For investors looking for a mix of solid increase and fair cost, the "Growth at a Reasonable Price" (GARP) method presents a strong middle path. This method tries to find companies that are increasing their earnings and sales faster than normal but are also priced in a way that does not completely account for that future possibility. It avoids both risky, very costly growth prospects and unchanging, low-priced value stocks. One way to search for these chances is by using fundamental ratings that evaluate important parts of a business. A stock that gets high marks for increase, earnings strength, and financial soundness, while also keeping a fair price score, can be a good fit for this method. Insulet Corp (NASDAQ:PODD) recently appeared on such an "Affordable Growth" search, justifying a more detailed examination of its fundamental picture.

A Base of Solid and Lasting Increase

The central idea of any GARP investment is, expectedly, increase. A company must show a clear ability to get bigger, with a believable path for that to keep going. Insulet's fundamental report shows notable strength here, receiving a top-level Increase rating of 9 out of 10. The company's past results are notable, but more key, the path seems lasting.

- Past Speed: Over the last year, Insulet increased its Revenue by 27.1% and its Earnings Per Share (EPS) by 27.6%. The view over five years is even stronger, with a 5-year yearly Revenue increase rate of 22.9% and EPS increase of 79.2%.

- Future Predictions: Analyst projections indicate this speed is not finished. Revenue is forecast to increase at a typical yearly rate of 20.6% in the next few years, while EPS is predicted to rise by 28.1%. This forward-looking increase is a key part, as the GARP method depends on future earnings to support the current stock price.

This steady, double-digit increase in both sales and profits points to a company gaining market position and enlarging its activities effectively, a requirement for being seen as an "affordable" increase story.

