A Fragile Bounce to End a Turbulent Week

Some Fridays simply feel heavier than others, this one certainly did.

After four straight sessions of tech-driven anxiety, the Nasdaq managed to claw its way back into the green, closing up 0.1%, even though it opened nearly 1.8% lower. In a week where confidence evaporated faster than Bitcoin in a risk-off mood, this tiny gain was the closest thing investors got to a victory lap.

Still, the pain was real: the Nasdaq ended the week down 0.5%, its worst stretch since early autumn.

What saved the day? One word, Nvidia. The semiconductor giant single-handedly kept the tech complex from breaking down entirely. Investors, myself included, are watching Wednesday’s earnings with the kind of nervous excitement usually reserved for medical test results.

A beat could rekindle AI optimism. A miss… well, let’s just say I hope your seatbelt is functional.

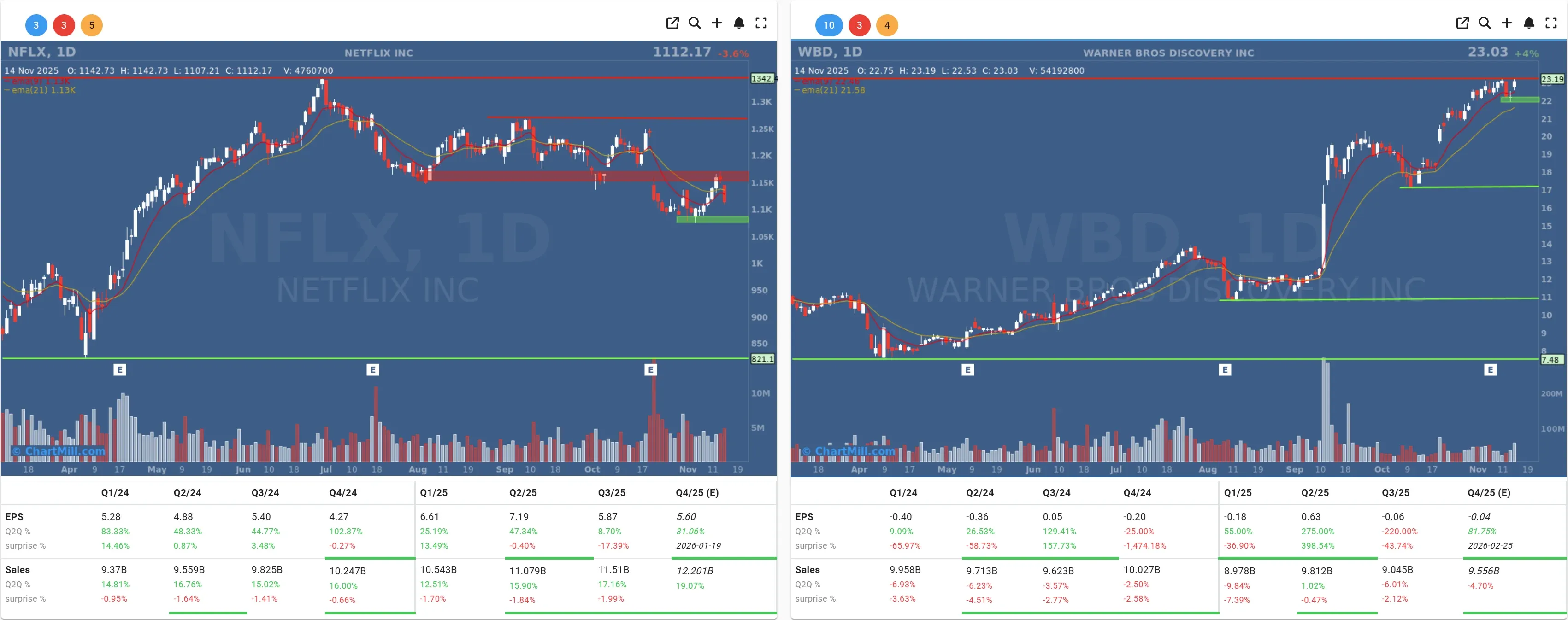

Netflix Takes Center Stage With a Rumored $75 Billion Gamble

While AI valuations steal the headlines, Netflix (NFLX | -3.64% pre-split) decided to spice things up with what may become the boldest M&A move of the decade. According to The Wall Street Journal, the streamer is preparing a $75 billion bid for Warner Bros. Discovery (WBD | +4.02%).

To put that into perspective: that’s 19× the company’s expected 2026 EBITDA. Even in a world where tech valuations regularly break the sound barrier, that’s a heavy lift.

Paramount Skydance (PSKY | +2.02%) and Comcast (CMCSA | -1.64%) are also reportedly circling WBD, turning the media landscape into an episode of Succession nobody asked for.

