A wild metals-and-crypto wobble tried to steal the spotlight, but Wall Street basically shrugged and bought stocks anyway.

A surprise rebound in U.S. manufacturing set the tone, while a handful of high-profile names reminded everyone that “earnings season” is just another way to say “expect emotional whiplash.”

The key message from Monday’s tape: cyclicals and mega-cap “comfort stocks” led the charge, while anything tied to speculative risk (crypto equities) or uncertain narratives (some AI adjacencies) got treated with a bit more suspicion.

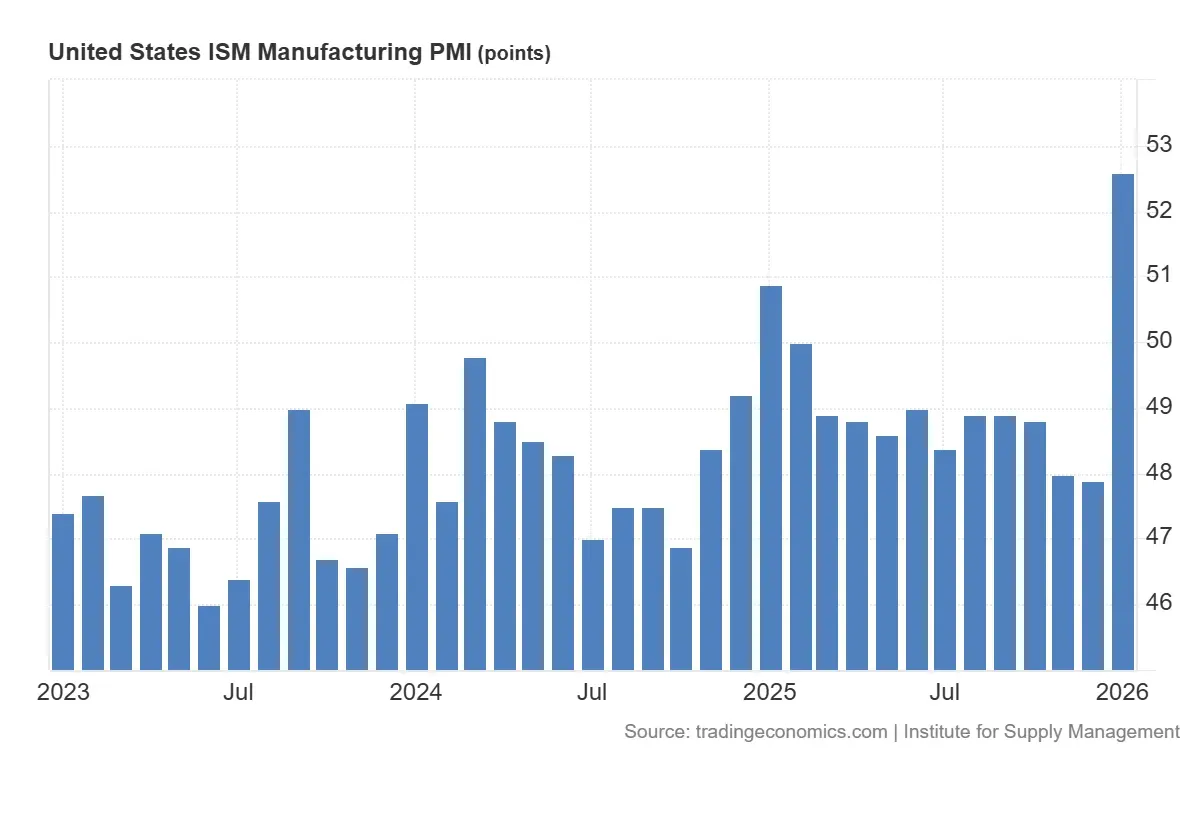

The data point that flipped the mood: ISM says “expansion”

The day’s most important catalyst wasn’t a product launch or a spicy CEO quote, it was a macro print.

U.S. manufacturing activity (the ISM manufacturing index) jumped to 52.6 in January, a sharp rebound that pushed the gauge back into expansion territory (above 50) and well above expectations.

