A five-day pause on potential U.S. strikes against Iranian energy infrastructure was all it took to flip a sea of red into a splash of green on Monday. Oil fell hard, rates retreated, and cruise and airline stocks surged, while Tesla's Terafab chip ambitions and Berkshire's latest Japan move added some genuine corporate substance to the session.

TACO Is Back on the Menu

Just when it looked like we were staring down the barrel of a full-blown geopolitical meltdown, Donald Trump reminded us once again why traders coined the acronym TACO, Trump Always Chickens Out.

With Asian and European equity markets opening deep in the red and Wall Street futures pointing to a grim start, the president announced on Truth Social that he had instructed the Department of Defense to delay all attacks on Iranian energy infrastructure for five days, following what he described as "productive conversations" with the regime in Tehran.

The timing was almost surgical. The Dow Jones closed Monday 1.4% higher, the Nasdaq gained 1.4%, and the S&P 500 added 1.2%. A full reversal in a matter of hours. If you've been following markets long enough, none of this should surprise you, but it still manages to be remarkable every single time it happens.

There's an important caveat to keep in mind before getting too comfortable, though. Iranian state media flatly denied that any direct talks had taken place between Washington and Tehran, and the confusion deepened when Trump later acknowledged that his envoy had spoken with a senior Iranian official but confirmed it wasn't Supreme Leader Khamenei.

Morgan Stanley analyst Chris Larkin put it well: this rally can only hold if we start seeing tangible results on the geopolitical front. We're still in a headline-driven market.

I'd add that the Strait of Hormuz - the chokepoint through which roughly a fifth of the world's oil and gas flows - remains closed as of Monday, which means the underlying problem hasn't gone away.

Oil and Rates Take a Breather

The market impact of Trump's announcement was most visible in commodities and fixed income. West Texas Intermediate crude for May delivery dropped 10.3% to $88.13 a barrel, having traded as high as $101.67 during the European session earlier in the day. Brent for May delivery shed 10.9%, settling at $99.94, after briefly nearing $115.00.

The 10-year U.S. Treasury yield fell to 4.33%, pulling back from an intraday peak of 4.45%. It directly affects mortgage rates, corporate borrowing costs, and valuation multiples across equity markets.

Meanwhile, gold ended the session above $4,400 after touching $4,100 in early trading, and the euro strengthened back toward the 1.16 handle after dipping to 1.1485.

These swings within a single session underscore just how jittery this market is. Positioning is thin, conviction is limited, and any headline - from either side - can move these markets dramatically.

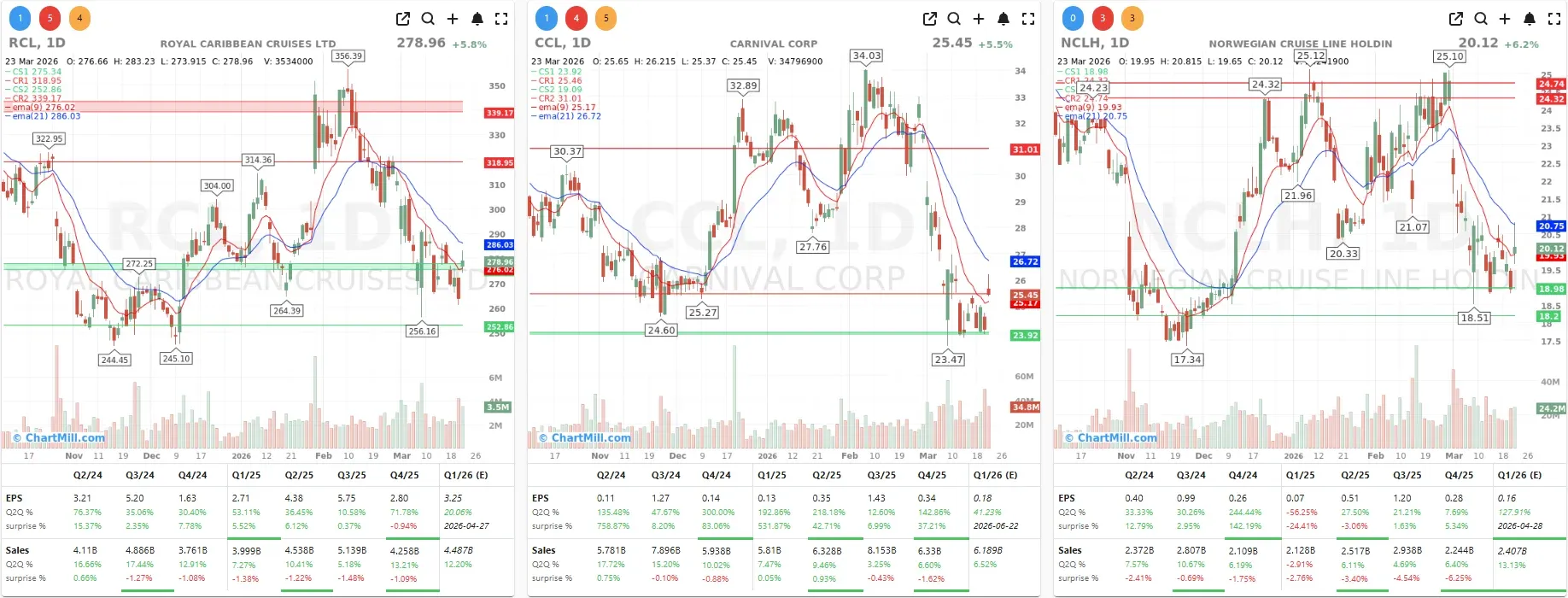

The Cruise and Airline Bounce

The direct beneficiaries of falling oil prices were easy to spot.

