Wednesday’s tape felt like a reality check for the AI trade.

Chip and software leaders got hit hard after AMD’s outlook disappointed, while investors quietly rewarded steadier “old economy” names.

Under the surface, soft private payrolls and mixed services data kept macro anxiety alive, even as oil jumped on renewed Iran-related geopolitical tension.

The day’s defining move: a sudden loss of faith in AI pricing

If you only looked at the index closes, you’d think this was just another wobbly risk-off session.

But the real story was concentration risk: once the market decided AI expectations were a bit too perfect, the selling got surgical, fast.

The Nasdaq sank early before trimming losses into the close, a classic “panic first, think later” pattern.

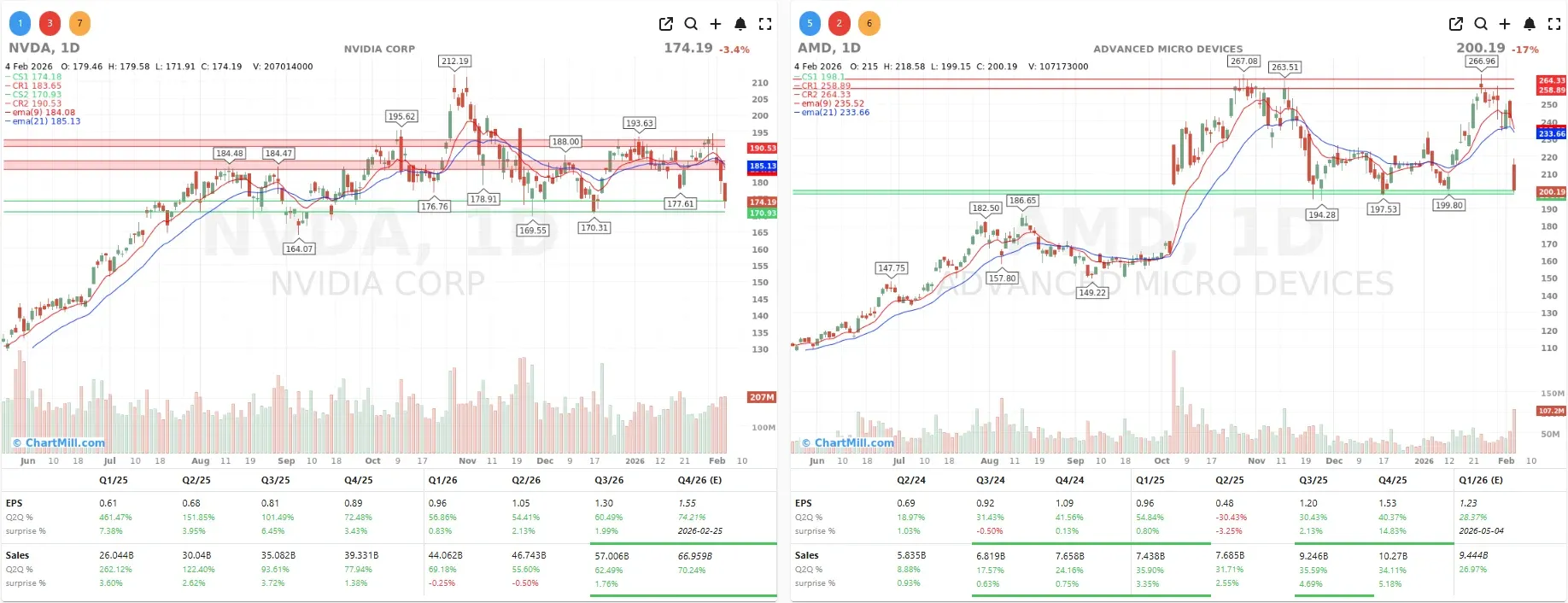

AMD shocks the room, Nvidia catches the collateral damage

Advanced Micro Devices (AMD | -17.31%) delivered the kind of forecast that doesn’t forgive lofty positioning, and the stock was punished accordingly.

Nvidia (NVDA | -3.41%) slid in sympathy, and the whole AI-compute complex traded as if investors suddenly wanted proof - not promises - that the datacenter buildout can keep compounding at the pace markets have priced in.

“Software exodus” vibes return—Palantir becomes the poster child

The selloff wasn’t limited to semis.

Palantir (PLTR | -11.62%) gave back optimism in a hurry, echoing a broader fear I keep hearing from investors: that smarter AI agents could compress the pricing power of legacy software models faster than Wall Street is ready to model.