In plain English: factories suddenly looked a lot less sleepy than the market had priced in.

That kind of surprise tends to do two things fast:

-

it boosts confidence that the economy can keep absorbing higher rates/yields, and

-

it sends investors hunting for “real economy” winners.

And that’s exactly how the session traded.

Industrials and “everyday economy” stocks did the heavy lifting

The clearest beneficiary was Caterpillar (CAT | +5.10%), which acted like the poster child for “manufacturing is back, baby.”

Meanwhile, the market also piled into familiar, liquid bellwethers, names that sit at the intersection of consumer spending and institutional comfort:

When you see this combo rally together, I read it as: investors want upside exposure, but they want it in “known quantities.”

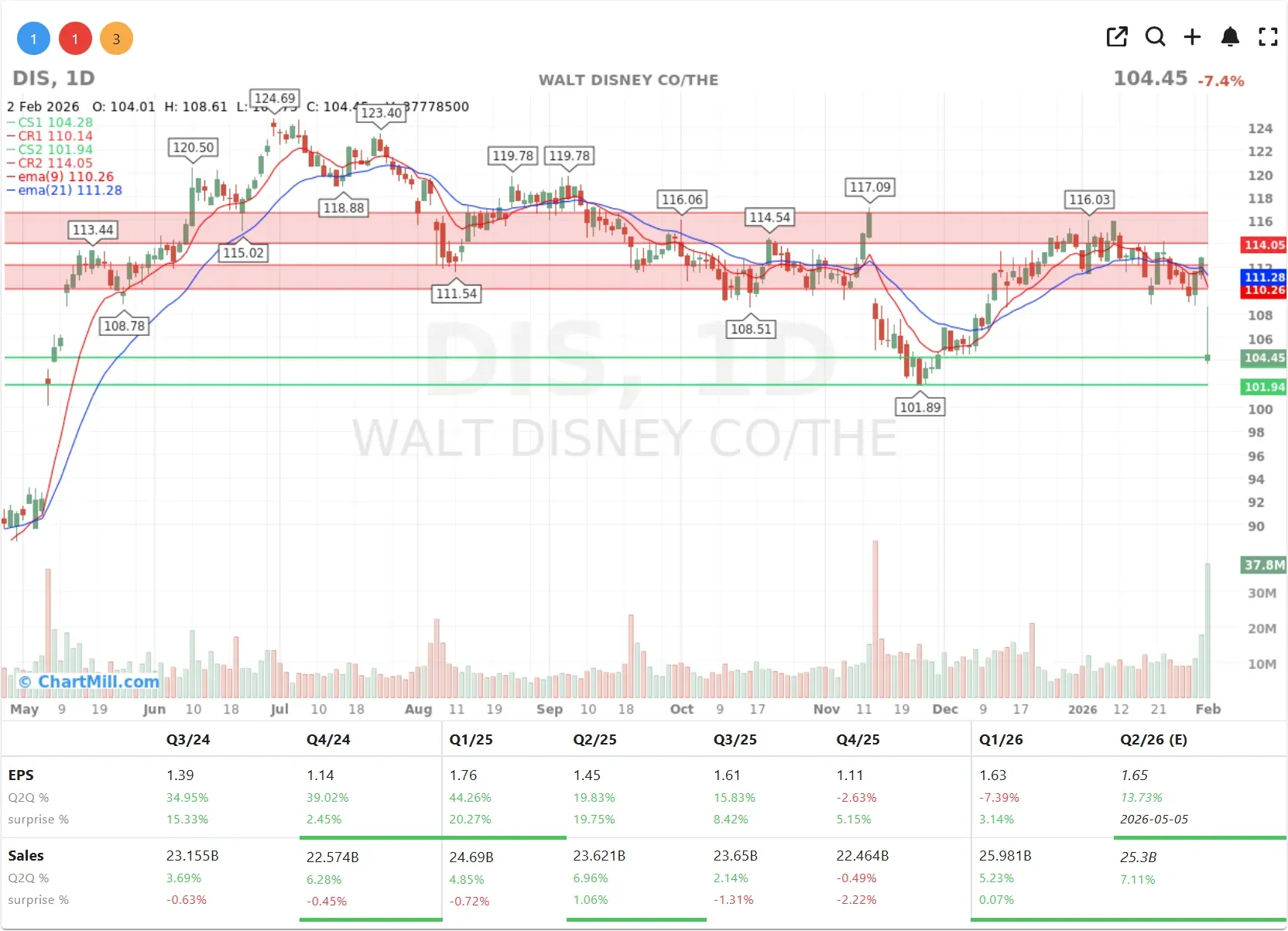

Disney: good quarter, bad vibes

Disney (DIS | -7.40%) delivered a fundamentally solid update - revenue grew and parks held up - but the stock still got smacked because the forward view spooked investors, particularly around theme-park attendance trends and softer international visitation.

This is the kind of earnings reaction I don’t ignore: it’s not about what Disney did, it’s about how little patience the market has for any uncertainty in guidance right now.

