The company that convinced the world to bet hundreds of billions on AI infrastructure has reportedly missed its own growth targets. If that doesn't make you sit up straight, I don't know what will.

The Rundown

- Doubts about OpenAI's revenue trajectory and internal leadership friction triggered a broad selloff in AI infrastructure stocks

- Oil climbed back above $110 a barrel as the Iran-US standoff deepens, with the Strait of Hormuz remaining fully blocked

- Consumer confidence surprised to the upside, while earnings delivered a genuine mixed bag, ranging from sharp miss to clean beat

- Wednesday brings the biggest macro and micro event of the week: four Big Tech heavyweights report after the bell alongside the Fed's rate decision

A Market Waiting for Wednesday

Tuesday's session was never designed to be climactic.

With MICROSOFT CORP (MSFT | ▲1.04%), ALPHABET INC-CL A (GOOGL | ▼0.16%), META PLATFORMS INC-CLASS A (META | ▼1.07%) and AMAZON.COM INC (AMZN | ▼0.54%) all lined up to report after Wednesday's close - and the Federal Reserve set to announce its rate decision earlier in the same session - many investors were simply in wait-and-see mode.

The Dow Jones barely moved, down 0.05%. The Nasdaq had less patience, shedding 0.9%.

What shifted the mood was a story out of The Wall Street Journal and it was aimed squarely at the beating heart of the current AI bull run.

OpenAI: When the Numbers Start to Matter

For a company valued at $852 billion that has never turned a profit, OpenAI has done an extraordinary job keeping the narrative intact. Until Tuesday.

The WSJ reported that OpenAI has missed its own internal revenue and user growth targets in the lead-up to its highly anticipated IPO. That would have been uncomfortable enough on its own. But the report went further: CFO Sarah Friar is said to have growing concerns about the company's staggering capital commitments, reportedly over $600 billion in future obligations to cloud providers.

Her position, according to the report, is that spending should be scaled back in line with the slowing growth trajectory. CEO and founder Sam Altman, who has built his entire strategic identity around massive AI infrastructure deployment, sits squarely on the other side of that argument. Friar is said to have found sympathisers on the board.

OpenAI raised $122 billion in its most recent funding round earlier this month, the largest private capital raise on record. That round valued the still loss-making company at $852 billion. The investor calculus behind that number rests entirely on the assumption that revenue growth will eventually catch up with infrastructure spending. Tuesday's report put a question mark next to that assumption.

Both Altman and Friar issued a joint statement denying any rift: "We're completely aligned on buying as much compute as possible and we work on this every day." A statement like that - precise, coordinated, and entirely focused on the one thing they're not disagreeing on - is worth reading carefully.

The market read it and sold.

Companies with deep OpenAI ties took the biggest hits.

ORACLE CORP (ORCL | ▼4.05%) dropped 4%. COREWEAVE INC-CL A (CRWV | ▼5.83%) shed nearly 6%. ADVANCED MICRO DEVICES (AMD | ▼3.41%) fell more than 3%. NVIDIA CORP (NVDA | ▼1.59%) lost 1.6%.

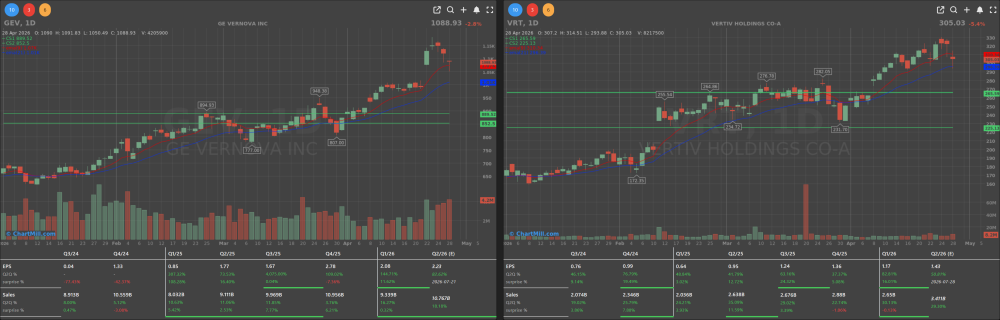

SoftBank, OpenAI's largest financial backer, had already absorbed a 10% hit in Tokyo earlier that day, the US-listed shares closed 12% lower. Power infrastructure plays tied to the datacenter buildout weren't spared either:

GE VERNOVA INC (GEV | ▼2.79%) and VERTIV HOLDINGS CO-A (VRT | ▼5.40%) both took meaningful hits.

One name bucked the trend: MICROSOFT CORP (MSFT | ▲1.04%), which holds a 27.5% stake in OpenAI and has its own multi-layered cloud and enterprise AI revenue base to insulate it. That 1% gain, in this context, is actually noteworthy.

The OpenAI story isn't entirely new. Anthropic has been taking share in coding and enterprise markets. Google's Gemini and Anthropic's Claude have closed the product gap considerably since ChatGPT first ran away with the narrative. But there's a meaningful difference between "competitors are catching up" and "the market leader is missing its own internal targets."

Oil Pushes Back Above $110

The Iran-US standoff isn't softening. Brent crude rose roughly 2.5% on Tuesday to trade above $111 a barrel, fully erasing all the losses that accumulated during ceasefire speculation earlier in the month. WTI traded around $100. Every decline since the blockade began has been bought back.

