The Iran conflict tightens its grip on markets as the Dow joins the Nasdaq in correction territory, Meta reels from a double legal knockout, and a surprise AI data leak rattles the entire cybersecurity sector.

The Rundown

- Markets in correction: Dow ▼1.73%, Nasdaq ▼2.15%, S&P 500 ▼1.67%, all at seven-month lows

- Iran war escalates: Strait of Hormuz closed, oil briefly tops $100 (WTI) and Brent hits $112.57

- First earnings casualty: Carnival slashes 2026 profit guidance, blaming a 60% surge in fuel costs

- Meta double legal blow: $381M in verdicts across two child safety trials; thousands more lawsuits in the pipeline

- Anthropic "Mythos" leak: Accidental data leak reveals a next-gen AI model with advanced cyber capabilities, cybersecurity stocks drop 6%

- Bright spots: Exxon and Chevron up on higher oil; gold rises 3%+; Brown-Forman surges on Pernod Ricard merger talks

- Consumer mood souring: UMich confidence falls; inflation expectations rise to 3.8%

When war starts dictating earnings guidance, you know things have gotten serious.

That's exactly where we find ourselves after Friday's close, a session that felt less like a trading day and more like a triage exercise for portfolios exposed to energy, tech, and social media.

Indices Deep in the Red and Getting Worse

The three major averages all closed lower on Friday. The Dow Jones Industrial Average lost 793.47 points, or 1.73%, to end at 45,166.64. The S&P 500 dropped 1.67% to close at 6,368.85, and the Nasdaq Composite fell 2.15% to settle at 20,948.36. A market that is systematically breaking down under the weight of geopolitical uncertainty.

The Dow, S&P 500, and Nasdaq each closed at their lowest level since August. The Nasdaq extended losses after closing in correction territory on Thursday, now more than 12.5% below its record high from October.

The S&P 500 dropped 3.4% across Thursday and Friday combined, its worst two-day drop since April last year, when tariff uncertainty shook markets. And just to underscore the technical damage: all three major stock indexes have now fallen below their 200-day moving averages, a threshold that traders widely consider the long-term "ultimate trendsetter" in financial markets.

Iran: The Overhang That Won't Lift

The root cause hasn't changed - it's still the Iran war - but it is intensifying. The Strait of Hormuz has been closed by Iran's Revolutionary Guard, with traffic through this critical waterway to be punished with severe measures.

Two Chinese vessels were refused passage early Friday morning, and a Thai cargo ship ran aground in the waterway.

President Trump extended the deadline for attacking Iranian energy infrastructure to April 6, posting on Truth Social that talks are proceeding well. But even with the extension, investors now appear to want to see an actual resolution rather than promises that one might be coming.

The gap between diplomatic language and hard facts is exactly the kind of ambiguity that markets hate most.

The oil market is pricing that risk accordingly. Brent crude rose 4.22% to $112.57 per barrel, settling at its highest level since the war began. West Texas Intermediate climbed 5.5% to $99.64, briefly touching above the psychologically important $100 mark.

Should the conflict drag on through the end of June, a scenario currently assigned roughly a 40% probability by Macquarie strategists, crude could potentially reach $200 per barrel. That's a number that would make the current market pain look modest by comparison.

Carnival: The First Real Earnings Casualty

Carnival (CCL | ▼4.31%), the cruise giant slashed its full-year earnings per share guidance from $2.48 to $2.21, directly blaming the surge in fuel costs which are now running at an annual bill of approximately $2.15 billion.

Because Carnival doesn't hedge its fuel exposure, every additional dollar per barrel of crude lands directly on their bottom line. Sector peers Royal Caribbean (RCL | ▼4.45%) and Norwegian Cruise Line (NCLH | ▼6.85%) got swept along in the selloff.

I'll be watching this space closely. Carnival is likely the first of many corporates to downgrade guidance on energy costs, and this wave of profit warnings could become a major headwind for the broader market in the weeks ahead.

