Merry (slightly belated) Christmas and happy New Year!

After a holiday pause since December 23, the market came back like someone hitting “refresh” on a browser tab that never fully loaded: lots of motion, not much agreement. Semiconductors did the heavy lifting, mega-cap tech mostly sulked, and Tesla reminded everyone that “expectations management” is also a sport.

The tape: a volatile “hello” to 2026

The first trading day of 2026 was basically a mood swing in chart form: early green, mid-day wobble, and a close that looked calm only if you ignore the intraday rollercoaster. The Dow (+0.66%) finished higher, the S&P 500 (+0.19%) eked out a small gain, and the Nasdaq Composite (-0.03%) ended essentially flat.

Semis: the only party on Wall Street (and it was a good one)

If you were long semiconductors, you started 2026 the way everyone wanted to start 2026.

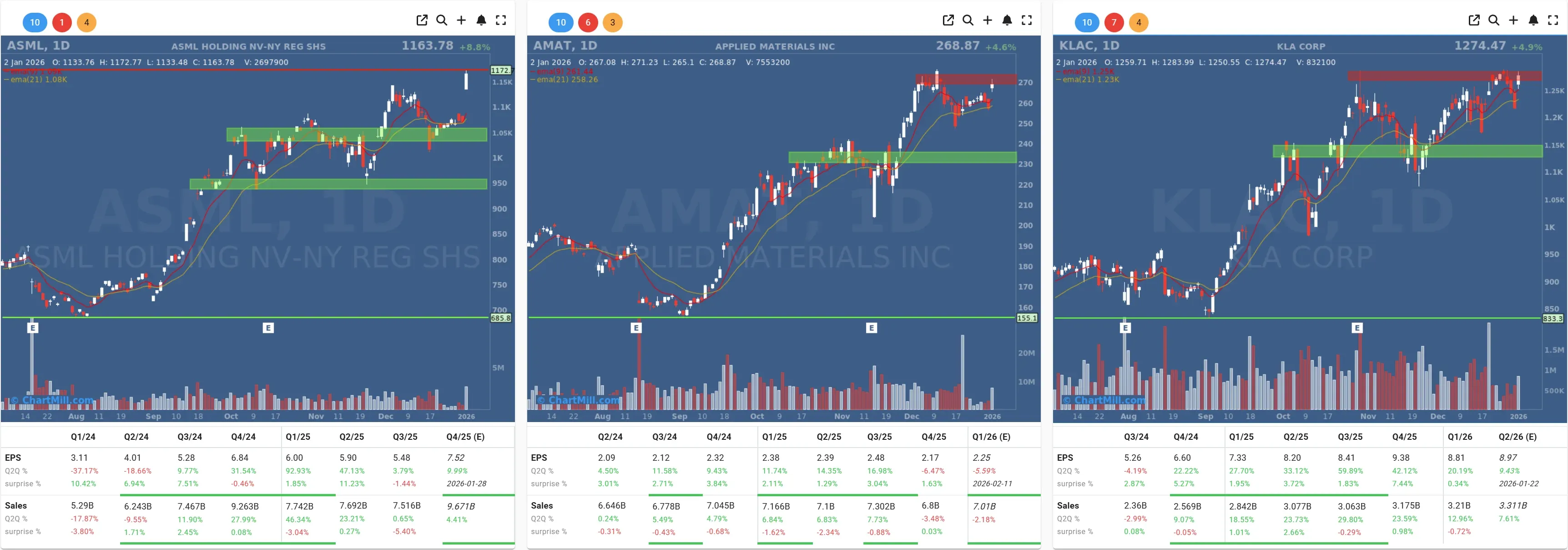

ASML (ASML | +8.78%) ripped higher after a notable tone shift from Aletheia Capital, an upgrade to Buy and a sharply higher price target, leaning on demand for EUV tools (and the memory cycle improving).

And once ASML moves, sympathy trades tend to show up on time. Applied Materials (AMAT | +4.62%) and KLA (KLAC | +4.89%) followed it higher, like they were attached by an invisible “semi-capex” rubber band.