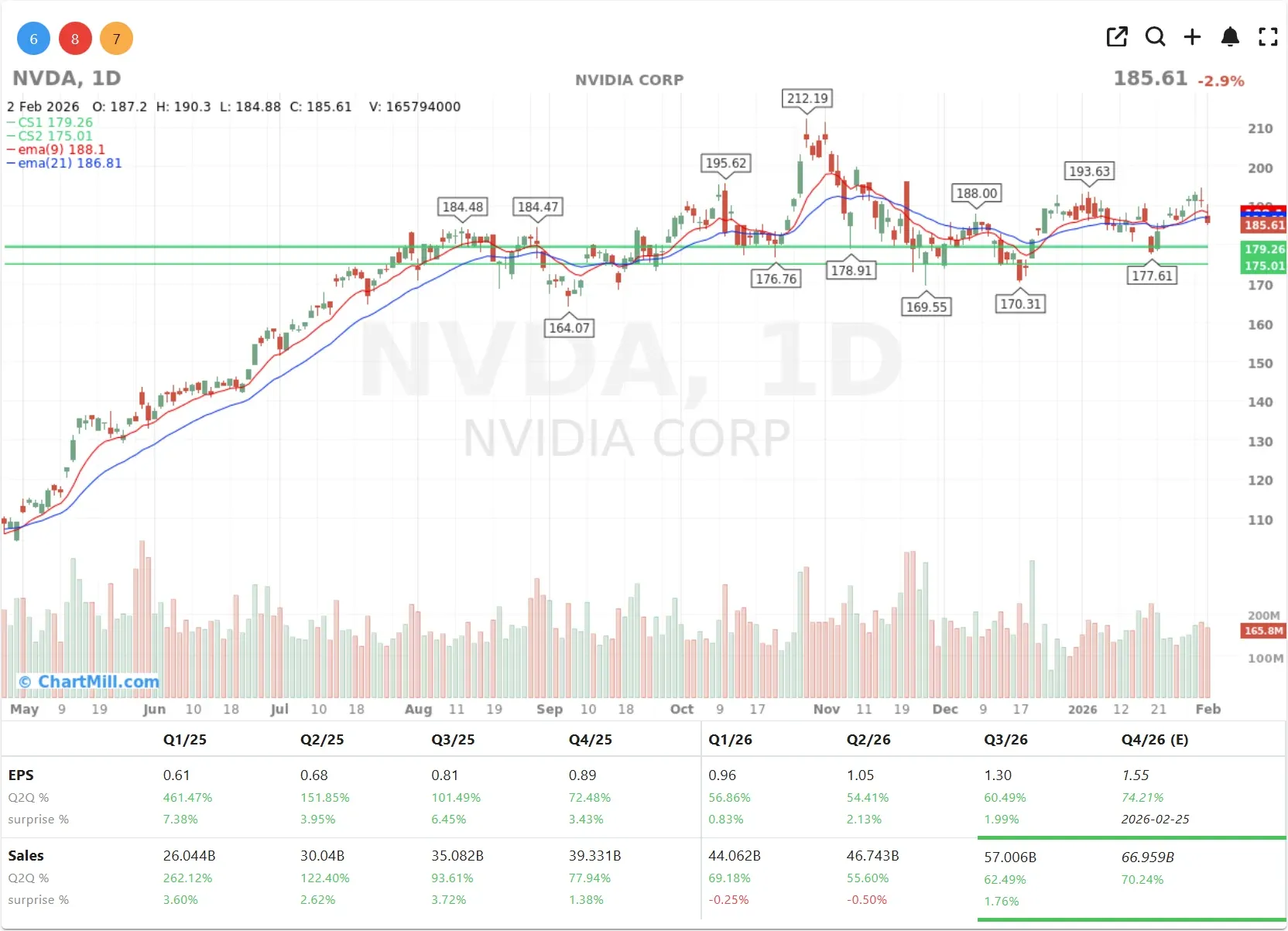

Nvidia and the AI narrative: markets hate “maybe”

Nvidia (NVDA | -2.89%) didn’t join the party, and the reason was refreshingly simple: uncertainty.

The market is re-pricing the probability (and scale) of Nvidia’s mooted investment arrangement with OpenAI after reports and commentary suggested the “up to $100 billion” idea isn’t exactly a signed-and-sealed commitment. Investors can live with risk; they just prefer risk with a spreadsheet attached.

