For investors aiming to build a portfolio that generates reliable passive income, a disciplined screening process is necessary. One useful strategy involves filtering for companies that not only offer an attractive dividend today but also have the basic financial strength to maintain and possibly increase those payments over time. This method often uses composite ratings that assess multiple fundamental areas. A stock that receives a high score on a dedicated dividend rating, while also holding acceptable scores for profitability and financial condition, can be an interesting candidate. This profile indicates a company is rewarding shareholders without risking its operational stability or future investments.

EXXON MOBIL CORP (NYSE:XOM) appears from such a screening method. The integrated energy giant, a constant presence in global oil, gas, and petrochemicals, presents a case study in balancing shareholder returns with corporate strength. Its fundamental report shows a stock that fits the central ideas of defensive dividend investing, justifying additional examination for income-focused portfolios.

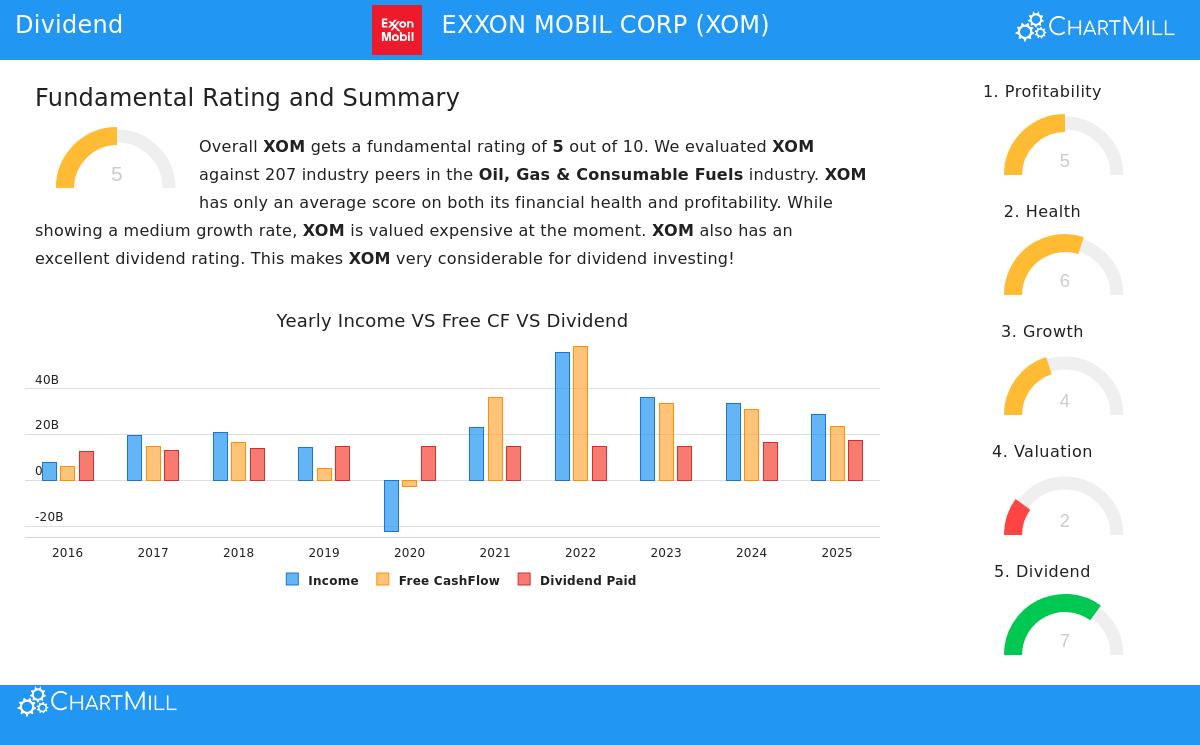

Dividend Reliability and Sustainability

The main attraction for dividend investors is, expectedly, the dividend itself. ExxonMobil’s profile here is marked by a history of reliability and measures that indicate it can be maintained.

- Yield and Track Record: The company provides a forward dividend yield near 3.48%, which is almost double the current average yield of the S&P 500. More significantly, this is not a recent or irregular payment. ExxonMobil has a reliable history, having paid and not reduced its dividend for more than ten years. This long record is a vital filter for dividend strategies, as it shows management’s dedication to returning capital to shareholders across different market periods.

- Payout Ratio Analysis: A central measure for sustainability is the payout ratio, which indicates what part of earnings is given out as dividends. ExxonMobil’s ratio is near 60%. While this is elevated, it stays within a zone usually viewed as workable, particularly for a mature, capital-heavy business. The report states that the company’s earnings are increasing more quickly than its dividend, which is a good sign that the current payout level can be kept without pressuring finances.

- Modest but Consistent Growth: The dividend itself has shown a limited yearly growth rate near 2.84% over recent years. For investors who value high current yield over fast growth, this steady, small increase can be appealing as it helps counter the effects of inflation over many years.

Supporting Fundamentals: Profitability and Financial Condition

A good dividend is only as sound as the company behind it. This is why screening for acceptable profitability and condition ratings next to the dividend rating is important, it helps steer clear of "value traps" where a high yield signals a deeper business weakening. ExxonMobil’s scores in these areas give background for its dividend soundness.

- Profitability Profile: The company gets a neutral profitability rating. It meets basic tests, having been profitable with positive cash flow in each of the last five years. Its return measures, like Return on Equity (11.12%) and Return on Invested Capital (7.38%), are strong within its industry, doing better than many peers. However, the report mentions a decrease in profit and operating margins lately. This highlights the value of the screening filter; while not the best, the profitability is seen as "acceptable," meaning the company is still producing enough earnings to finance its operations and dividend.

- Financial Condition and Solvency: With a good condition rating, ExxonMobil shows a strong balance sheet, which is critical for dividend sustainability during economic lows. The company’s Altman-Z score shows low bankruptcy risk, and its debt levels are careful. Importantly, its debt-to-free-cash-flow ratio of 1.84 is very good, meaning it could pay off all its debt with under two years of cash flow. This high solvency gives a major cushion, making sure the dividend is not endangered by too much financial leverage. The primary area of mention is liquidity, where the quick ratio is under 1, but this is typical in the capital-heavy energy sector and is offset by good overall solvency.

Valuation and Growth Considerations

From a strict dividend view, valuation is often less important than yield and safety. Still, it is a part of total return possibility. ExxonMobil’s valuation rating is low, with a P/E ratio near 21. This matches its industry peers but shows a market price that accounts for its stable, income-producing profile instead of high growth hopes. The growth rating is also neutral, with past earnings under pressure but future EPS growth forecasts becoming positive. For a dividend investor, this limited growth view paired with good condition measures may be satisfactory, as the main investment idea is focused on income generation from a settled industry leader.

A Candidate for Additional Study

ExxonMobil shows the kind of company a "Best Dividend" screen intends to find: one with a notable and reliable yield supported by sufficient profitability and a very sound balance sheet. The high dividend rating is supported by a long payment history and a workable payout ratio, while the acceptable profitability and good condition ratings imply the company has the basic strength to keep up its shareholder returns.

For investors wanting to examine other stocks that fit similar standards of high dividend quality with supporting fundamentals, you can see the full screen results here: Best Dividend Stocks Screen.

As always, this examination is based on past performance and present fundamental data. Investors should think about their own financial aims, risk comfort, and do complete study, including looking at ExxonMobil’s entire fundamental analysis report, before making any investment choices. This article is for information only and is not investment advice.