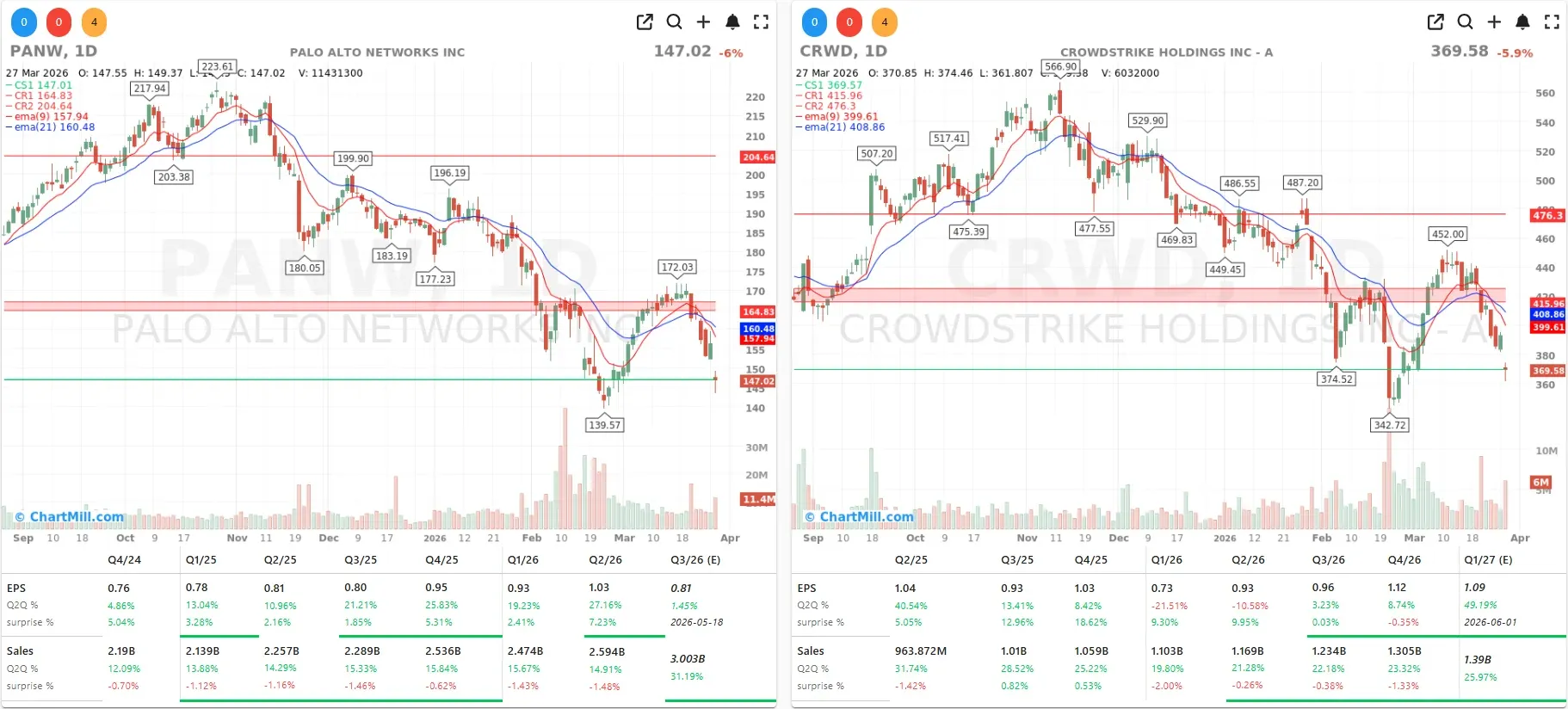

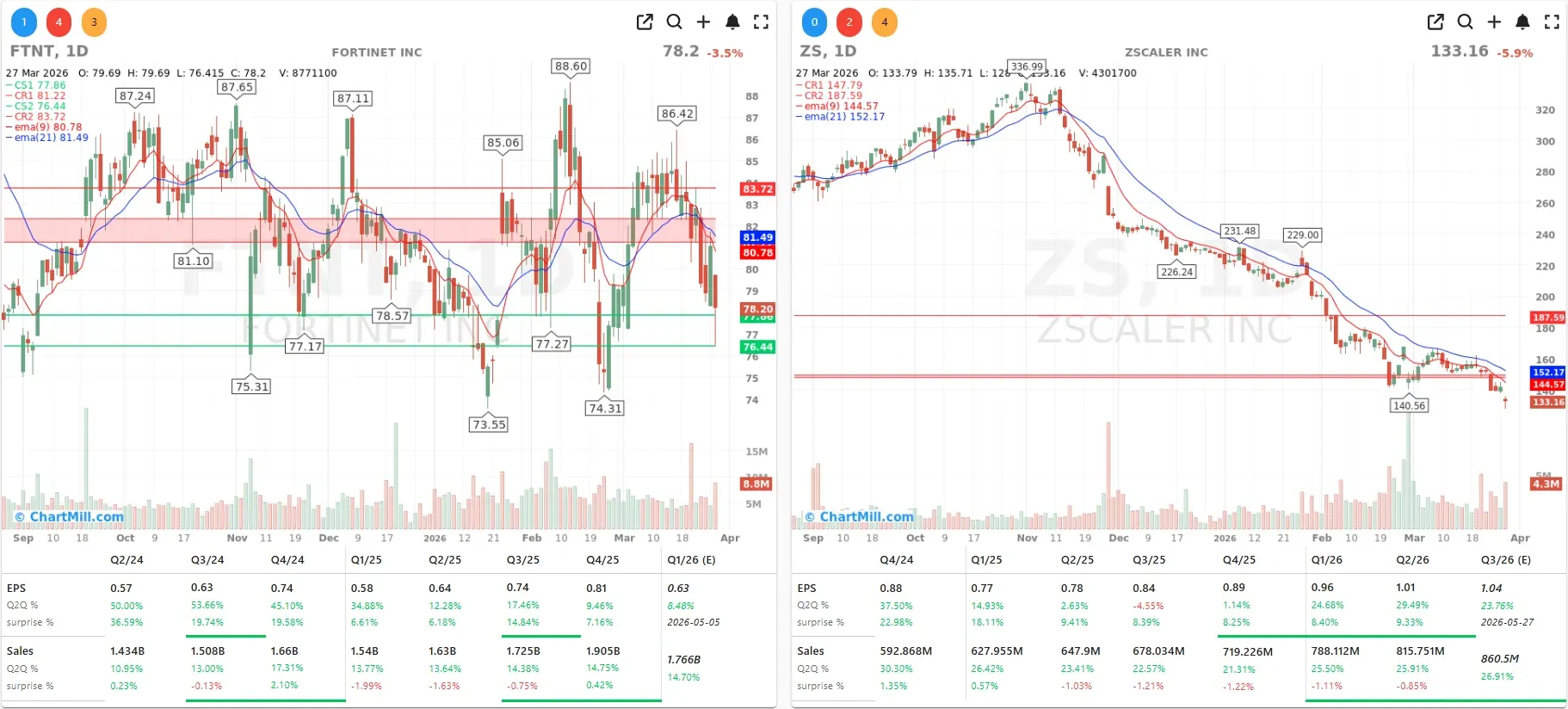

Anthropic's "Mythos" Leak Torpedoes Cybersecurity Stocks

The most unexpected story of the session didn't come from the Middle East, it came from a misconfigured content management system at AI lab Anthropic.

A data leak caused by a major security lapse in Anthropic's public-facing CMS revealed that the company is working on a powerful new model called "Claude Mythos," which it has since officially acknowledged, describing it as a "step change" in performance and its "most capable model to date."

The leaked draft blog post introduced a new model tier called "Capybara," described as larger and more capable than the existing Opus models.

