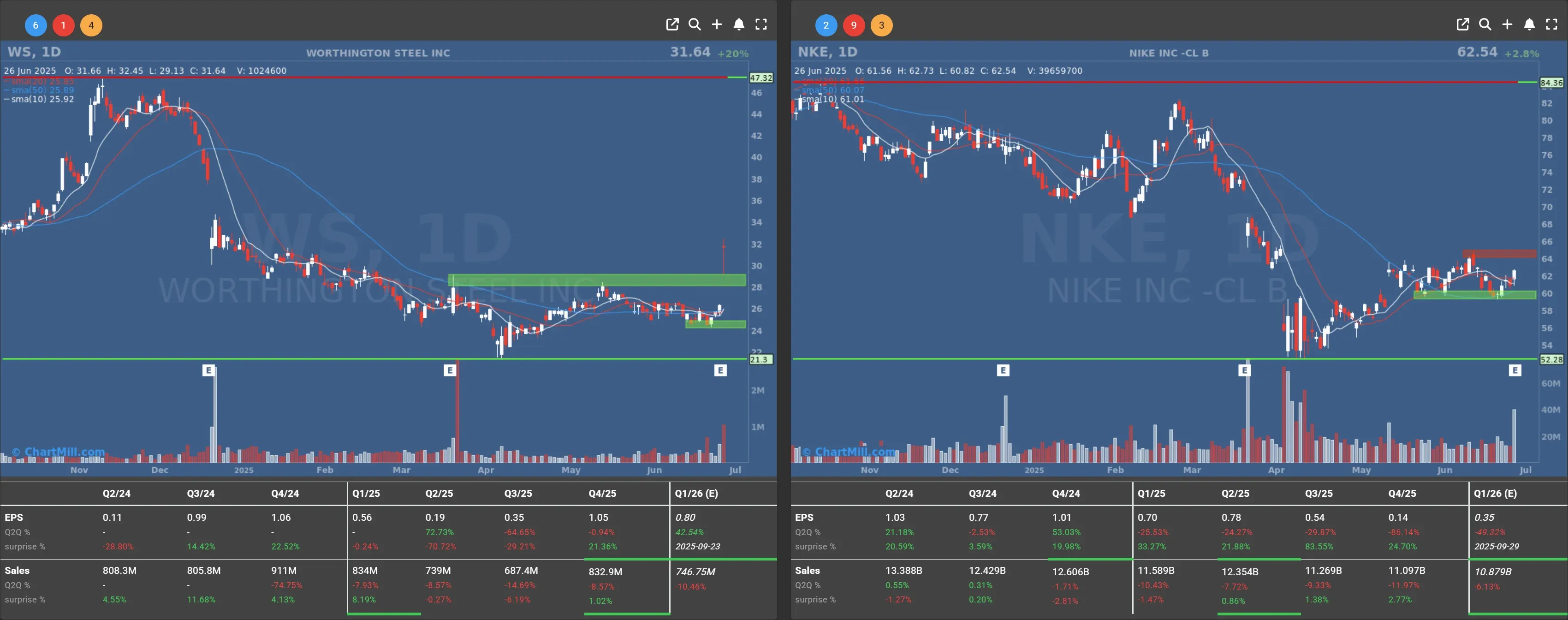

Nike (NKE | +2.81%) posted slightly better-than-feared Q4 results: $0.14 EPS on $11.1B revenue (vs. $0.13 and $10.7B expected). It’s still down 17% YTD, but investors found a sliver of hope in the new CEO’s turnaround plans.

-

Worthington Steel (WS | +20.49%) crushed earnings. No other way to put it.

- Acuity Inc (AYI | +5.81%) also topped expectations.

Notable loser: Unity Software

Unity Software (U | -3.11%) closed more than 3% lower. According to Bank of America, the company's game engine activities are overvalued.

The stock was given an underperform rating with an annual price target of $15.

What I’m Watching Today

-

May PCE inflation data, If it runs hot, rate cut bets might cool fast.

-

The dollar’s slide, already on the ropes, a Powell replacement could send it lower.

-

Semiconductor showdown. Can Micron hold its edge with Samsung back in the game?

-

Nike’s slow rebound. Is there enough momentum to reclaim some YTD losses?

-

Oil prices, after a failed breakout, will geopolitical concerns give it a second wind?

Final Thought:

This market feels like a tightrope walk in high wind, strong earnings and easing trade tensions keep it upright, but Fed politics, inflation jitters, and geopolitical noise are gusting hard. As always, stay nimble.

We're in a bull market... but it sure doesn’t feel like an easy ride.

Kristoff - Co-Founder ChartMill

Next to read: Market Monitor Trends & Breadth Analysis, June 27