PAYCOM SOFTWARE INC (NYSE:PAYC) stands out as a potential candidate for quality investors, based on our Caviar Cruise screening methodology. The company demonstrates strong profitability, consistent growth, and efficient capital allocation, making it a compelling option for long-term investors.

Key Strengths of PAYCOM SOFTWARE INC

- High Return on Invested Capital (ROIC): PAYC’s ROIC (excluding cash and goodwill) is an impressive 27.09%, well above the 15% threshold for quality stocks. This indicates the company generates substantial returns from its investments.

- Strong Profit Growth: Over the past five years, PAYC has delivered an EBIT growth CAGR of 22.90%, significantly outpacing its revenue growth of 7.06%. This suggests improving operational efficiency and pricing power.

- Healthy Profit Quality: The company’s five-year average profit quality (free cash flow to net income) is 84.82%, reflecting reliable cash generation from earnings.

- Zero Debt Burden: PAYC has no outstanding debt, meaning it operates with a clean balance sheet and no financial leverage risk.

- Consistent Revenue Expansion: Analysts expect future revenue growth to remain steady at 7.06% annually, reinforcing the company’s ability to sustain expansion.

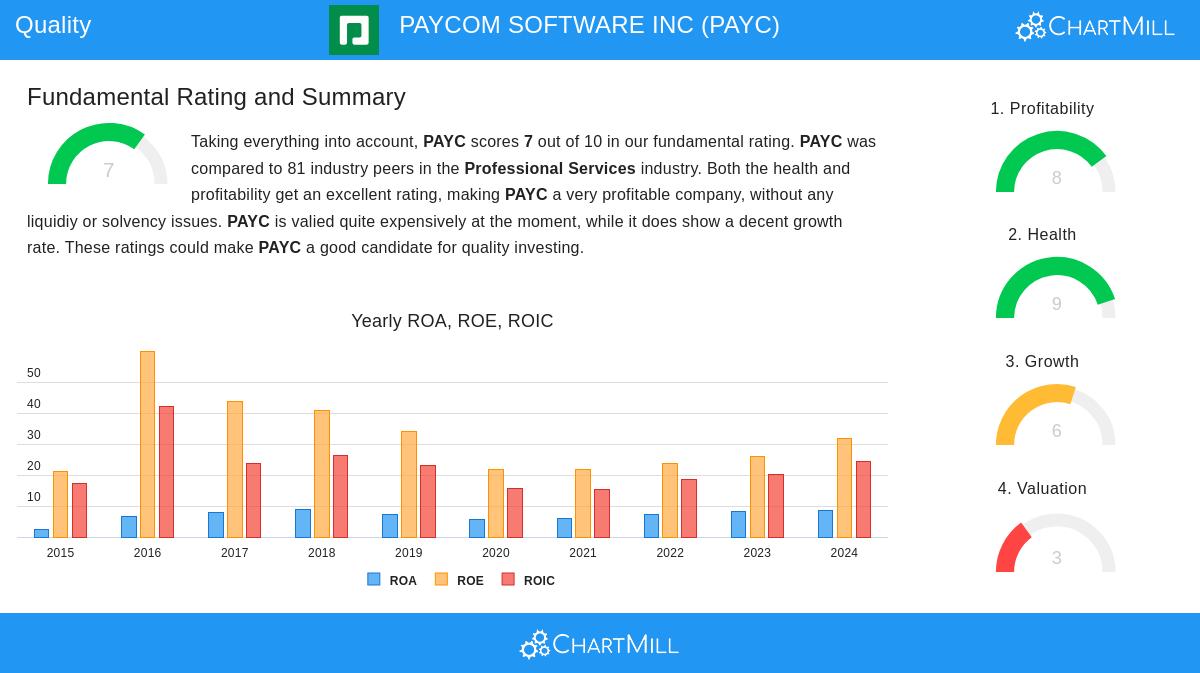

Fundamental Analysis Summary

PAYC earns a solid fundamental rating of 7 out of 10, with particularly high marks in profitability and financial health. Key takeaways include:

- Profitability: The company outperforms most peers in operating margin (27.88%) and profit margin (20.60%).

- Valuation: While PAYC trades at a premium (P/E of 29.13), its strong growth and profitability may justify the higher multiple.

- Growth Outlook: Earnings are projected to grow at 12.40% annually, though revenue growth is expected to moderate slightly.

For investors seeking high-quality businesses with strong fundamentals, PAYC presents a well-rounded profile.

Our Caviar Cruise screener provides more quality stock ideas and is updated regularly.

Disclaimer

This is not investment advice. Always conduct your own research before making investment decisions.