There’s nothing quite like checking your portfolio after a company delivers a blowout quarter, only to find the stock down double digits.

It’s like a company beating earnings across the board, only to see its stock drop because the CFO didn’t smile enough during the guidance call.

That’s exactly what happened this week with GitLab (NASDAQ: GTLB). The company reported stellar Q1 FY2026 results — revenue up 27% year-over-year, a massive beat on EPS, and record free cash flow. But the market? It wasn’t impressed. The stock plunged over 10% in a single day.

At first glance, it seems like one of those classic market tantrums. So I did what any long-term investor with a stubborn streak would do: I dug in. And the more I read, the more convinced I became that this sell-off is more opportunity than omen.

Let’s Look at the Numbers

GitLab pulled in $214.5 million in revenue, beating both analyst estimates and its own guidance. Non-GAAP EPS came in at $0.17, versus just $0.03 a year ago. That’s a 467% increase. Not a typo.

Operating margin? Now in positive territory at 12% on a non-GAAP basis, a huge improvement from -2% last year. Free cash flow hit $104 million, also a record.

In short: GitLab is growing, it’s turning the corner toward profitability, and it’s doing it while maintaining high gross margins (~90%).

So what was the problem?

The Market Hates Being Bored

GitLab’s guidance for the next quarter and full fiscal year was solid. They guided Q2 revenue to $226–227 million and full-year revenue to $936–942 million. That’s above Wall Street expectations. But here's the catch: the growth rate is slowing.

Instead of 27% YoY growth like this quarter, we’re looking at something closer to 20% going forward. Still respectable, but in a market that throws tantrums like a toddler denied dessert, that’s apparently a dealbreaker.

As Warren Buffett famously said:

“The stock market is a device for transferring money from the impatient to the patient.”

Well, Mr. Market just handed long-term investors like me a gift.

Technically Speaking…

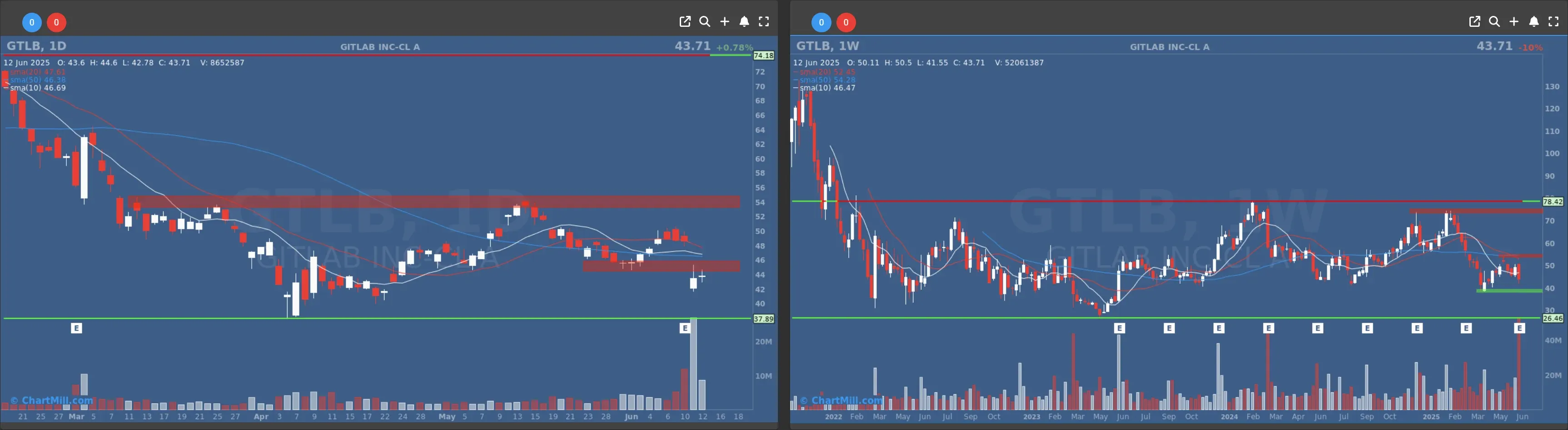

If you’re a chart-watcher, GitLab’s technical setup looks… not great. The price fell out of a consolidation range, broke below key support around $46, and is now hovering dangerously close to $38, a level that’s acted as strong support in the past.

There’s a decent chance the stock retests that level or dips a little lower. In the short term, it’s broken. But as Peter Lynch reminded us:

“Far more money has been lost by investors preparing for corrections, or trying to anticipate corrections, than has been lost in the corrections themselves.”

That’s why I don’t mind averaging in slowly. No one rings a bell at the bottom.

So Why Am I Buying?

Here’s the thing: GitLab is building something meaningful. Their AI-native DevSecOps platform is hitting all the right notes at a time when software development, security, and automation are converging faster than ever. They’re being used by over 50% of the Fortune 100. Their customer base is growing, and existing customers are spending more, net retention is 122%.

This isn’t some speculative hype train. It’s a company with real revenue, real growth, and now, real profitability.

Sure, Wall Street wanted more hypergrowth. But I’m more than happy with consistent, sustainable growth and improving margins. GitLab is executing, and they’re doing it with discipline.

Final Thoughts

Short-term traders saw slowing growth and hit the sell button. I saw expanding margins, strong cash flow, a moat forming in enterprise DevOps, and a valuation that just got a lot more attractive.

Could the stock go lower in the coming weeks? Absolutely. But five years from now, I suspect I’ll be glad I started buying here.

I’ll be doing just that.

Walter Shares, ChartMill