The investment philosophy of legendary fund manager Peter Lynch focuses on finding well-run companies with good growth prospects that are trading at sensible prices. Often called a "growth at a reasonable price" (GARP) method, Lynch’s strategy steers clear of speculative stocks, preferring businesses with steady, clear growth, sound financial condition, and appealing valuations. A stock screener using his standards can help investors locate possible candidates that deserve more study. One such company that recently appeared using this method is Workday Inc-Class A (NASDAQ:WDAY).

Examining Workday More Closely

Workday offers enterprise cloud applications for finance and human resources, serving over 11,000 organizations globally. The company’s main products in Financial Management, Human Capital Management (HCM), and Planning assist businesses in meeting industry-specific requirements. Based in Pleasanton, California, Workday has become an important participant in the competitive software industry by aiding organizations in managing their workforce and finances using AI-driven solutions.

How Workday Matches Lynch's Main Ideas

Peter Lynch highlighted steady growth, financial soundness, and reasonable valuation. Workday’s present financial measurements show a strong match with these ideas.

Steady and Solid Growth Lynch wanted companies increasing earnings consistently, but not at an unstable, very fast speed. He usually searched for 5-year earnings per share (EPS) growth between 15% and 30%.

- Workday’s 5-Year EPS Growth: 26.3%. This puts the company solidly within Lynch's preferred range, showing a good but likely maintainable historical growth path.

Sensible Valuation Compared to Growth A key part of Lynch's strategy is the Price/Earnings to Growth (PEG) ratio, which tries to find stocks that might be priced low compared to their growth rate. Lynch preferred a PEG ratio of 1 or lower.

- Workday’s PEG Ratio (Past 5 Years): 0.55. This number, much lower than 1, implies the market may be pricing Workday below its historical growth. It is an important sign for GARP investors that the stock’s price has not completely matched its earnings increase.

Good Profitability Lynch demanded a high return on equity (ROE) as a mark of efficient management and earnings generation.

- Workday’s ROE: 16.1%. This is above Lynch's common minimum of 15%, showing the company is producing satisfactory profits from shareholder equity.

Cautious Financial Condition To reduce high risk, Lynch liked companies with controlled debt amounts and enough cash to pay short-term bills.

- Debt-to-Equity Ratio: 0.38. This is well under the screener's maximum of 0.6 and fits Lynch's liking for little debt. It shows the company is financed more by equity than by debt.

- Current Ratio: 1.32. This satisfies the Lynch screen's need to be at least 1, indicating Workday has sufficient current assets to pay its short-term debts.

Fundamental Condition Review: A Summary

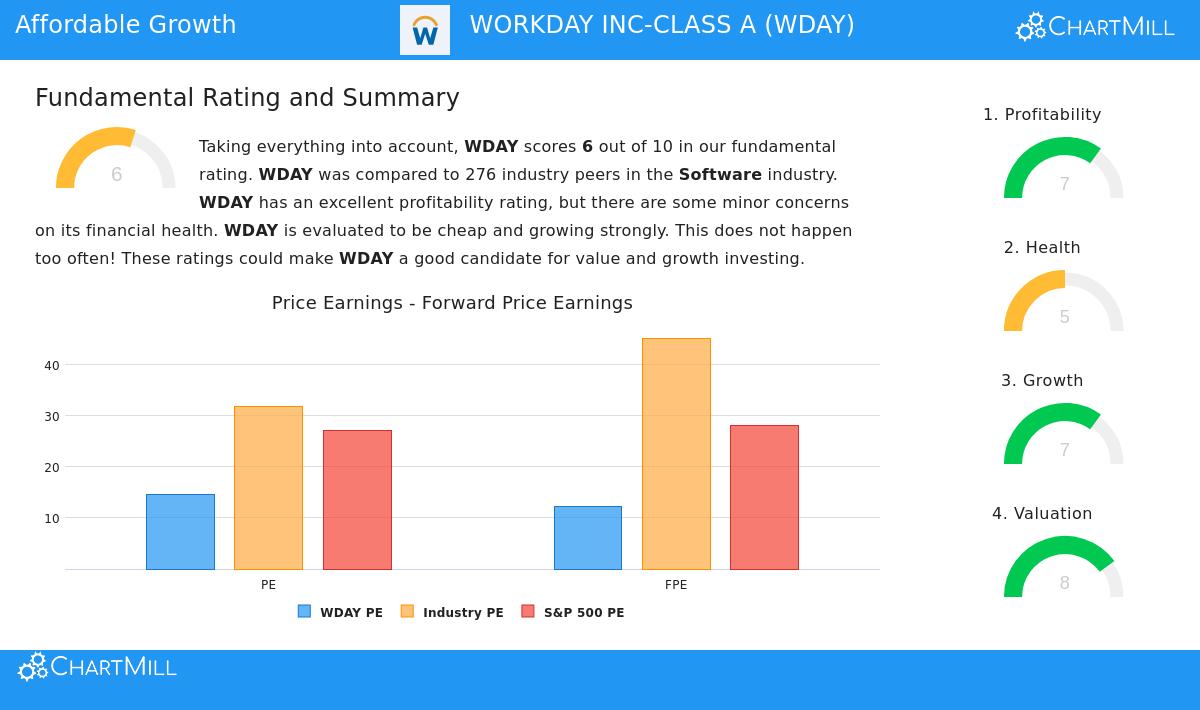

A wider fundamental analysis of Workday gives background beyond the specific Lynch filters. The company gets an overall fundamental score of 6 out of 10. Its profile is marked by clear positives in profitability and growth, together with a very appealing valuation next to both its industry and the wider market.

- Profitability & Growth: Workday rates well on profitability measures like Return on Assets (6.97%) and Return on Invested Capital (10.27%), placing it with the stronger companies in the software industry. Its revenue and EPS have displayed good double-digit growth in recent years.

- Valuation: The study points out Workday's valuation as a specific positive. Its Price/Earnings and Price/Forward Earnings ratios are lower than about 80% of its industry competitors and are notably below the present averages for the S&P 500.

- Points to Note: The report mentions some small issues about financial condition, mainly connected to liquidity ratios that are near the industry average. However, the company's low debt amounts help lessen total solvency risk.

Is Workday a Lynch-Type Investment?

Judging by the numerical filters taken from Peter Lynch’s strategy, Workday makes a strong argument for more examination by long-term, GARP-focused investors. It shows the characteristics Lynch prized: a record of solid (but not excessive) earnings growth, high profitability, a careful balance sheet, and, importantly, a valuation that seems sensible when its growth is considered through the low PEG ratio. The company works in the necessary, if ordinary, area of enterprise software, delivering vital services that businesses use every day.

For investors constructing a varied, long-term portfolio, Workday stands for the kind of fundamentally healthy growth company that Lynch might have called a possible "stalwart." As usual, a screener gives a beginning, not a final answer. The following action for any investor is the careful study Lynch promoted: learning the business model, competitive strengths, and future growth sources to judge if the company's outlook stays positive.

Find Other Possible Candidates The Peter Lynch strategy screen that found Workday can produce other noteworthy investment ideas. You can view the complete, current list of passing stocks by going to the Peter Lynch Strategy Screen.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or an offer to buy or sell any securities. The study uses data and a set screening method. Investors must do their own complete research and think about their personal financial situation and risk appetite before making any investment choices. Past results do not guarantee future outcomes.