According to the document, Capybara achieves dramatically higher scores than Claude Opus 4.6 on tests of software coding, academic reasoning, and cybersecurity. That last capability is the one that set off alarm bells. The document warned that the system could pose serious cybersecurity risks, pointing to its ability to identify and exploit software vulnerabilities rapidly.

The irony of a company building the world's most advanced cybersecurity AI leaking that fact through a basic configuration error is not lost on anyone, but the market consequences were entirely serious.

Palo Alto Networks (PANW | ▼5.97%), CrowdStrike (CRWD | ▼5.87%), Zscaler (ZS | ▼5.9%), and Fortinet (FTNT | ▼3.49%) all took heavy losses as investors grappled with what a model far ahead of every other AI system in offensive cyber capabilities means for incumbents in the security space.

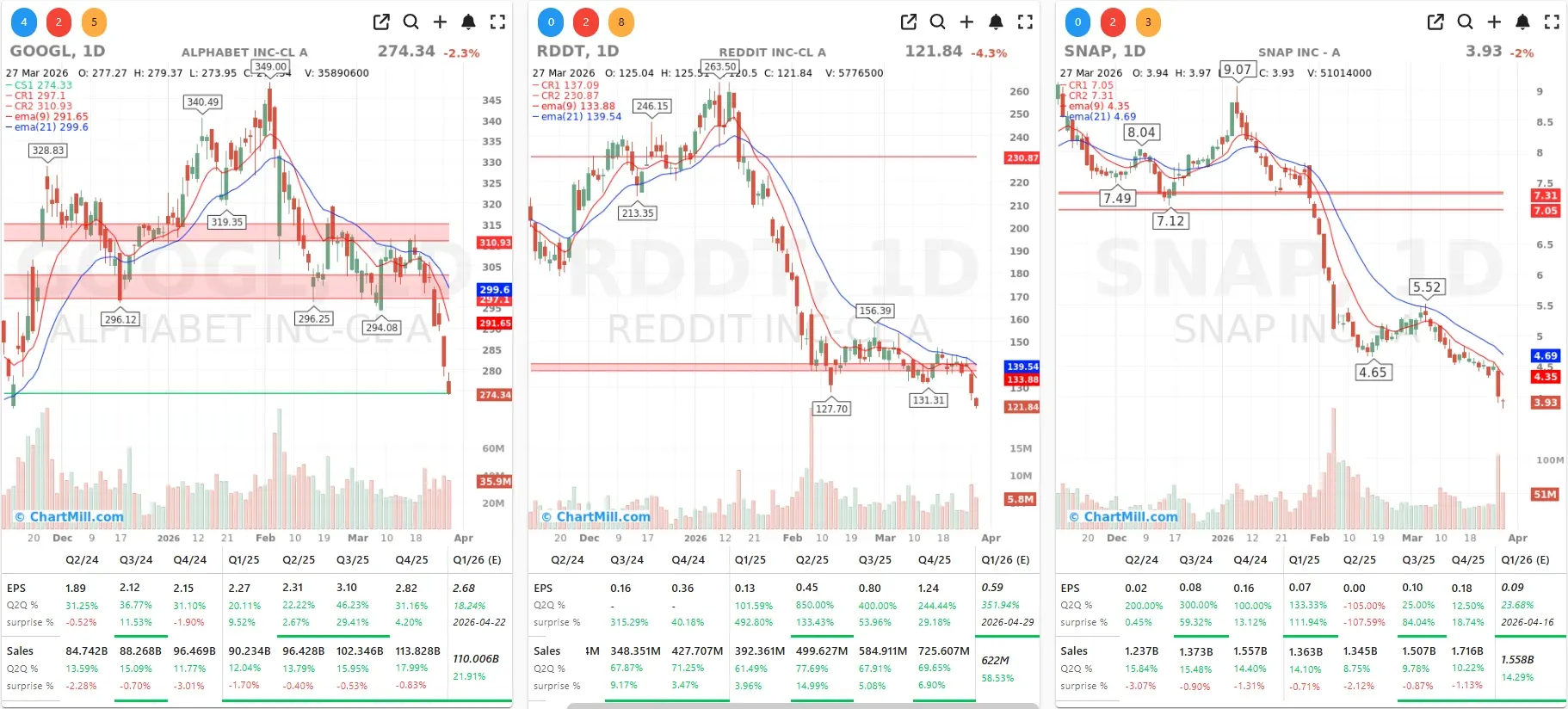

Meta: A Legal Reckoning Two Courts in the Making

Meta Platforms (META | ▼3.99%) has had one of the worst weeks in recent memory, and Friday's 4% decline came on top of an 8% drop Thursday. The trigger: back-to-back courtroom defeats that have fundamentally reframed how legal liability around social media and minors is understood.

A New Mexico state court jury ordered Meta to pay $375 million in civil damages after finding the company failed to protect children from sexual predators on Facebook and Instagram. Simultaneously, a separate jury in Los Angeles found Meta and YouTube negligent for designing platforms that harmed a young woman's mental health through addictive features.

New Mexico's attorney general noted there is a distinct possibility these verdicts will push Congress to reexamine Section 230 of the Communications Decency Act, the shield that has long protected platforms from liability for user-generated content.