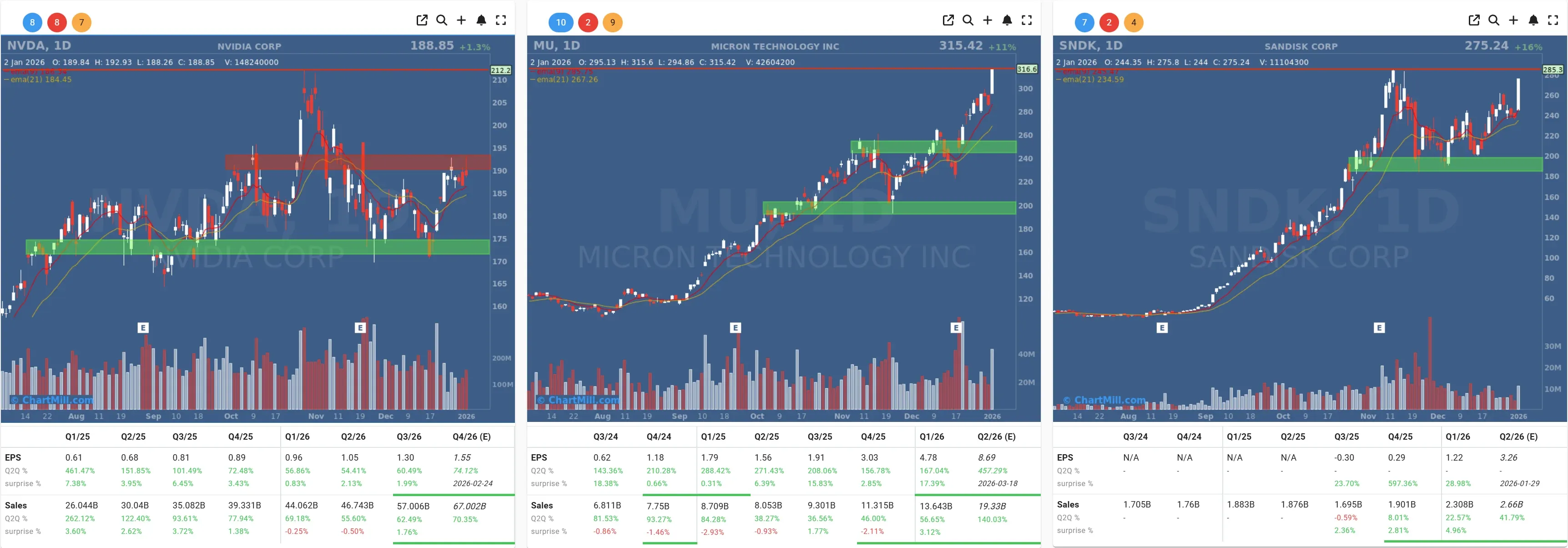

The memory complex was even louder: Micron (MU | +10.51%) surged, and Sandisk (SNDK | +15.95%) jumped hard as investors latched onto improving sentiment out of Asia and the broader memory narrative.

That “Samsung is back” line wasn’t just a nice New Year’s slogan, either, Samsung’s messaging around memory leadership and AI-era ambitions helped reinforce the idea that the memory downcycle might be in the rear-view mirror. Samsung Electronics rallied in Seoul alongside that renewed confidence.

Even within the Magnificent crowd, Nvidia (NVDA | +1.26%) was one of the few names that managed to stay on the right side of the tape.

Mega-cap reality check: Tesla stumbles, and big tech doesn’t catch it

While semis were doing push-ups, several mega-cap tech names were… not.

Amazon (AMZN | -1.87%) and Microsoft (MSFT | -2.21%) took noticeable hits, which is one reason the S&P’s move looked so modest despite all that semiconductor strength.

Then came the headline that actually changed something fundamental: Tesla (TSLA | -2.59%) reported Q4 deliveries of 418,227 vehicles, below what many on the Street were looking for. Tesla itself highlighted Q4 deliveries “over 418,000” and production “over 434,000.”

The market reaction wasn’t subtle: Tesla finished down on the day, and the broader EV space didn’t exactly inspire confidence either.

EV cross-currents: Rivian steadies

Rivian (RIVN | -1.52%) posted Q4 production of 10,974 and deliveries of 9,745, numbers that were broadly in line with what traders expected, but the stock still drifted lower.

My takeaway: the EV trade is drifting from “category growth” toward “category selection.” The market is becoming less forgiving about misses and more willing to reward operational momentum.

Macro backdrop: PMI says “expanding,” but the vibe says “careful”

-

The macro read wasn’t recession-y, but it wasn’t exactly champagne either. The S&P Global U.S. Manufacturing PMI for December was confirmed at 51.8, still in expansion (>50) but softer than the prior month’s pace.

-

On the markets side, the euro weakened to 1.1721 USD per EUR on January 2.

