For investors looking for a disciplined, long-term way to build wealth, few strategies are as respected as Peter Lynch's method. As explained in his book One Up on Wall Street, Lynch's thinking focuses on finding well-run, expanding companies trading at sensible prices—a style often called Growth at a Reasonable Price (GARP). He supported investing in businesses that are easy to understand, have good fundamentals, lasting expansion, and sound financial condition, then keeping them for many years. A filter based on his main criteria—covering profit expansion, price, earnings power, and balance sheet quality—can identify possible choices for this kind of portfolio. One company that recently came from this filter is INTUIT INC (NASDAQ:INTU), the maker of financial software such as TurboTax and QuickBooks.

A Base of Lasting Expansion

A key part of Lynch's strategy is finding companies with a steady and lasting expansion path. He specifically advised against pursuing extremely fast expansion, which is often not maintainable, favoring instead reliable, foreseeable growth. The filter looks for companies with a 5-year earnings per share (EPS) expansion rate between 15% and 30%.

- INTU's 5-Year EPS Expansion: 20.77%

This number puts Intuit directly within Lynch's desired range. It shows a good history of profit expansion that is solid but not so high it might be temporary. This history of turning sales into profits is an important first step for a GARP investor, indicating the company has a workable and repeatable business model.

Price Measured by the PEG Ratio

Lynch was known for using the Price/Earnings to Growth (PEG) ratio to see if a stock's price is fair relative to its expansion rate. A PEG ratio of 1 or less was his standard for a sensible price, meaning the market might not be paying too much for future expansion.

- INTU's PEG Ratio (Past 5Y): 0.82

With a PEG ratio clearly below 1, Intuit meets this important Lynch standard. This measure indicates that, compared to its past profit expansion, the stock is not priced too high. For an investor using this strategy, it gives a numerical reason that the company's expansion possibility may not be completely seen in its present share price.

Earnings Power and Financial Condition

Lynch stressed investing in companies that are not only expanding but are also basically healthy and run well. His filter includes standards for high return on equity (ROE) and a careful debt setup.

- Return on Equity (ROE): 21.31%

- Debt-to-Equity Ratio: 0.28

An ROE above 15% shows that Intuit's leadership is very good at creating earnings from shareholder investment, a mark of high-quality operations. Also, a debt-to-equity ratio much lower than the filter's limit of 0.6 (and even Lynch's more careful liking of 0.25) points to a cautious balance sheet. The company is financed mainly by investment rather than debt, which lowers money risk and gives steadiness—a key factor for long-term holdings. The company also has a good current ratio of 1.39, showing enough cash to cover near-term needs.

Basic Analysis Summary

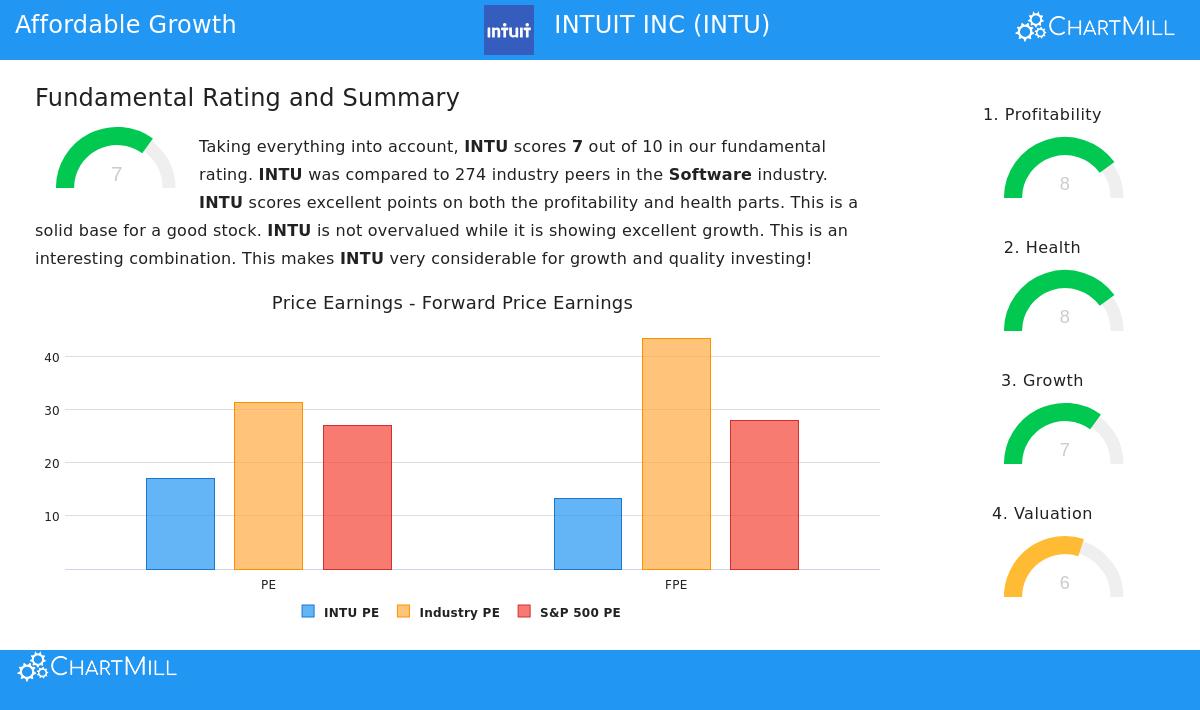

A wider view of Intuit's basic rating, which gets a 7 out of 10, supports the image shown by the Lynch filter. The company receives high scores for earnings power and financial condition, with notable measures like Return on Invested Capital (ROIC) and a good Altman-Z score pointing to low failure risk. Its expansion profile stays solid, with good past and projected future growth in both sales and EPS.

On price, the report shows a varied but mostly positive view. While the usual P/E ratio looks high by itself, measures that compare Intuit to other software companies or that adjust for expansion—like the forward P/E and Enterprise Value/EBITDA—indicate the stock is priced more favorably relative to the market and its industry. You can see the full, itemized basic analysis for INTU here.

A Choice for the Long-Term Portfolio

Intuit’s description matches several of Peter Lynch's idea-based preferences. It works in an area many investors can grasp—tax preparation and small business accounting software—through leading names like TurboTax and QuickBooks. This "invest in what you understand" point is a Lynch signature. The company's business model creates repeat sales and gains from a lasting competitive advantage, traits that help support lasting long-term expansion.

For investors making a portfolio based on the Growth at a Reasonable Price idea, Intuit offers a strong argument. It joins a history of solid, lasting profit expansion with a price that seems sensible when expansion is considered, all supported by high earnings power and a very strong balance sheet. It represents the kind of company Lynch might call a "reliable performer"—a steady expander deserving of a long-term investment.

Want to look at other companies that meet the Peter Lynch filter? You can find the present list of passing stocks and use the filter yourself with this link: Peter Lynch Strategy Stock Screen.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The analysis uses past data and particular investment methods, which do not promise future outcomes. Investors should do their own study and talk to a qualified financial advisor before making any investment choices.