Whether that fear is right or premature, it’s clearly influencing positioning this week.

Alphabet’s numbers impress, but capex steals the headline

Alphabet (GOOGL | -2.20%) was already weak into the close, and then came the after-hours twist: strong results paired with a very large investment plan that underscores how expensive “staying in the AI race” is getting.

The market now has to balance real growth in Cloud demand against the uncomfortable truth that the bill for AI infrastructure is accelerating.

Big Tech wasn’t uniformly punished

It wasn’t “sell everything with a mega-cap label.”

Apple (AAPL | +2.60%) stood out on the upside, while Microsoft (MSFT | +0.72%) eked out gains.

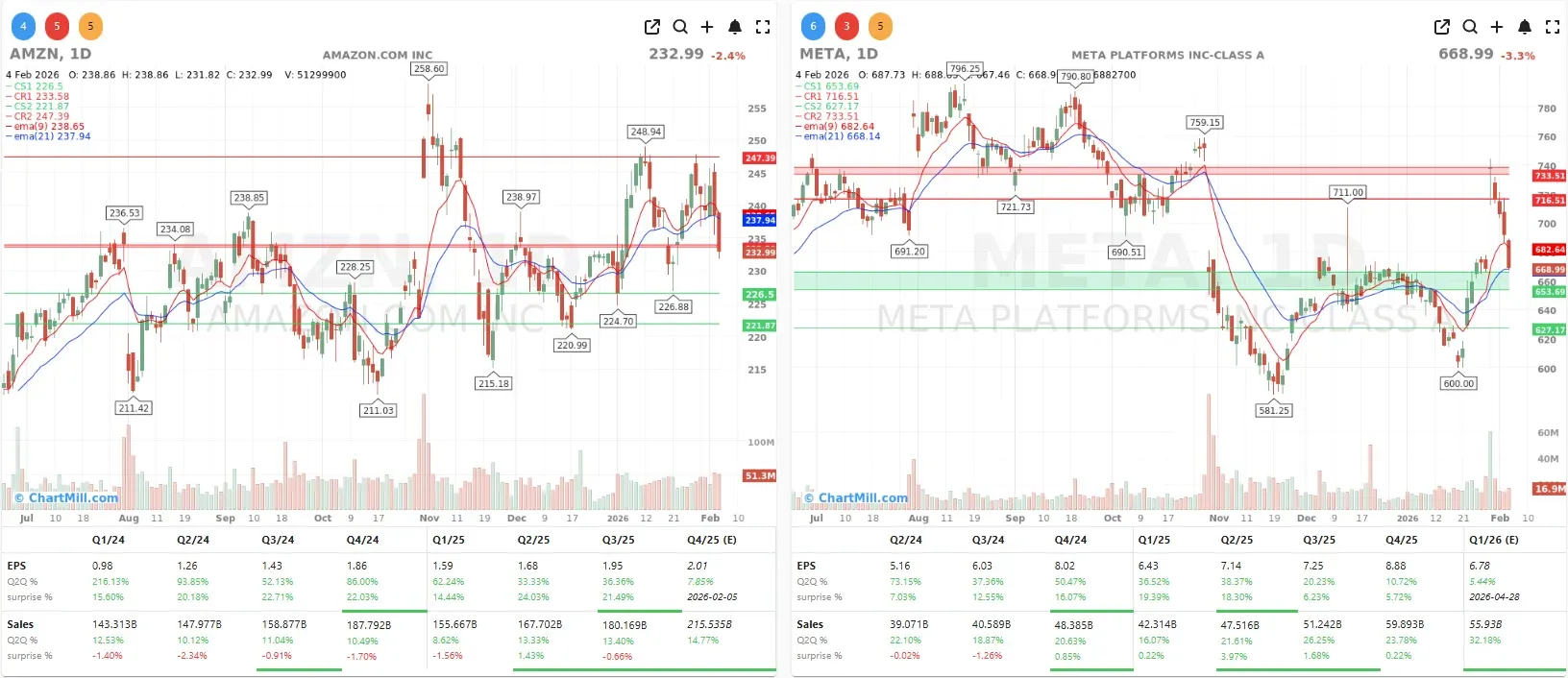

Meanwhile, Amazon (AMZN | -2.36%) and Meta Platforms (META | -3.28%) stayed in the line of fire with the rest of the AI-adjacent complex, and Alphabet’s capex messaging only amplified the market’s sensitivity to spending intensity.