And as if that wasn’t enough news for one weekend, Netflix executed a 10-for-1 stock split after the close. Shares are now trading around $111 instead of $1,110, same valuation, just more “affordable” for employee stock plan participants. This marks the company’s third split following similar moves in 2004 and 2015.

Despite the recent sell-off triggered by an unexpected tax bill, Netflix remains up roughly 25% YTD, outperforming legacy rivals by a mile.

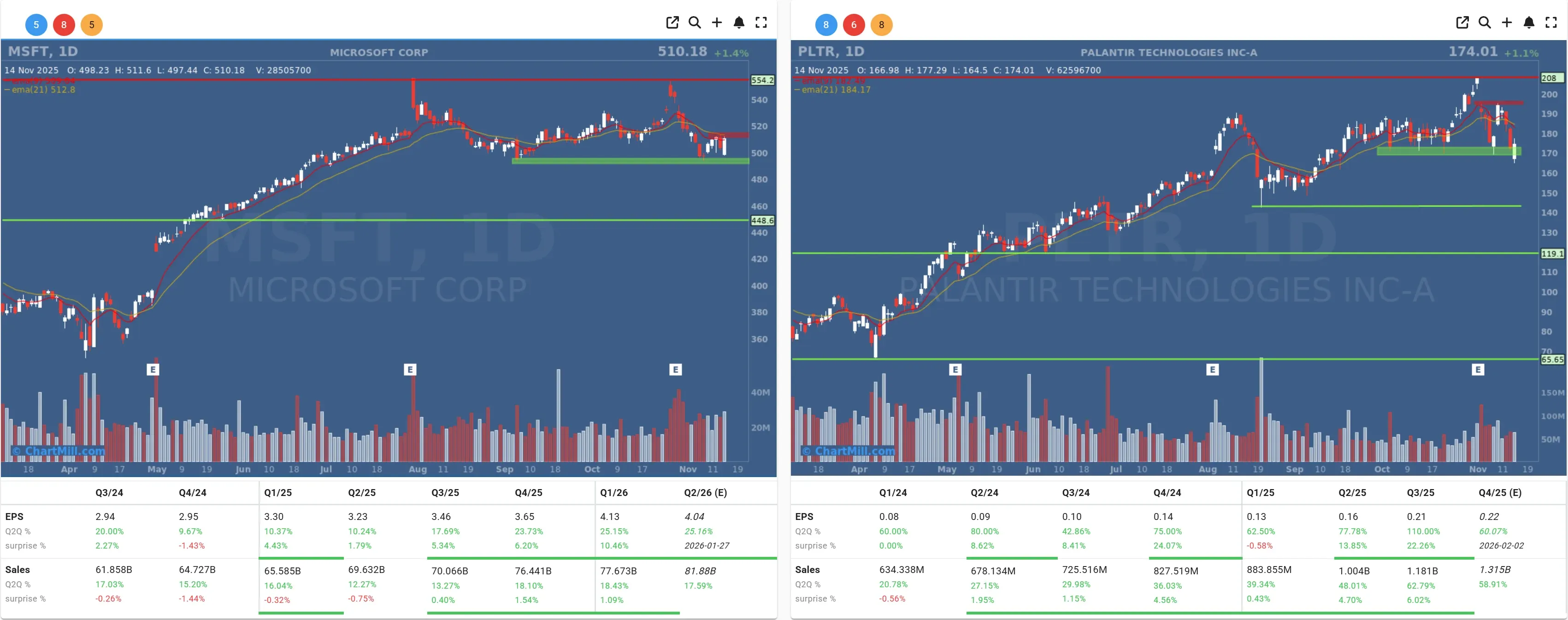

Tech Rebounds… But AI Valuation Fears Still Linger

While Nvidia was the main driver, other megacaps helped shape Friday’s rebound. Microsoft (MSFT | +1.37%) and Palantir (PLTR | +1.09%) both found buyers after a week of pressure.

But don’t mistake this for broad enthusiasm.

Underneath the surface, the AI trade is showing cracks. With the sector priced for perfection, many investors - including institutional desks - are openly questioning whether AI momentum, heavy government spending, and potential monetary easing can realistically synchronize into a new global growth cycle.

Friday’s tone made one thing painfully clear: confidence in the “AI forever” narrative is cooling.

Fed Doubts Grow as December Rate Cut Odds Slip

The macro picture didn’t help. The market-implied probability of a December rate cut dropped to 46%, according to CME FedWatch data. Confidence took a hit as Fed officials continued to deliver a cautious - and at times contradicting - message.

Add in the government shutdown, which delayed key releases including retail sales and producer prices, and Friday’s macro calendar felt like someone forgot to show up for their shift.

What we did see:

-

10-year Treasury yields ticked slightly higher

-

EUR/USD slid to 1.1623

-

Gold fell more than 2% on Friday but still logged a +2% weekly gain

-

Bitcoin dropped to $94,000

-

Oil surged more than 2%, boosted by a Ukrainian drone strike on a Russian Black Sea oil port

In short: a lot of noise, not much clarity.