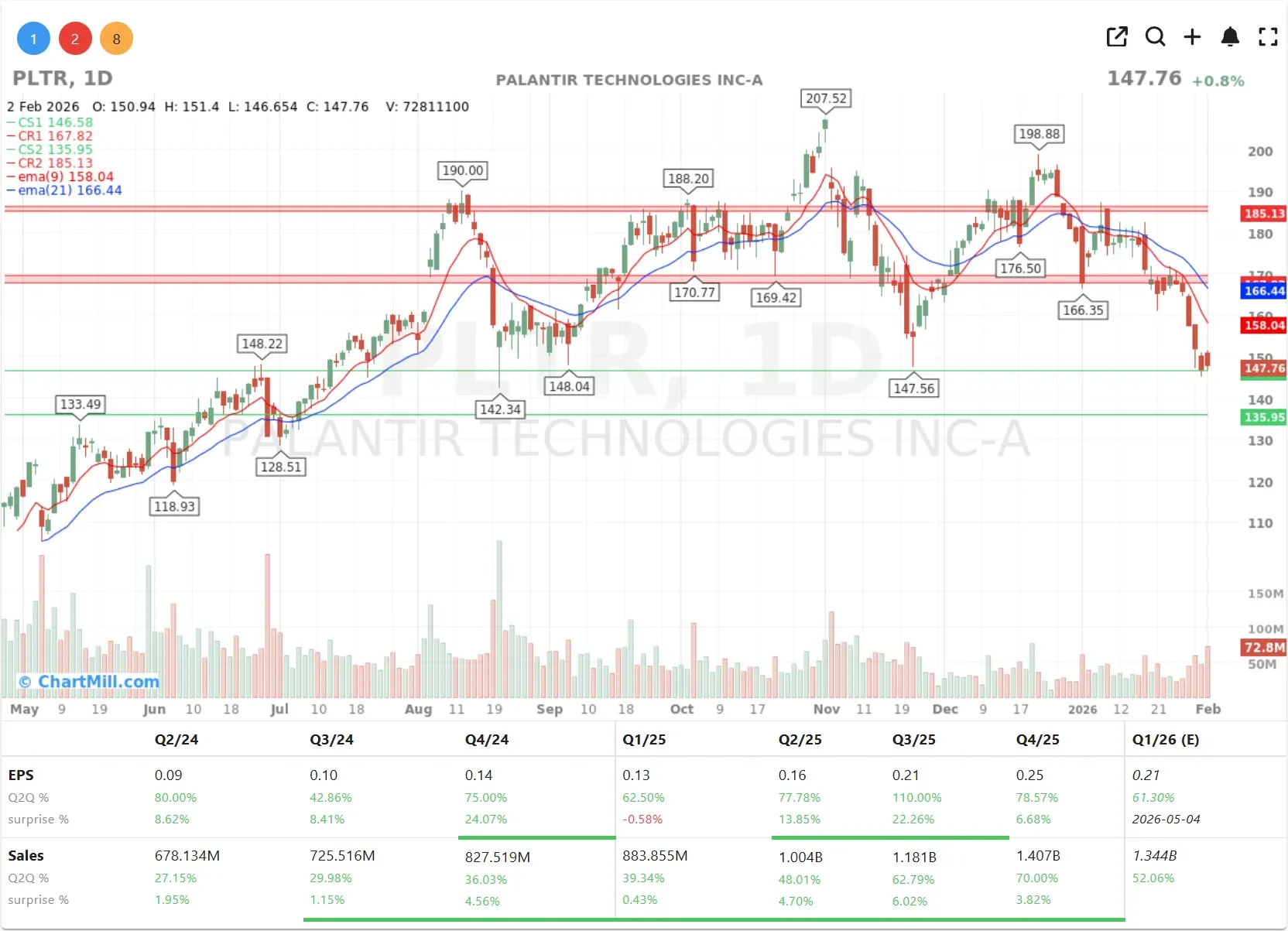

Palantir after the bell: growth is still a drug

In after-hours, Palantir (PLTR | After Hours +10.86%) grabbed the mic with results showing sharply accelerating growth and bullish guidance for 2026 revenue, numbers that came in ahead of what analysts were modeling. The stock reaction was immediately positive in late trading.

I’d summarize the takeaway like this: while parts of “software” have been in the penalty box, the market will still pay up for a company that can print real growth and tie it convincingly to AI demand.

Metals and crypto: a reminder that “risk” hasn’t disappeared

Even with stocks higher, the backdrop wasn’t calm. Precious metals have been swinging violently, and bitcoin dipped below $80,000 over the weekend before stabilizing.

Crypto-linked equities reflected that risk-off undertone:

-

Strategy (MSTR | -6.73%)

-

Coinbase (COIN | -3.53%)

-

Robinhood Markets (HOOD | -9.62%)

This split - stocks up, speculative corners down - is exactly what “selective risk appetite” looks like.

Policy and geopolitics: tariffs, minerals, Iran… and a shutdown wrinkle

A lot of Monday’s headlines were political, but investors mostly treated them as directional nudges rather than full-blown regime shifts (for now).

U.S.–India trade surprise

Donald Trump and Narendra Modi surfaced a trade framework that includes tariff reductions and a pledge by India to stop buying Russian oil, while committing to large purchases of U.S. goods.

“Project Vault” and the rare-earth complex