The rotation message got louder: Dow strength, value leadership

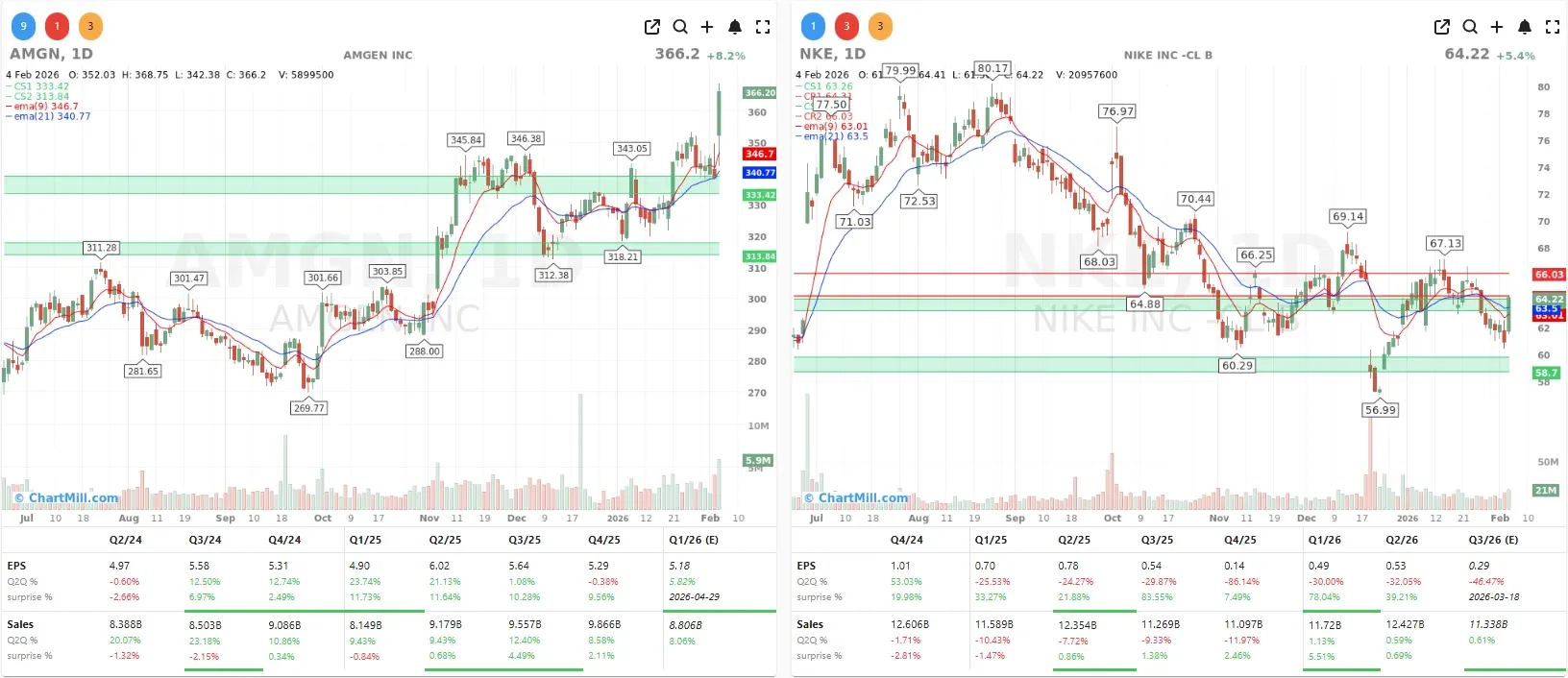

This is the part I don’t ignore: while growth was wobbling, “less-AI, more-cashflow” stocks did real work.

Amgen (AMGN | +8.15%), Nike (NKE | +5.40%), and 3M (MMM | +5.21%) helped keep the Dow resilient. And the rotation isn’t theoretical anymore, Walmart (WMT | +0.23%) recently pushed into the $1T club, a milestone that fits the narrative of investors paying up for scale, stability, and execution.

Earnings did what earnings are supposed to do: create dispersion

A few company moves were impossible to miss.

Eli Lilly (LLY | +10.33%) jumped after a standout report and upbeat outlook, while Super Micro Computer (SMCI | +13.78%) surged as AI-server demand translated into strong results.