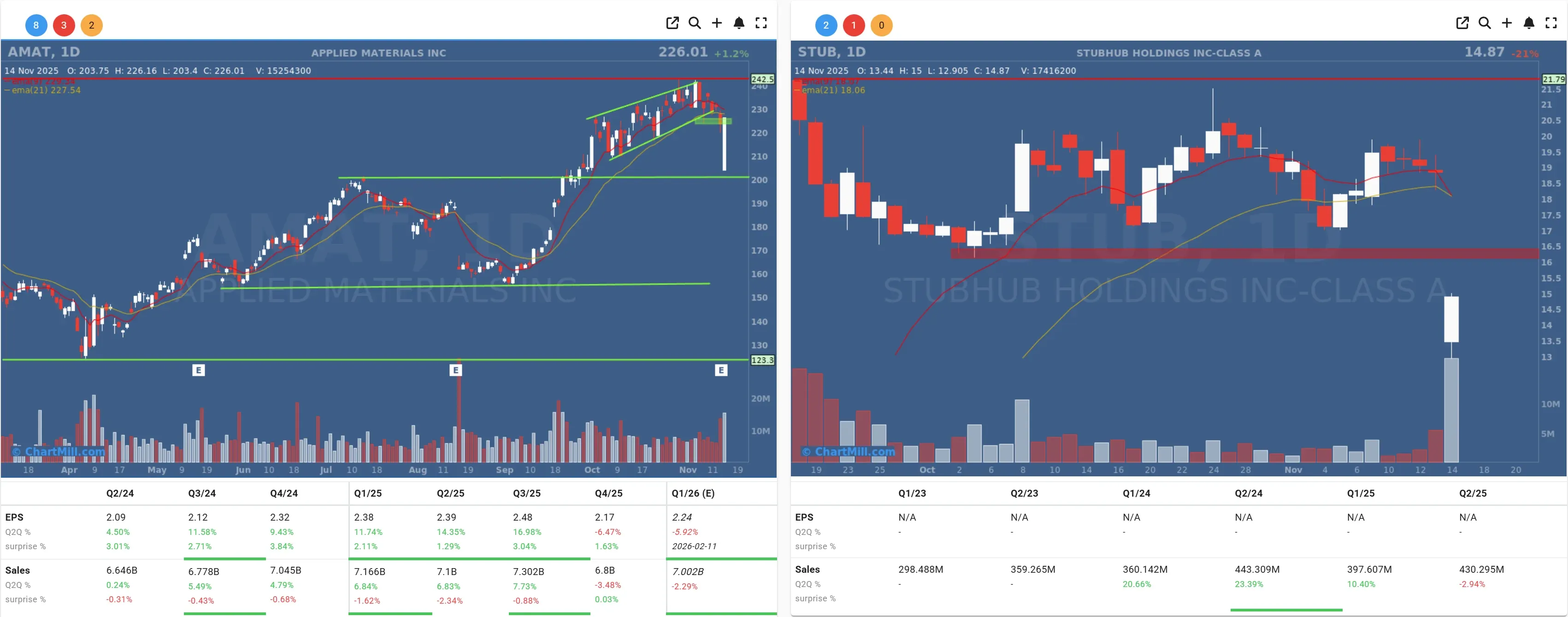

Notable Movers

Applied Materials (AMAT | +1.25%)

The chip-equipment maker rose after delivering a solid quarterly update. With AI-related capex booming worldwide, AMAT remains one of the quiet beneficiaries of the broader tech build-out.

StubHub (STUB | -20.99%)

The ticketing platform cratered after refusing to provide forward guidance, never a great look, especially after losing over $1 billion. Investors reacted exactly as you’d expect.

Berkshire Hathaway’s Portfolio Shuffle

In its latest 13F filing, Berkshire Hathaway (BRK.B | -0.81%) revealed:

-

A new 17.8 million-share position in Alphabet (GOOGL), valued at $4.3B

-

A sale of 41.8 million Apple (AAPL) shares

-

Total Q3 activity: $12.5B sold, $6.4B purchased—marking the 12th consecutive quarter of net selling

This signature Buffett discipline comes just as the Oracle of Omaha prepares to hand the reins officially to Greg Abel at year-end.

A symbolic shift in an era where tech continues to dominate global markets.

Final Thoughts

Friday’s rebound felt more like a breather than a turning point. With Nvidia’s earnings looming and rate-cut doubts rising, the market is entering a week where sentiment could swing wildly and fast.

If you’re positioned heavily in AI names, buckle up. If you’re not positioned at all… grab popcorn.

Kristoff - ChartMill

Next to read: Market Breadth Softens Further Despite Prior Stabilization