President Trump reportedly rejected Iran's proposed interim arrangement, which would have lifted the Strait of Hormuz blockade first and addressed the nuclear programme in subsequent negotiations.

Trump is said to be dissatisfied with those sequencing terms.

Sustained oil above $100 doesn't just show up at the petrol station, it feeds into inflation expectations, complicates the Fed's rate decisions, and suppresses consumer discretionary spending. All of which matters directly for the earnings and guidance that companies will be delivering over the next 48 hours.

Consumer Confidence: A Rare Bright Spot

Not all the macro signals were negative. The Conference Board's Consumer Confidence Index rose to 92.8 in April, economists had pencilled in a decline to 89. March's reading was also revised higher.

The high fuel prices appear, for now, to be putting less strain on American consumers than many feared. Whether that holds as the summer driving season approaches is a separate question, but it's a more encouraging number than the consensus expected.

Earnings: Everything But Boring

Tuesday's earnings flow was genuinely varied. The range between the best and worst single-stock performance told the story.

SPOTIFY TECHNOLOGY SA (SPOT | ▼12.43%) had the hardest landing. Q1 revenue came in at €4.5 billion, up 8% year-on-year but fractionally below the €4.53 billion analyst consensus.

The operating result rose 40% to €715 million, and EPS hit €3.45, those are fine numbers in isolation. The problem was the Q2 guidance: operating profit of €630 million, well below the €674 million consensus, and a gross margin forecast of 33.1%, barely above Q1's 33%. Bloomberg Intelligence was direct about the elephant in the room: growing concern that AI-generated music is beginning to take market share. Citi maintained its buy rating and $650 price target but acknowledged the market reaction was unsurprising.

The recently installed dual-CEO structure - shared between Gustav Söderström and Alex Norström - adds its own layer of uncertainty to an already clouded picture.

COCA-COLA CO/THE (KO | ▲3.86%) delivered the cleanest result of the day. EPS of $0.86 beat the $0.81 consensus; revenue of $12.5 billion topped the $12.25 billion estimate. Full-year guidance for 4-5% organic revenue growth was maintained intact. In an environment where consumer pressure is building, a staples name executing this reliably is worth noting.

VISA INC-CLASS A SHARES (V | ▼0.11%) closed barely changed on Tuesday, but the after-hours reaction told the real story. Q2 EPS of $3.31 beat the $3.10 estimate cleanly and revenue grew 17% year-on-year, the strongest growth rate since 2022.

The stock jumped roughly 5% in extended trading. CEO Ryan McInerney cited "resilient consumer spending" across all business lines. American Express had already corroborated that picture, reporting 10% spending growth with its own cardholders. Payments companies are, for now, one of the more reliable corners of the consumer economy.

STARBUCKS CORP (SBUX | ▼0.62%) posted its second consecutive quarter of positive comparable sales growth under CEO Brian Niccol, a milestone worth pausing on, given where the company was a year ago.

US comp sales rose 7.1%, overall comparable sales were up 6.2%, and revenue grew 9% to $9.5 billion. Adjusted EPS of $0.50 cleared the $0.43 estimate by a meaningful margin. The turnaround strategy - better service, renewed stores, new products, and high-profile marketing partnerships with Taylor Swift and MrBeast - is quietly producing results. The stock added 5% in after-hours trading. That's particularly notable against a backdrop where Domino's reported falling March sales as consumer confidence dipped and competitors discounted more aggressively.

UNITED PARCEL SERVICE-CL B (UPS | ▼3.97%) beat on adjusted EPS at $1.07, but revenue declined and the full-year outlook was left unchanged rather than raised. In this market, a modest earnings beat without a guidance upgrade doesn't get rewarded. The stock lost 4%.

SHERWIN-WILLIAMS CO/THE (SHW | ▼3.52%) grew both revenue and profit in Q1 and maintained its full-year outlook, the market sold it off anyway. Sometimes meeting expectations simply isn't enough.

Wednesday's Main Event

Wednesday afternoon, MICROSOFT CORP (MSFT | ▲1.04%), ALPHABET INC-CL A (GOOGL | ▼0.16%), META PLATFORMS INC-CLASS A (META | ▼1.07%) and AMAZON.COM INC (AMZN | ▼0.54%) all report within hours of each other.

These four names represent an enormous share of both the S&P 500 and the Nasdaq. Their results - and specifically their commentary on AI capital spending, cloud demand, and advertising - will directly test the OpenAI narrative that rattled markets on Tuesday. If they confirm robust AI investment returns, the selloff looks like an overreaction. If they hedge their language around ROI and timeline, Tuesday may look like a preview.

Earlier in the same session, the Federal Reserve announces its rate decision. With oil above $100, inflation expectations rising in the background, and consumer confidence surprisingly resilient, the path forward for rates isn't a straightforward call.

The euro-dollar pair is trading around 1.1710. UniCredit has flagged the potential for EUR/USD to reach 1.20 if the ECB eventually moves to raise rates while the Fed continues cutting, a spread worth monitoring.

Bottom line

Tuesday was the market asking a question it had been politely avoiding: does the AI investment thesis hold up when the numbers behind it start to crack?

OpenAI's stumble handed the bears a concrete data point. Wednesday's Big Tech earnings won't settle the debate permanently, but they will move it decisively in one direction or the other. I'll be watching the guidance language at least as closely as the headline numbers.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.