Price: The Cost for Good Increase

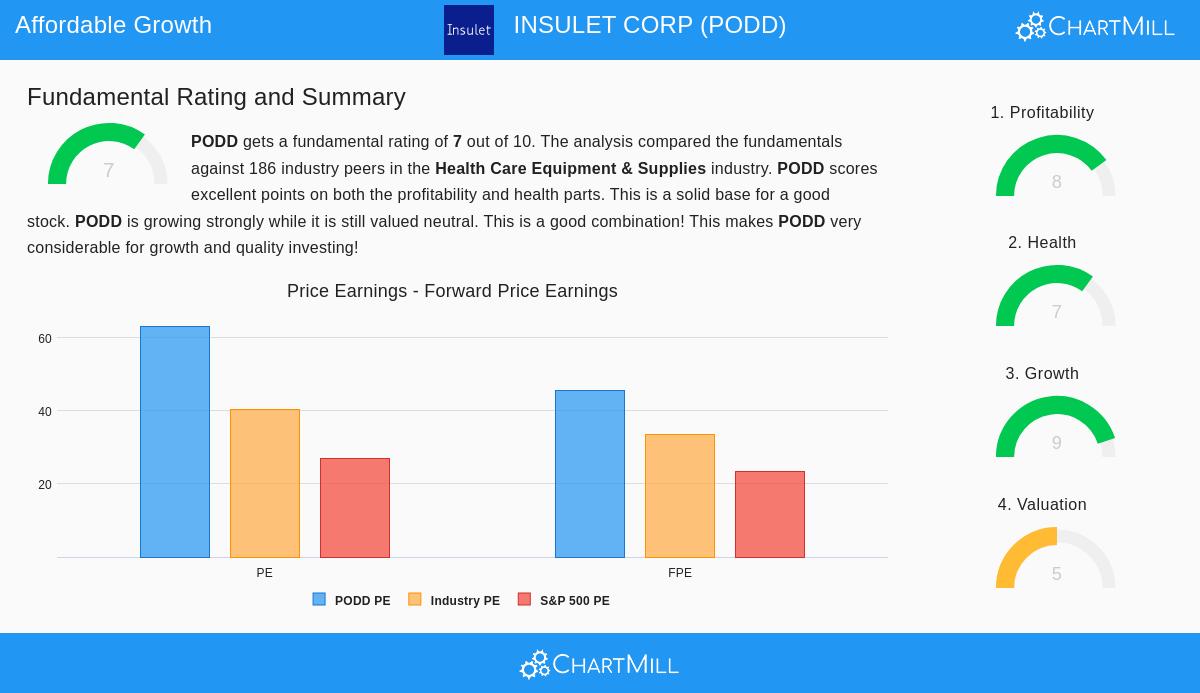

The "reasonable price" part of GARP is often the most discussed. Insulet's Price rating of 5 shows this balance. At first look, common measures suggest a higher cost. The company's Price/Earnings (P/E) ratio of 63.2 and its Forward P/E of 45.5 are much higher than wider S&P 500 averages. This at first seems to go against the "affordable" name.

However, price cannot be seen alone. Two key setting points help the case for fairness:

- Sector Comparison: Compared to similar companies in the active Health Care Equipment & Supplies field, Insulet's price looks more average. Its P/E ratio is lower than about 67% of field companies, and its Forward P/E is lower than almost 70%. This relative price is key, as it shows the market is setting a cost for increase for the whole sector, and Insulet is not an exception.

- Increase Adjustment: The fundamental analysis mentions that the PEG ratio, which changes the P/E for predicted earnings increase, points to a "fair price." Also, the report clearly says that Insulet's "excellent earnings strength rating" and solid predicted earnings increase "could support a higher PE ratio." In short, you are paying for high-quality, clear increase, the core of the GARP idea.

Supporting Basics: Earnings Strength and Financial Soundness

An increase story built on weak finances or poor earnings strength is a uncertain one. The GARP method lowers this risk by needing fair scores in Soundness and Earnings Strength, making sure the company has the financial strength to carry out its increase plans. Insulet does well here, with an Earnings Strength rating of 8 and a Soundness rating of 7.

Earnings Strength Points:

- The company has very good margins, with a Gross Margin of 71.5%, an Operating Margin of 17.3%, and a Profit Margin of 9.8%, each placed in the top level of its field.

- Returns on capital are solid, with a Return on Invested Capital (ROIC) of 14.5% and a Return on Equity (ROE) of 17.8%, both doing much better than field peers.

Financial Soundness Review:

- Insulet shows a very low chance of financial trouble, shown by a strong Altman-Z score of 9.28.

- Cash availability is good, with a Current Ratio of 2.87 and a Quick Ratio of 2.18, showing enough ability to meet near-term needs.

- While the Debt/Equity ratio is seen as average for the field, the report ends that the company has "very little existing debt," reducing payment worries.

These solid supporting basics give trust that Insulet's increase is not only fast but also high-quality and built on a steady financial foundation. This lowers the investment risk and helps the case that the increase cost in its stock price is connected to a lasting business model.

Summary

Insulet Corp shows a standard case for Growth at a Reasonable Price study. The company is clearly in a fast-increase stage, with excellent past measures and a positive forecast. While its total P/E numbers are high, they are supported within its increase field and when weighed against its very good earnings strength and firm financial soundness. For an investor using a GARP method, PODD stands as a possible chance to invest in a company with a strong increase driver, without entering the area of speculative price extremes. The fundamental ratings, high Increase and Earnings Strength, good Soundness, and a middle Price, match well with the search rules made to find such chances.

You can see the full fundamental analysis for Insulet Corp (NASDAQ:PODD) here.

Searching for more options that match this picture? Our set Affordable Growth Search is refreshed often and can help you find other stocks showing strong increase, fair basics, and acceptable prices.

,

Disclaimer: This article is for information only and is not financial advice, a suggestion to buy or sell any security, or a support of any investment method. The information given is based on data supplied and fundamental analysis reports, which may change. Investors should do their own complete study and think about their personal financial situation and risk comfort before making any investment choices.