APPLIED MATERIALS INC (NASDAQ:AMAT) emerged from our Peter Lynch-inspired screen as a stock with attractive growth prospects and reasonable valuation. The company, a leader in semiconductor manufacturing equipment, meets several key criteria for long-term investors seeking sustainable growth at a fair price.

Why AMAT Fits the GARP Approach

- Strong Earnings Growth: AMAT has delivered a 5-year average EPS growth of 23.2%, well above the 15% minimum threshold in our screen. This reflects consistent execution in a high-demand industry.

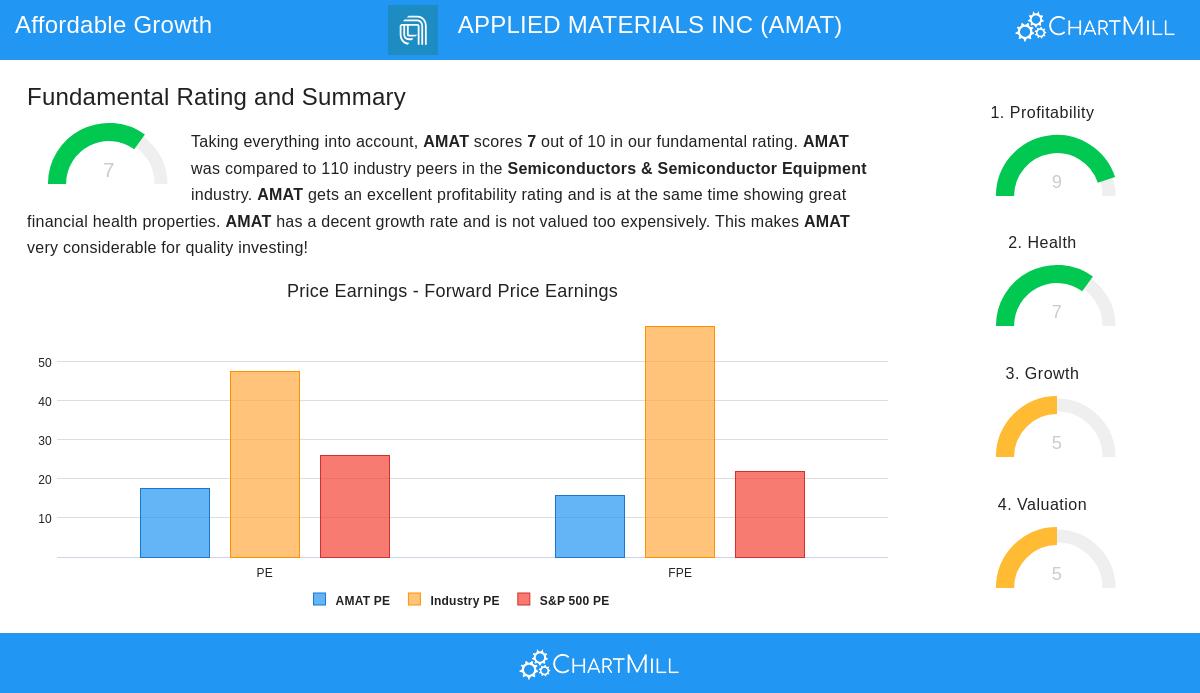

- Reasonable Valuation: While the PEG ratio of 1.81 is slightly above Lynch’s ideal threshold of 1, it remains competitive relative to industry peers. The P/E ratio of 17.4 is below both the S&P 500 average (25.9) and the semiconductor industry average (47.6).

- Healthy Financials: The company maintains a solid balance sheet with a Debt/Equity ratio of 0.34, below the screen’s 0.6 limit. Its Current Ratio of 2.68 indicates ample liquidity to cover short-term obligations.

- High Profitability: AMAT’s Return on Equity (ROE) of 34.1% far exceeds the 15% minimum, showcasing efficient use of shareholder capital.

Fundamental Strengths

Our fundamental analysis assigns AMAT a rating of 7/10, highlighting:

- Industry-leading margins: Operating margin of 29.2% outperforms 90% of semiconductor peers.

- Sustainable growth: Revenue has grown at a 13.2% annualized rate over the past 5 years, with analysts projecting continued mid-single-digit growth.

- Shareholder-friendly actions: The company has reduced shares outstanding over time and offers a growing dividend (12% annual increase over the past decade).

For investors aligned with Peter Lynch’s philosophy of buying financially sound growers at reasonable prices, AMAT warrants closer research.

Our Peter Lynch Strategy screener provides more companies matching these criteria, updated daily.

Disclaimer

This is not investing advice! The article highlights observations at the time of writing, but you should conduct your own analysis before making investment decisions.