The financial penalties themselves are, frankly, rounding errors for a $1.5 trillion company. But what ratlles the market is the litigation pipeline behind these verdicts.

More than 40 state attorneys general have filed lawsuits against Meta, claiming it is contributing to a mental health crisis among young people, and thousands of individual cases are pending. The bellwether has spoken.

Alphabet (GOOGL | ▼2.34) also took a hit given its YouTube exposure to the Los Angeles verdict, while Reddit (RDDT | ▼4.26%) and Snap (SNAP | ▼2%) were dragged lower by sector contagion.

A Rare Bright Spot: Spirits Giants in Merger Talks

Brown-Forman (BF.B | ▲5.63%), the maker of Jack Daniel's, ended meaningfully higher after confirming it is in discussions with French spirits giant Pernod Ricard over a potential business combination.

Both companies have described the potential tie-up as a "merger of equals", a deal that would unite the world's second-largest spirits maker with the largest producer of American whiskey. The move comes as spirits companies broadly battle a multi-year sales slump amid slowing demand and tariff pressures, which has triggered a slide in valuations and a wave of cost-cutting across the industry.

No terms have been agreed, and no assurances have been given that a deal will close, but the strategic logic of combining Jack Daniel's and Woodford Reserve with Absolut, Jameson, and Chivas Regal is hard to ignore.

Energy Winners and the Gold Revival

On the other side of the ledger, the oil majors did what they always do in this environment: Chevron (CVX | ▲1.62%) and Exxon Mobil (XOM | ▲3.36%) both climbed as crude prices surged.

And in a welcome development for those who've been asking "where's the safe haven?", gold finally stepped up. The gold price rose more than 3% to around $4,500 per troy ounce, while U.S. Treasury yields remained broadly unchanged and the euro/dollar pair traded around 1.1516.

Gold miners like Agnico Eagle (AEM | ▲3.11%) benefited accordingly.

