For investors looking for a dependable source of passive income, a systematic filtering method is important to steer clear of high-yield dangers. One useful technique is to concentrate on stocks that provide a good dividend and are also founded on solid core business operations. This method values endurance above high yield, selecting for companies with a high ChartMill Dividend Rating to confirm quality, while also asking for satisfactory scores in Profitability and Financial Health. This pairing finds businesses able to keep and possibly increase their dividends over time, instead of those where a high yield may point to hidden trouble.

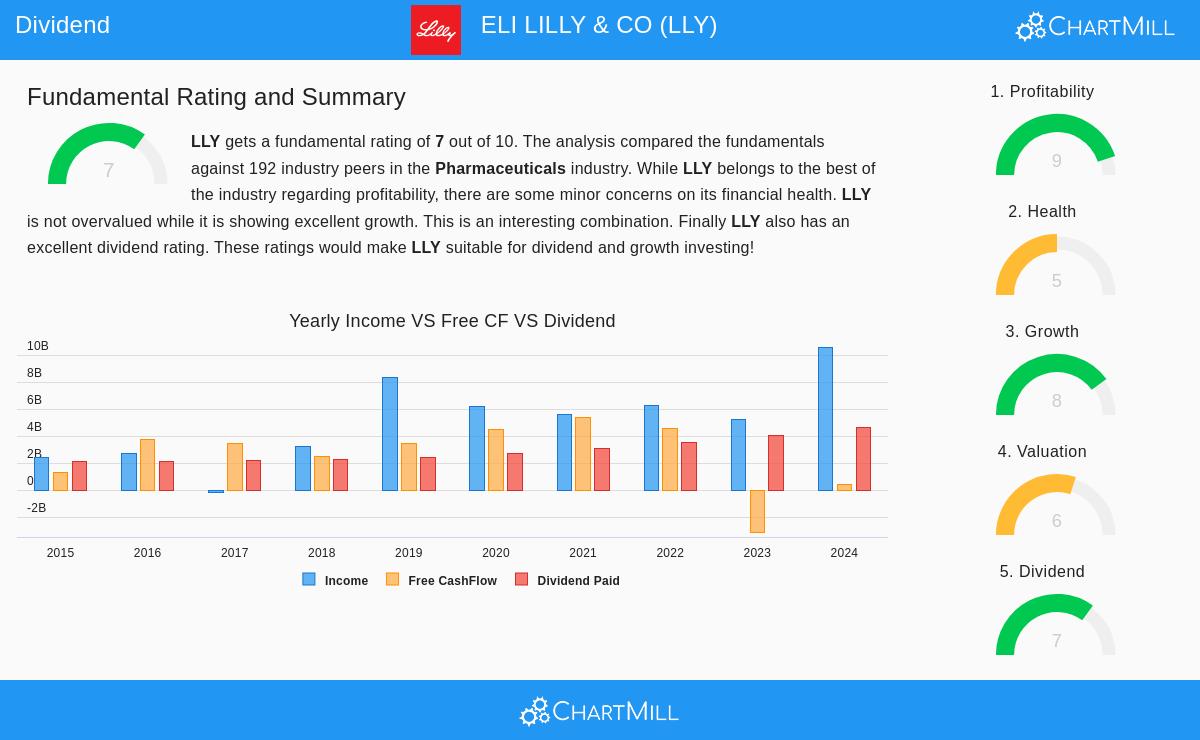

A clear instance resulting from this filter is ELI LILLY & CO (NYSE:LLY). The pharmaceutical leader receives a solid Dividend Rating of 7, aided by a first-class Profitability Rating of 9. Its Financial Health Rating of 5, while showing some points to note, reaches the "satisfactory" level needed by the method, implying the firm is not in immediate financial trouble. This description makes Lilly an interesting option for dividend investors that prize steadiness and expansion possibility with their income.

A Dividend Founded on Steadiness and Expansion

The heart of Lilly's attraction for dividend investors rests in the standard and direction of its shareholder returns, not a striking initial yield. The company’s dividend narrative is one of steady expansion backed by a maintainable financial framework.

- History of Raises: Lilly has a steady record, having paid and raised its dividend for at least ten straight years. This shows a management dedication to giving capital back to shareholders across different market periods.

