For investors looking for a mix of solid expansion and fair prices, the "Growth at a Reasonable Price" or "Affordable Growth" method presents a sensible option. This method looks for companies with good, steady growth paths while steering clear of those with prices that assume too much future success. The aim is to identify businesses where growth is still present, but the current cost allows for some protection and a believable chance for good returns. One stock that recently appeared from this type of filter is Insulet Corp (NASDAQ:PODD), a top company in tubeless insulin pump technology.

A Good Growth Path

The central idea of any affordable growth method is, of course, growth. Insulet’s basic facts are strong here, receiving a high ChartMill Growth Rating of 9 out of 10. The company is not just talking about future growth, it is achieving it regularly.

- Revenue Growth: In the last year, revenue increased by 27.12%. More notably, the average yearly revenue growth in recent years is 22.92%.

- Earnings Increase: The profit growth is more pronounced. Earnings Per Share grew by 27.65% last year and has risen at an average yearly rate of 79.24% in recent years.

- Future Expectations: This pace is likely to persist. Analyst forecasts point to good future revenue growth of about 20.64% per year and EPS growth averaging 28.51% each year.

This steady performance in both revenue and profits forms a good base for the growth part of the investment case, showing a company that is effectively growing in the big and increasing diabetes care market.

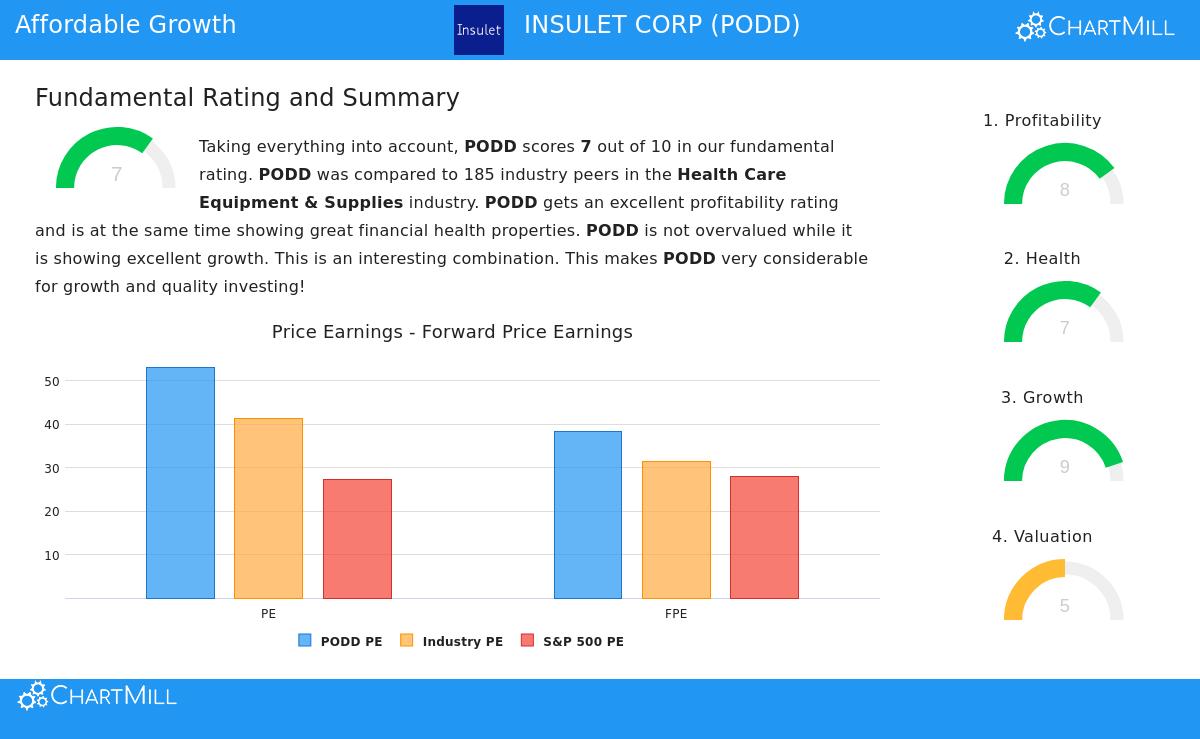

Price Considerations

While growth is necessary, paying a fair price for that growth is what makes it "affordable." Insulet’s price presents a detailed picture, earning a ChartMill Valuation Rating of 5. On a simple level, numbers like a Price-to-Earnings ratio of 53.12 and a Forward P/E of 38.29 seem high, particularly next to the wider S&P 500. However, price is relative, especially for fast-growing companies in specific fields.

- Industry Comparison: Next to similar companies in the Health Care Equipment & Supplies industry, Insulet’s price seems more acceptable. Its P/E ratio is lower than about 68% of the industry, and its Forward P/E is lower than almost 70% of others.

- Growth Adjustment: The Price/Earnings-to-Growth ratio, which modifies the P/E for expected growth, indicates the current price could be suitable given the company's high growth rate. The analysis states that the high simple valuation "may be acceptable as PODD's earnings are expected to grow with 34.21% in the coming years."

For a GARP investor, this detail is important. The filter specifically finds stocks that are "not overpriced," and Insulet’s valuation rating of 5, along with its industry-relative cost and strong growth story, indicates it fits this idea of fair pricing within its fast-growing group.

Basic Financial Soundness

An affordable growth method must also think about the longevity of the growth. A company requires a sound financial base (Health) and effective operations (Profitability) to maintain its expansion, which is why filters check for adequate scores in these areas. Insulet scores well here, with a Health Rating of 7 and a Profitability Rating of 8.

The company’s financial condition is helped by a very good Altman-Z score of 8.10, showing low short-term default risk, and a sound current ratio of 2.87. While it has some debt, its capacity to produce free cash flow is good, with a Debt-to-FCF ratio of 2.49, meaning it could pay off all debt in less than two-and-a-half years using its current cash flow.

On profitability, Insulet does very well. It has high returns, including a Return on Equity of 17.79% (better than 93.5% of its industry) and a Return on Invested Capital of 14.49%. Its margins are also high, with a Gross Margin above 71% and a Profit Margin of 9.76%, putting it in the top part of its industry. This high profitability helps support its price level and supplies the money required to fund future growth.

Summary

Insulet Corp represents a possibility that fits the ideas of affordable growth investing. It shows clear, double-digit growth in both revenue and profits that is expected to keep going. While its simple price numbers are high, they are understood in light of its better growth rate and seem fair compared to its industry. Importantly, this growth is supported by high profitability numbers and a sound financial condition, suggesting the growth is lasting and of good quality.

This review uses Insulet’s full Fundamental Analysis Report, which gives a detailed look across growth, valuation, profitability, health, and dividend areas.

Investors curious about finding other companies that match this profile of acceptable growth, decent basics, and fair price can review more outcomes using the Affordable Growth stock screen.

Disclaimer: This article is for information only and does not make up financial advice, a suggestion to buy or sell any security, or a support of any investment plan. Investors should do their own study and think about their personal financial situation and risk comfort before making any investment choices.