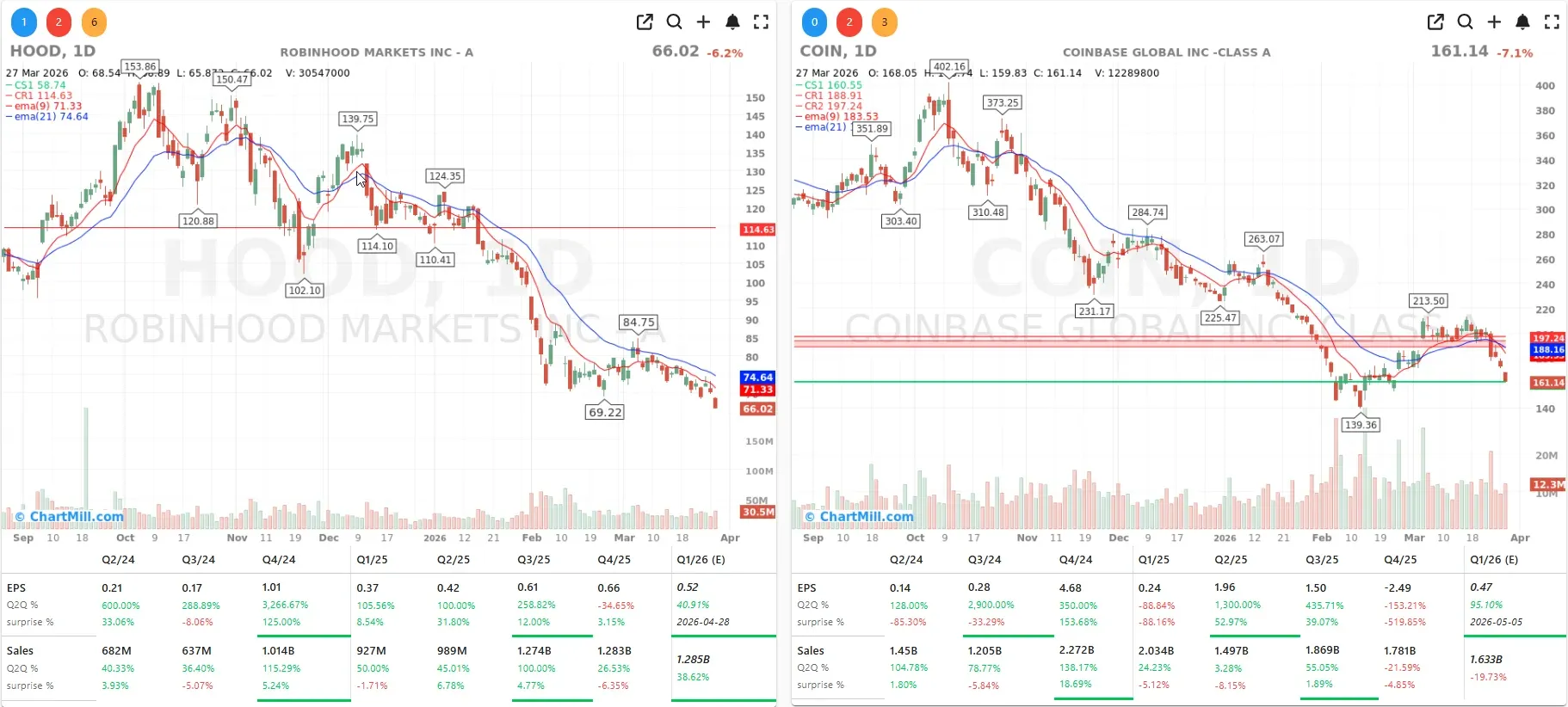

Bitcoin, meanwhile, had a rough Friday, falling below $66,000 as crypto-linked names Coinbase (COIN | ▼7.06%) and Robinhood (HOOD | ▼6.15%) tracked the broader risk-off move lower.

Consumer Sentiment: The Pressure Is Building

The University of Michigan's consumer confidence reading for the US declined on Friday, while inflation expectations rose from 3.4% to 3.8%. That combination, falling confidence and rising inflation expectations, iis the kind of data point that makes the Fed's job considerably harder and gives equity bulls very little to work with heading into the new week.

Conclusion

Going into Monday, the tape is unambiguous: this market is in a corrective phase driven by a war that shows no clear end, energy prices that are tightening like a vice on corporate margins, and a legal environment that is finally starting to impose real costs on Big Tech's approach to platform safety.

The Anthropic Mythos story is a wildcard worth monitoring closely, if the cybersecurity fears around that model prove substantive, the pressure on security sector valuations could intensify further.

The only meaningful green shoots I see are in energy, gold, and the occasional M&A story like Brown-Forman. For now, defense remains the name of the game.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Breakdown Deepens as Weekly Downtrends Confirm