- Notable Dividend Expansion: The typical yearly dividend expansion rate of 15.59% over recent years is notable. This expansion greatly exceeds inflation and improves the long-run income possibility for investors who reinvest dividends or depend on an increasing cash stream.

- Maintainable Payout Ratio: A central measure for endurance, Lilly’s payout ratio is at a manageable 28.28% of its earnings. This low ratio means the company keeps most of its profits to put back into its successful drug pipeline, future expansion projects, and more debt decrease, all while allowing a big safety cushion for the dividend.

While its present dividend yield of 0.54% is small next to the wider market average, this is a direct result of the company's large stock price gain pushed by its expansion outlook. The method of filtering for a high Dividend Rating centers on the standard and endurance of the dividend, not only the yield, which can frequently be made larger by a declining stock price.

Profitability: The Source Financing Future Payments

Lilly’s outstanding Profitability Rating of 9 is the basic source that allows its steady dividend. This rating is vital for the filtering method, as a very profitable company creates the extra cash required to pay dividends without stressing its finances.

- Excellent Returns: The company creates superior returns on its capital, with a Return on Invested Capital (ROIC) of 28.84%, much higher than its cost of capital. This shows very efficient use of shareholder money.

- Sector-Best Margins: Lilly works with leading margins, including an Operating Margin of 44.41% and a Gross Margin above 83%. These solid margins give a lasting guard against cost increases and assure strong cash flow creation to back all corporate goals, including dividends.

This degree of profitability supplies the financial strength to keep financing research and development, the essential element of a pharmaceutical company, while also regularly compensating shareholders. A sound profitability picture is essential for a maintainable dividend method, as it indicates a business framework that can survive economic declines.

Financial Health: A Measured Evaluation

The filtering method asks for a "satisfactory" degree of financial health, and Lilly’s rating of 5 shows a varied situation that deserves investor notice. The company’s health is aided by its superb profitability but affected by its capital structure.

- Solvency Soundness: Lilly’s Altman-Z score of 8.09 is very good and shows a very small short-term chance of financial difficulty, easily beating most industry rivals.

- Debt Points: The main issue is in its borrowing, with a Debt-to-Equity ratio of 1.72 that is above many industry peers. This is a usual trait for big pharma companies that often use debt for strategic purchases and share repurchases. While the debt amount is high, it is presently well-aided by the company’s huge and increasing cash flows.

The filter for satisfactory health helps bypass companies with serious balance sheet problems. In Lilly’s situation, the rating implies investors should watch debt amounts, but the dominant soundness of its cash-creating ability gives meaningful confidence about its capability to handle debts and keep its dividend.

Valuation and Expansion Setting

It is key to see the dividend idea inside Lilly’s complete investment story. The company is in a time of fast expansion, pushed by its GLP-1 drugs for diabetes and obesity. This supports both its high valuation and its ability for dividend expansion.

- Expansion Explains High Value: Analysts project earnings to expand by over 42% in the next years. This fast expansion profile helps explain its present valuation measures and indicates future dividend raises could be large.

- Combined Idea: For a dividend expansion investor, Lilly presents a mixed chance. It gives the steady, increasing income stream they want, but it is driven by a changing growth story more common of a fast-expansion stock. This mix is uncommon and is exactly what a multi-part filtering method tries to find.

A complete look at all these basic points is present in the full ChartMill Fundamental Analysis Report for LLY.

Conclusion

ELI LILLY & CO shows the result of a systematic dividend filtering method that looks past yield. It fits the main conditions of a high-standard dividend aided by superb profitability and acceptable financial health. The company presents an interesting bundle for the dividend expansion investor: a long-standing, increasing payment financed by a very profitable business that is itself in a strong growth phase. While the present yield is small, the chance for meaningful future dividend expansion, supported by fast earnings growth, makes it a distinct option for those making a long-run, income-focused portfolio.

For investors wanting to find other companies that fit similar conditions of sound dividends, profitability, and financial health, you can review the complete list of outcomes by using the Best Dividend Stocks screen.

Disclaimer: This article is for information only and does not form financial guidance, a suggestion, or a deal to buy or sell any security. Investing holds risk, including the possible loss of capital. You should do your own study and talk with a certified financial consultant before making any investment choices.