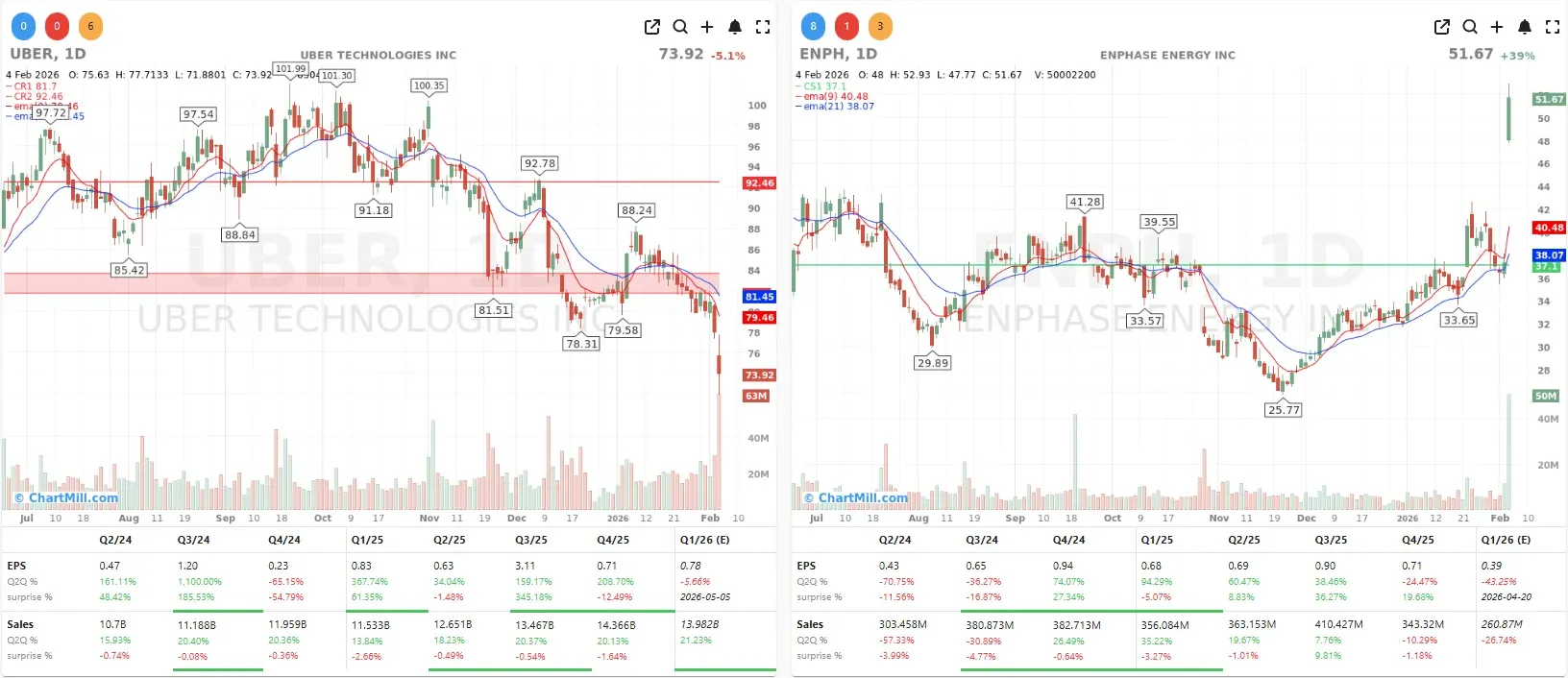

Enphase Energy (ENPH | +38.60%) ripped higher on better-than-expected numbers and a stronger outlook, while Uber (UBER | -5.15%) slid on softer profitability and cautious guidance.

Macro and geopolitics: soft hiring, steady services, oil pops

On the macro front, ADP showed just 22,000 private jobs added in January, well below expectations, keeping the labor narrative uneasy. At the same time, services data still pointed to expansion (more “steady” than “hot”).

Then geopolitics hit commodities: oil jumped after planned U.S.–Iran talks were thrown into doubt, raising the temperature around supply-risk pricing.

Bitcoin slides again and forced selling anxiety creeps back in

Bitcoin’s drop reintroduced an old fear: when leveraged holders get stressed, price declines can become self-reinforcing. The move matters less for crypto purists and more for cross-asset sentiment, because in nervous markets, investors tend to sell what they can, not just what they should.

Conclusion

My takeaway from Wednesday is simple: the market isn’t abandoning AI, but it is downgrading “infinite runway” assumptions, especially where guidance, valuations, and spending intensity collide.

At the same time, rotation into steadier earners is real, and it’s acting like a pressure valve: when the AI trade stumbles, capital doesn’t have to leave equities, it just has to find a different story.

Kristoff - ChartMill

Next to read: Breadth Wobbles as Mega-Cap Tech Leads the Pullback