Carnival Corporation (CCL | +5.51%), Norwegian Cruise Line (NCLH | +6.17%), and Royal Caribbean (RCL | +5.81%) each surged between 5% and 7% on the back of lower fuel cost expectations. These are the companies that suffer the most when crude spikes, so their bounce was proportional to the relief.

The airline sector joined in too. Delta Air Lines (DAL | +2.66%), American Airlines (AAL | +3.64%), and Southwest Airlines (LUV | +2.39%) each gained between 2% and 4%.

It's worth keeping perspective here: these are largely reactive moves in an ongoing conflict environment. The Strait of Hormuz situation hasn't been resolved. Anyone adding meaningfully to these positions right now is essentially making a bet on diplomatic progress within the next five days. That's not a long runway.

Tesla Plants Its Chip Flag But Questions Linger

Away from the geopolitical noise, Tesla (TSLA | +3.50%) had its own headline moment.

CEO Elon Musk confirmed that Terafab - the joint chip fabrication project between Tesla, SpaceX, and xAI - will be built in Austin, starting with an advanced technology fab near the existing Gigafactory in Travis County.

The $20–25 billion project is described by Musk as "the most epic chip-building exercise in history by far," targeting one terawatt of computing power per year and combining logic design, fabrication, memory production, advanced packaging, and testing under one roof.

The strategic rationale is real enough: Tesla and its sister companies currently rely on external suppliers including Samsung for their AI chips, and Musk has repeatedly flagged supply constraints as a key bottleneck for scaling autonomous driving, robotics, and xAI's Grok models.

That said, I'd urge tempered expectations. No construction timeline was provided at the announcement event, and Tesla's CFO acknowledged that the full Terafab cost is not yet incorporated into Tesla's 2026 capital expenditure plan, which already exceeds $20 billion on its own. The ghost of Dojo lingers here: Tesla disbanded its entire Dojo supercomputer team as recently as August 2025, with Musk calling the project "an evolutionary dead end" before partially reviving the concept just months later under a new orbital computing framing.

Terafab is an ambitious and potentially transformative bet, but it deserves healthy skepticism until shovels are in the ground.

The Terafab announcement was a welcome catalyst for the broader semiconductor equipment sector. Applied Materials (AMAT | +1.32%), KLA Corporation (KLAC | +0.85%), Lam Research (LRCX | +~2%), and ASML Holding (ASML | +3.98%) all moved higher on the news.

Greg Abel Makes His Move in Japan

While the headlines obsessed over geopolitics, Berkshire Hathaway (BRK.B | -0.2%) quietly announced one of the most strategically interesting deals of the year. This marks the first major international initiative led by CEO Greg Abel since he officially assumed the role from Warren Buffett on January 1, 2026.

The deal involves a 2.49% equity stake in Tokio Marine Holdings - Japan's oldest and largest insurance group - alongside a comprehensive 10-year agreement centered on global reinsurance collaboration and joint M&A activity.

For Berkshire, the investment is consistent with a deepening Japan strategy: the five Japanese trading house stakes, built up since 2019, had a combined market value of nearly $41 billion as of mid-March 2026, representing over 13% of Berkshire's total portfolio. In his February shareholder letter, Abel explicitly described the Japanese holdings as comparable to Berkshire's major U.S. positions in importance and long-term value creation potential.

What makes this different from the trading house strategy is the operational dimension. Where Buffett was content to hold stakes passively, Abel is engaging with an active, working partner in one of the most capital-efficient corners of global insurance. If the duo indeed moves forward with joint acquisitions as expected, this could reshape how Berkshire deploys capital over the next decade.

Elliott Takes Aim at Synopsys

The day's other standout mover was Synopsys (SNPS | +2.89%), after the Wall Street Journal reported that activist investor Elliott Investment Management has built a multibillion-dollar stake in the electronic design automation firm and intends to push the company to extract greater value from its software and services portfolio.

Elliott managing partner Jesse Cohn told CNBC that Synopsys is "essential to the global chip industry" and that as AI drives increased chip complexity and capital investment, "Synopsys is uniquely positioned to benefit from this growth."

The firm sees a clear gap between the value Synopsys delivers to its customers and what it captures in financial performance.

Synopsys, valued at over $80 billion, has been a core supplier of chip design software to companies like AMD and Nvidia for decades. Elliott's arrival follows Nvidia's own $2 billion equity investment in Synopsys announced last December, a signal that the world's most important semiconductor ecosystem players are converging around a handful of critical infrastructure providers. With activist pressure now added to the mix, watch this one closely.

Macro Picture: Under the Surface

Away from the individual company stories, Monday's macro data deserves attention.

The Chicago Fed National Activity Index slipped back into negative territory in February, falling from +0.20 in January to -0.11, a sign that broader economic momentum may be softening. U.S. construction spending also unexpectedly declined 0.3% month-over-month in January, against expectations of a small rise.

These aren't alarming numbers in isolation, but they add to a picture of an economy that is navigating significant uncertainty, elevated energy prices, a murky geopolitical backdrop, and lingering questions about Fed policy. The market's ability to rally on a single Trump tweet, while macro data quietly deteriorates, is a tension worth watching.

Conclusion

Monday's session was a good reminder of the market we're operating in: reactive, headline-sensitive, and quick to price in best-case scenarios.

Trump's five-day pause on Iran gave traders the excuse to buy, and they did, hard. But the structural problems haven't been resolved. The Strait of Hormuz is still closed, the economic data is softening, and the volatility isn't going anywhere.

Amid the noise, I find the Berkshire–Tokio Marine deal and Elliott's move into Synopsys far more interesting as longer-term portfolio signals than the TACO trade. Those are stories worth following closely over the next several months.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.