For investors looking to balance the search for growth with some caution, the "Growth at a Reasonable Price" (GARP) method provides a sensible middle path. This tactic looks for companies that are increasing their operations and earnings at a good rate but are also priced at levels that do not assume flawless future performance. It is a way to avoid the speculative excitement common around high-growth stocks and to bypass value traps, companies that are inexpensive for a cause. One instrument for applying this tactic is an "Affordable Growth" filter, which selects for stocks showing good growth, acceptable basic profit and financial soundness, and a price that is not extreme. Workday Inc. - Class A (NASDAQ:WDAY) appears as a selection from such a filter, justifying a more detailed examination of its basic profile.

Growth Path: A Main Asset

The strongest point for Workday as a GARP selection is found in its good and steady growth measures, which are the driver of any affordable growth idea. The company's basic report notes a good history and a positive forecast.

- Past Results: In the last year, Workday’s Earnings Per Share (EPS) increased by a notable 24.89%. The view over a longer period is more significant, with a yearly EPS growth rate of 30.89% over recent years. Revenue growth has also been large, rising 13.16% last year and averaging 18.42% each year.

- Future Projections: The growth narrative is not only historical. Analysts forecast continued good performance, with EPS predicted to grow at an average rate of 18.02% and revenue expected to rise by 12.60% yearly in the next few years.

This pairing of good past results and solid future projections is key for the GARP tactic. It implies the company has a lasting edge in its market, providing enterprise cloud applications for finance and human resources, that can maintain expansion even as its size grows.

Price: Sensible Given the Situation

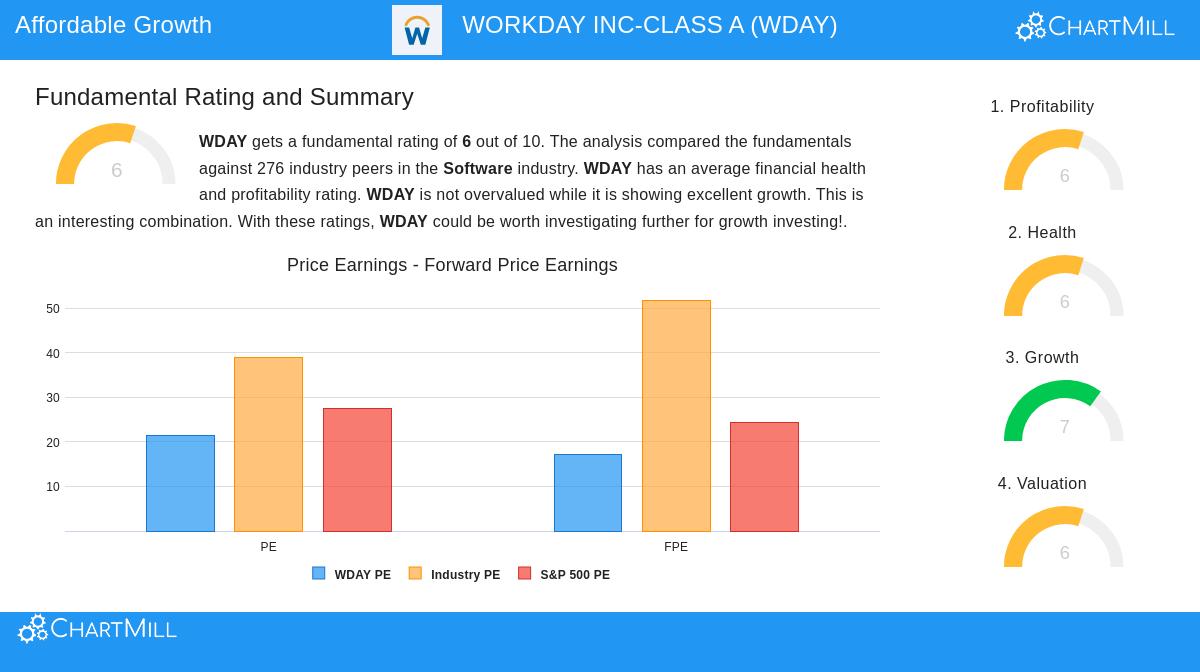

A stock cannot be viewed as "affordable growth" if its cost already accounts for many years of future achievement. Workday’s price presents a varied but finally sensible view, particularly when compared to its industry and growth outline.

- Direct and Comparative Measures: Initially, a Price/Earnings (P/E) ratio of 21.53 and a Forward P/E of 17.12 may seem high. However, the software industry is known for high growth projections and usually sells at higher prices. Compared to similar companies, Workday seems more fairly priced. Its P/E ratio is less expensive than about 72% of the software industry, and its Forward P/E is below roughly 77% of rivals.

- Growth Adjustment: Maybe the most informative measure for a GARP review is the PEG ratio, which modifies the P/E for projected earnings growth. Workday’s low PEG ratio shows the market is not paying too much for its forecasted growth, a central idea of finding affordable growth possibilities. The basic report states that its "low PEG Ratio... shows a fairly inexpensive price of the company."

This price setting is important. The tactic seeks growth that is not extremely costly, and Workday’s price, while not a bargain, seems fair and even interesting relative to both its own growth speed and its industry group.

Profit and Financial Soundness: A Steady Base

While growth and price are the main features for a GARP filter, the supporting aspects of profit and financial soundness are essential. They confirm the growth is of good quality and the company is durable. Workday receives a neutral but acceptable 6 out of 10 in both these areas, offering a steady base.

- Profit Performance: The company’s margins are a positive point. Its Operating Margin of 15.55% and Profit Margin of 13.10% are better than over 82% and 74% of industry peers, in order. Returns on capital are also good, with Return on Invested Capital (ROIC) at 9.29%, higher than 82% of software firms. These measures show that Workday’s growth is effectively turning into profits.

- Financial Soundness Points: Workday’s balance sheet displays both positives and small points of note. Its Altman-Z score shows low short-term bankruptcy danger, and its Debt-to-Free-Cash-Flow ratio is very good at 1.16, meaning it could in theory clear all debt with just over a year of cash flow. However, its Debt-to-Equity ratio is above many peers. The basic report explains this, proposing it might be from elements like share repurchases rather than high borrowing, especially with the strong FCF coverage.

For the affordable growth investor, these acceptable, if not outstanding, scores in soundness and profit are comforting. They show the company has the operational effectiveness and financial steadiness to manage economic changes and keep supporting its growth plans without high risk.

Summary and Next Steps

Workday Inc. shows a profile that matches the goals of a Growth at a Reasonable Price tactic. It displays a strong and well-set growth path in the enterprise software market, sells at a price that is acceptable relative to that growth and its industry, and is supported by good profit measures and a generally firm financial condition. The company’s basic report, which can be studied fully here, backs the idea that it is a growth narrative selling at a sensible price.

Investors curious about examining other companies that match this careful growth profile can find more possible selections by using the Affordable Growth stock filter.

Disclaimer: This article is for information only and is not financial guidance, a suggestion, or an offer to buy or sell any securities. The review is based on data and scores from ChartMill.com, and investors should do their own complete research and think about their personal financial situation and risk comfort before making any investment choices.