Trump also pushed a plan to create a strategic stockpile of critical minerals - headline number: $12 billion - aimed at insulating supply chains and reducing reliance on China. This helped spark interest in U.S.-listed rare-earth and critical-minerals names, even if individual stock reactions were mixed by the close.

One example: MP Materials (MP | +0.58%, After Hours +4.04%) held onto a small gain. And USA Rare Earth (USAR | -1.38%, After Hours +4.70%) was volatile on the day as the story spread across pre-market and intraday trading.

The Metals Company (TMC | +0.08%, After Hours +3.70%) was essentially flat.

Oil slid on Iran de-escalation talk

Crude gave back geopolitical premium after Trump signaled Iran was “seriously” talking with Washington, pushing Brent down sharply on the day.

The jobs report gets delayed

And the wonky-but-important operational detail: a partial U.S. government shutdown is delaying the January employment report. That doesn’t change the economy, but it does change how confidently the market can price the next few macro steps.

What I’m taking into Tuesday

If Monday had a slogan, it was: “strong data beats noisy cross-asset volatility.” The rally was broad enough to feel real, but selective enough to tell me investors are still allergic to ambiguity, whether that’s Disney’s forward view or Nvidia’s OpenAI chatter.

If the next batch of economic prints confirms manufacturing’s bounce and earnings keep clearing the bar, this tape can stay constructive. But if metals/crypto instability spreads into credit or volatility markets, equities won’t be able to pretend it’s background noise forever.

Kristoff - ChartMill

Next to read: Bounce Day, But Participation Still Playing Catch-Up