The Peter Lynch investment strategy, famously detailed in his book One Up on Wall Street, centers on identifying companies with strong growth potential that are trading at reasonable valuations. This approach, often categorized as Growth at a Reasonable Price (GARP), emphasizes fundamental health, sustainable growth, and financial stability over market timing or speculative trends. Lynch advocated for investing in understandable businesses with solid financials, manageable debt, and proven profitability, aiming to hold these stocks for the long term. One company that recently surfaced through a screen based on Lynch’s criteria is AIFU INC - CL A (NASDAQ:AIFU), a China-based provider of insurance agency and claims adjusting services.

AIFU appears to align well with several key filters in the Lynch methodology, which prioritizes earnings growth, valuation, and financial health. Below is an analysis of how the company measures up to these criteria and why it may appeal to long-term, fundamentals-driven investors.

Earnings Growth and Sustainability Lynch favored companies with earnings per share (EPS) growth between 15% and 30% over a five-year period, enough to indicate solid expansion but not so high as to be unsustainable. AIFU’s EPS has grown at an average annual rate of 19.76% over the past five years, placing it squarely within this ideal range. This consistent growth suggests the company has been able to increase profitability without relying on excessive or erratic expansion, a hallmark of the type of business Lynch would classify as a "stalwart" or "slow grower" with reliable potential.

Valuation and the PEG Ratio Central to Lynch’s strategy is the PEG ratio, which adjusts the price-to-earnings (P/E) ratio for growth, helping to identify stocks that are undervalued relative to their growth trajectory. Lynch considered a PEG ratio below 1 as attractive. AIFU’s PEG ratio, based on past growth, is approximately 0.22, well below the threshold, indicating that the stock may be significantly undervalued given its historical earnings expansion. This low PEG aligns with Lynch’s emphasis on buying growth at a reasonable price, as it suggests investors aren’t overpaying for future potential.

Financial Health and Balance Sheet Strength Lynch placed strong emphasis on a company’s financial stability, preferring low debt and strong liquidity. AIFU’s debt-to-equity ratio of 0.05 is not only well below the screen’s upper limit of 0.6 but also exceeds Lynch’s personal preference for a ratio under 0.25. This minimal leverage reduces financial risk and indicates that the company is funded primarily through equity rather than debt. Additionally, AIFU’s current ratio of 2.50 signals strong short-term liquidity, meaning it can comfortably meet its immediate obligations, another factor Lynch considered vital for enduring market cycles.

Profitability and Return on Equity Lynch sought companies with high returns on equity (ROE), as this metric reflects efficient use of shareholder capital. AIFU’s ROE of 17.87% exceeds the 15% minimum set in the screen, indicating solid profitability and effective management. This is further supported by strong profit margins and industry-leading returns on assets, as noted in the fundamental report. For Lynch, a high ROE was often a sign of a well-run business with a durable competitive advantage.

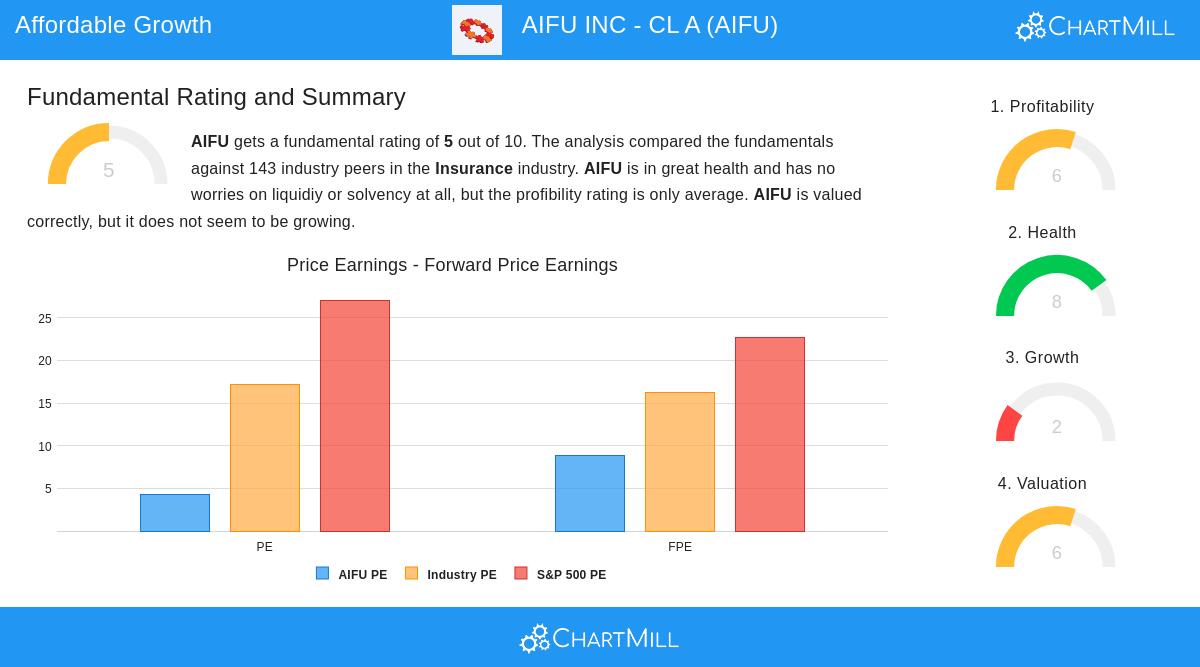

Summary of Fundamental Analysis AIFU’s overall fundamental rating of 5 out of 10 reflects a mixed but promising profile. The company performs well in financial health, with high marks for solvency and liquidity, and it demonstrates strong profitability metrics relative to industry peers. However, its growth rating is subdued due to a significant decline in revenue over the past year and a lack of forward estimates, which introduces some uncertainty. Valuation appears attractive, with low P/E and PEG ratios, but investors should note the absence of dividends and the need to monitor top-line performance. For a detailed breakdown, readers can review the full fundamental analysis report.

Contextualizing AIFU in the Lynch Framework From a Lynch perspective, AIFU operates in the insurance sector, a traditionally stable and understandable industry that aligns with his preference for "dull" businesses with predictable demand. The company’s focus on insurance agency and claims adjusting services is not flashy but may offer steady, long-term growth potential. Lynch also valued low institutional ownership and insider buying, which are not covered in this screen but could be areas for further research.

Investors interested in exploring other companies that fit the Peter Lynch strategy can find more screening results here.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own research and consult with a financial advisor before making any investment decisions.