-

Commodities were more “watching and waiting” than “breaking out”: oil eased slightly as supply concerns tugged against geopolitical risk (Ukraine/Venezuela staying in the headline rotation).

Policy ripple: a tariff pause lifts furniture retail

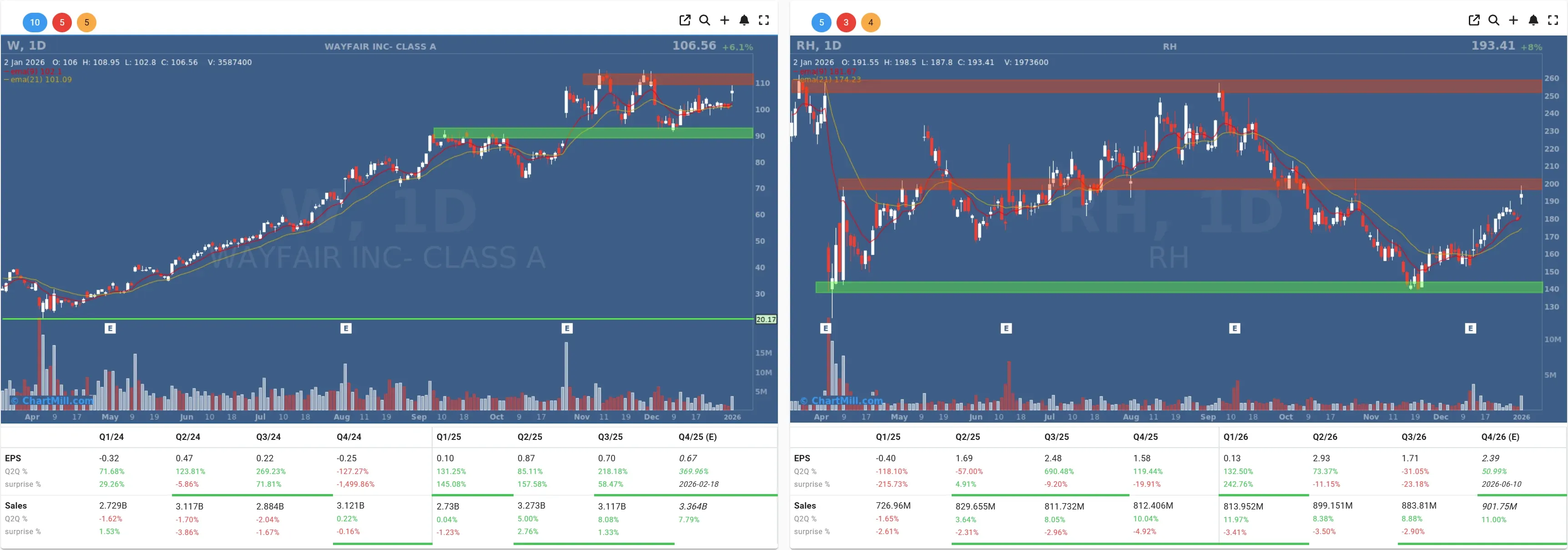

One of the more “wait, that matters?” drivers: the White House delayed planned tariff increases on certain finished wood products (including upholstered furniture, kitchen cabinets, and vanities) for an additional year.

The market’s immediate translation: margin pressure gets postponed. Wayfair (W | +6.12%) and RH (RH | +7.96%) both caught a bid.

The day’s weirdest shrug: AppLovin

AppLovin (APP | -8.24%) was the S&P’s ugly outlier. Sometimes the market gives you a clean narrative; sometimes it just takes your momentum stock and throws it down the stairs.

What I’m watching into Monday (Jan 5)

Because this is the first update back after the holidays, I’m paying extra attention to what could change the tape quickly:

- Energy + geopolitics: Over the weekend, Venezuela headlines escalated materially, and crude moved lower despite the geopolitical shock, suggesting the market is leaning “supply/demand first, drama second.”

- Do semis keep carrying the market? Friday looked like a “chips save the indices” day. If that leadership fades, the broader market may feel a lot heavier.

- Positioning reset: The first week of January often brings portfolio rebalancing behavior that can amplify moves, especially in last year’s winners and crowded momentum names.

That’s the setup: semis flexing, mega-cap tech wobbling, EVs turning into a stock-picker’s game, and macro saying “fine… but don’t get cocky.”

Kristoff - ChartMill

Next to read: Happy New Year - Breadth Starts 2026 With a Rebound, But the Short-Term Trend Still Needs Repair