For investors looking for a structured, long-term way to build wealth, few methods are as respected as Peter Lynch’s. As the famous leader of the Fidelity Magellan Fund, Lynch supported a idea of putting money into what you understand, concentrating on firms with clear operations, good expansion, and fair prices. His method, often called Growth at a Reasonable Price (GARP), stays away from risky trends by requiring durable expansion, sound finances, and a buffer in the share price. A filter using his main ideas, like steady profit expansion, little debt, good earnings, and a fair price compared to that expansion, can find firms that deserve more study for a long-term holding.

One firm that recently met a Peter Lynch-style filter is INTUIT INC (NASDAQ:INTU), the maker of financial software and products such as TurboTax, QuickBooks, and Credit Karma. Initially, Intuit matches the Lynch example of a "simple" but necessary operation: it gives key services for tax filing, small business bookkeeping, and personal finance. These are products with repeat need, forming a steady and clear source of income. The following stage is to see how it matches Lynch's number-based checks.

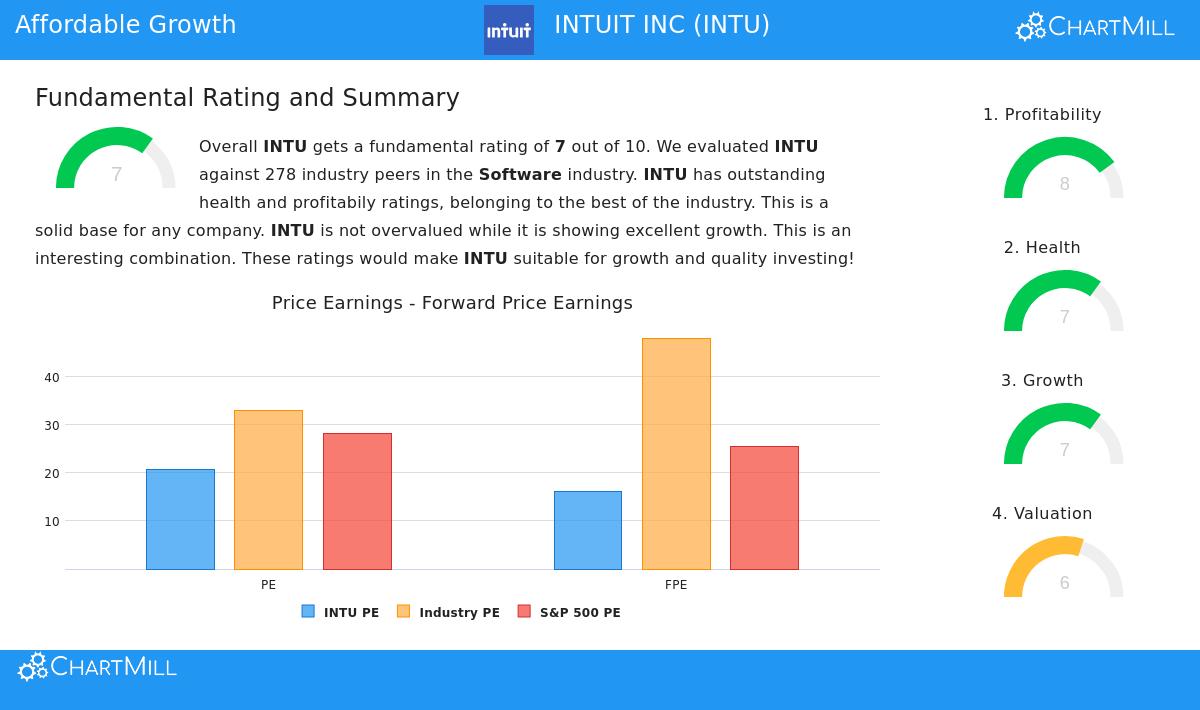

Matching the Lynch Standards

The filter uses particular rules to find firms with durable expansion and solid finances. Intuit's present numbers match these ideas closely:

- Durable Profit Expansion: Lynch looked for firms expanding consistently, not suddenly. He liked a 5-year earnings per share (EPS) expansion rate between 15% and 30%. Intuit's EPS has expanded at an average yearly rate of 20.77% over the last five years, putting it directly in this durable expansion range.

- Fair Price (PEG Ratio): A key part of the GARP method is the Price/Earnings to Growth (PEG) ratio, which Lynch liked at 1.0 or less. This number changes the standard P/E ratio for expansion, helping to find shares that might be priced low given their expansion path. Intuit's PEG ratio, using its past five-year expansion, is 0.99, showing the market is pricing its profit expansion nearly exactly at Lynch's mark for a fair price.

- Sound Financial Condition: Lynch stressed a solid balance sheet. The filter asks for a Debt-to-Equity ratio below 0.6, with Lynch himself favoring a more careful level below 0.25. Intuit's ratio of 0.28 shows a funding structure using mostly equity, not debt, lowering money risk. Also, its Current Ratio of 1.39 shows it has enough near-term assets to meet its close debts, passing another of Lynch's cash checks.

- High Earnings (ROE): A high Return on Equity (ROE) shows good use of owner money. The filter looks for firms with an ROE above 15%. Intuit's ROE of 21.31% is well above this level, showing leadership is creating good profit from the money put into the operation.

A Top-Level Basic View

A wider basic study of Intuit supports the image shown by the Lynch filter. The firm gets a good total basic score of 7 out of 10, with special force in two areas Lynch would like: earnings and financial condition.

- Earnings Leader: Intuit's margins are strong. It has a Gross Margin near 80% and an Operating Margin over 26%, doing better than most of its software industry group. Its returns on assets, equity, and invested money are all high, regularly placed in the top part of its field.

- Firm Balance Sheet: The condition score agrees with the low debt load noted before. The firm's Altman-Z score points to a very small chance of money trouble, and its debt level compared to its free cash flow shows it could clear all its debts in under a year.

- Expansion Path: While future expansion is thought to slow a bit from its strong past results, experts still plan good forward EPS expansion of about 15.5%. This fits Lynch's liking for durable, not extreme, expansion.

- Price Setting: On a lone P/E basis, Intuit may seem fairly priced. But, when compared to the wider software industry and the S&P 500, and, most key, when changed for its expansion via the PEG ratio, its price seems more fair. You can see the complete, full basic report for INTU here.

Closing

For an investor following the Peter Lynch idea, Intuit offers a strong example. It works in necessary, clear fields like taxes and small business finance. Importantly, it meets the number-based checks Lynch suggested: it has shown durable historical profit expansion, keeps a clean balance sheet with very little debt, makes high returns on equity, and is priced at a level that fairly shows its expansion picture. It represents the "growth at a reasonable price" goal, where the investor is not paying too much for future possibility.

While no filter replaces deep, personal study into a firm's competitive edge, leadership, and future outlook, a Lynch-based check works as a very good beginning point. Intuit, based on the given numbers, justifies more attention for long-term investors looking for good expansion firms selling at sensible prices.

Want to see other firms that meet a similar Peter Lynch investment filter? You can find more possible choices and adjust the filter to your own settings by going to the Peter Lynch Strategy screener.

Disclaimer: This article is for information and learning only. It is not a suggestion to buy, sell, or keep any security. The study is based on given data and a particular investment plan filter. All investing has risk, including the chance to lose the original amount. You should do your own full study and think about talking with a registered money advisor before making any investment choices.