For investors looking for a mix of solid increase and fair prices, the Growth at a Reasonable Price (GARP) or "affordable growth" method presents a good middle path. This method tries to find companies that are not only showing good, lasting increase but are also priced at levels that do not completely account for that future possibility. It avoids both risky, very costly increase stories and very low-priced companies with little future. A useful way to apply this is by searching for stocks with high scores in increase, earnings, and money strength, while making sure the price score stays fair, showing the market has not become too optimistic.

INTUIT INC (NASDAQ:INTU) stands out as a top choice from this kind of search. The company behind TurboTax, QuickBooks, and Credit Karma shows a picture that fits well with the affordable growth idea, mixing very good business results with a price that seems careful compared to its future.

Increase: A History of Increase

The center of any increase investment is, expectedly, increase. Intuit’s basic numbers show a company that has been performing very well on this front and is predicted to keep doing so.

- Past Results: Over the last year, Intuit increased its Revenue by 15.63% and, more notably, its Earnings Per Share (EPS) by 23.74%. The longer-term averages are even more notable, with Revenue increasing at 19.65% and EPS at 20.77% each year.

- Future Predictions: Expert forecasts suggest this speed is not ending. Revenue is predicted to increase at an average of 12.57% each year in the next few years, while EPS is forecast to rise by 15.50%. While these future guesses show a slowing from the outstanding past speeds, they still point to a "quite strong" speed of increase.

This steady double-digit increase across important money measures highlights Intuit's skill to grow its main tax and small business software platforms while successfully adding and growing newer buys like Mailchimp and Credit Karma.

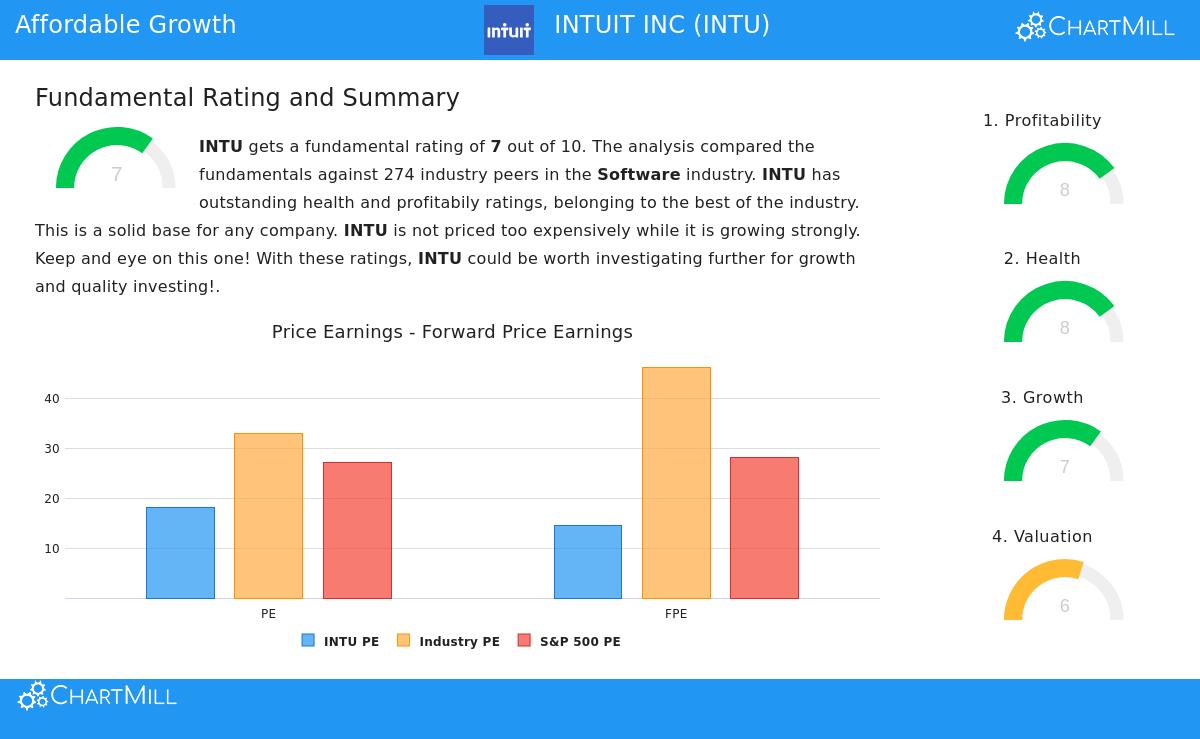

Price: Fair Compared to Quality

A high-increase profile often comes with a high cost. However, the affordable growth method specifically looks for cases where that high cost is not too high. Intuit’s price measures suggest it is in this area.

- Earnings Measures: Intuit trades at a Price/Earnings (P/E) ratio of 18.02. While this alone might seem high, the full picture is important. This ratio is clearly lower than the wider S&P 500 average (27.11) and much below the average for its software industry group (32.87).

- Future-Looking and Relative Price: The view becomes sharper with future-looking measures. Its Price/Forward Earnings ratio of 14.60 is also a discount to both the S&P 500 (28.13) and the industry (46.19). Also, other price measures like Enterprise Value to EBITDA and Price/Free Cash Flow show Intuit is priced lower than about 75-78% of its industry rivals.

This relative price position is key for the GARP method. It shows the market sees Intuit's quality but may not be fully counting its continued increase path, especially when compared to more highly priced sector peers.

The Supporting Parts: Earnings and Money Strength

Lasting increase at a fair price cannot exist without a strong base. Intuit gets high scores here, which supports its price and lowers investment risk.

- Very Good Earnings: The company gets a high earnings score, led by top-level margins. Its Operating Margin of 26.72% and Return on Invested Capital (ROIC) of 16.53% do better than nearly 90% of the software industry. High earnings means increase is effectively turned into profits, a key point for quality increase stocks.

- Good Money Strength: Intuit keeps a strong balance sheet, shown in a high strength score. Its debt amounts are workable, with a Debt-to-Free Cash Flow ratio under 1, meaning it could in theory pay off all its debt with less than a year's cash flow. A strong Altman-Z score also points to very low failure risk. This money strength gives the stability to put money into future increase projects and handle economic slowdowns.

Conclusion

Intuit shows the traits wanted by the affordable growth investor. It displays a strong mix of proven past increase, good future predictions, and industry-leading earnings, all held up by a very strong money base. Importantly, this set is available at a price that, while not "low" in simple terms, is a clear discount to both the whole market and its own high-flying industry. This difference between operational quality and relative price is the core of the GARP chance.

For investors wanting to look at other companies that fit this picture of good increase, decent earnings and strength, and fair price, more results can be found using the Affordable Growth stock screener.

Disclaimer: This article is for information only and is not money advice, a suggestion to buy or sell any security, or a support of any investment method. Investors should do their own study and talk with a qualified money advisor before making any investment choices. The basic analysis talked about is given by ChartMill and can be seen in full here.