Investors aiming to assemble a lasting portfolio of good companies at fair prices frequently consider the ideas of famous fund manager Peter Lynch. His method, explained in One Up on Wall Street, centers on finding expanding companies with sound finances and durable business models, yet importantly, ones the market has not valued too highly. This "growth at a reasonable price" (GARP) method steers clear of speculative, expensive stocks for businesses with established earnings, controlled debt, and prices that do not assume many years of future gains. A central measure in this system is the PEG ratio, which evaluates a stock's price-to-earnings (P/E) ratio against its earnings growth rate, a number at or under 1 often marking a fair price.

A recent filter using Lynch's main standards has identified Enphase Energy Inc (NASDAQ:ENPH) as a possible option for this kind of investor. The company, a worldwide frontrunner in microinverter-based solar and battery systems, seems to match many of the method's numerical checks.

Match with Peter Lynch Standards

The filter uses particular checks to locate companies with a mix of expansion, fair price, and monetary soundness. Enphase Energy's present numbers show a clear match:

- Durable Earnings Expansion: Lynch preferred companies with solid but not extreme expansion, usually from 15% to 30% each year, as very fast growth is frequently not maintainable. Enphase states a 5-year average EPS growth rate of 20.06%, putting it directly within this desired zone and indicating a record of steady, controlled increase.

- Fair Price via PEG Ratio: Maybe the most important Lynch measure is the PEG ratio, which modifies the standard P/E ratio for growth. A PEG of 1 or less implies the market may not be completely valuing the company's growth path. Enphase's PEG ratio, calculated from its last 5-year growth, is about 0.50, showing a possible large price reduction compared to its past earnings growth.

- High Earnings Power (ROE): Return on Equity (ROE) calculates how well a company produces earnings from shareholder funds. Lynch searched for high earnings power, with an ROE over 15% being a typical mark. Enphase's ROE of 19.66% easily meets this mark, indicating good management and a possible lasting edge.

- Sound Monetary Condition: The method stresses companies with good balance sheets to endure economic changes.

- The Current Ratio of 2.04 shows Enphase has more than sufficient immediate assets to pay its immediate debts, meeting Lynch's need for monetary steadiness.

- The Debt-to-Equity ratio of 0.57 is under the filter's maximum of 0.6, indicating the company is not too dependent on debt. Lynch himself liked an even smaller ratio, but this number still points to a fairly careful financial setup.

Basic Profile Summary

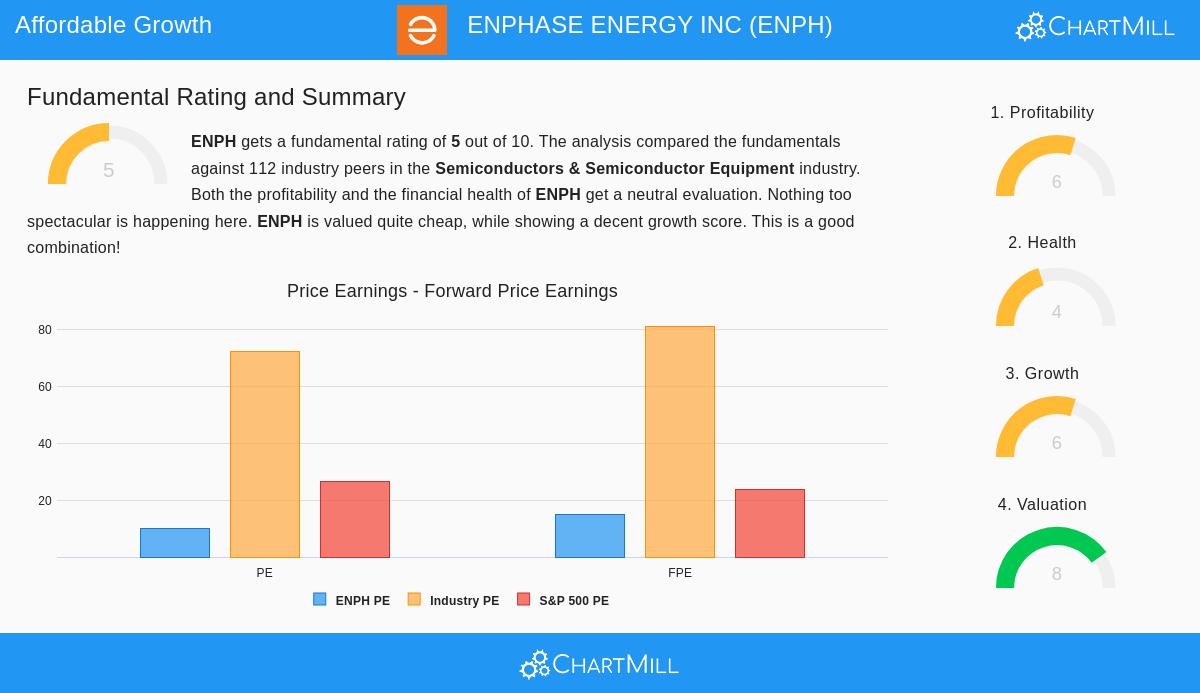

A look at Enphase's wider basic analysis report gives background beyond the filter's checks. The company gets an overall basic score of 5 out of 10, showing a varied but notable profile when measured against others in the Semiconductors & Semiconductor Equipment field.

- Earnings Power & Expansion: The company gets a 6 for earnings power, helped by a strong ROE and acceptable profit margins, although these margins have faced recent reduction. Its expansion score is also a 6, supported by very strong past EPS and sales growth over the last five years. Still, experts forecast a marked reduction in both earnings and sales growth for the next few years, a point of care for investors.

- Price Strength: This is where Enphase is most distinct. It gets a high price score of 8. Its P/E ratio of about 10 is low compared to both the field average and the wider S&P 500. This small earnings multiple, paired with its past growth, is what creates its notable PEG ratio.

- Monetary Condition Points: The company's condition score is a middle 4. While it has good cash availability (as shown in the Current Ratio), its debt amounts and Altman-Z score are points of attention, indicating a balance sheet that is sufficient but not outstandingly strong.

You can review the complete, itemized analysis in the Enphase Energy Basic Analysis Report.

Points for Investment

For an investor using a Peter Lynch-style GARP method, Enphase Energy offers a notable example. It shows the signs of a company that has reached marked expansion and high earnings power, but is now priced by the market at a level that does not appear to completely account for this record. The small PEG ratio is the numerical focus of this view. Also, the company works in the long-term expansion area of clean energy technology, supplying products that allow home energy self-reliance, a market with a lasting favorable trend.

However, the Lynch method also needs knowing the business. Possible investors must evaluate if the forecasted reduction in growth is a short-term field challenge or a more lasting change. Also, while the debt amount passes the filter's check, watching the company's financial borrowing will be key. The method’s good result depends on keeping shares during swings, if the central business idea stays valid.

Locating Comparable Options

Enphase Energy resulted from a methodical search built on Peter Lynch's ideas. For investors curious about finding other companies that meet these standards for maintainable growth at fair prices, the filter is a practical beginning for more study.

You can see and adjust the active Peter Lynch Strategy filter here.

Note: This article is for information only and is not financial guidance, a suggestion, or a plan to buy or sell any security. Investing holds risk, including the chance to lose the original amount. You should do your own full study and think about talking with a registered financial consultant before making any investment choices.