The investment philosophy of Peter Lynch, the former manager of the Fidelity Magellan Fund, focuses on finding good growth companies available at fair prices—a method called Growth at a Reasonable Price (GARP). Lynch supported investing in businesses that are easy to understand, have solid basics, steady earnings increases, and good financial condition, while staying away from prices that are too high. His approach, described in his book One Up on Wall Street, employs a group of number-based filters to find these companies, looking at maintainable earnings increases, profit generation, balance sheet soundness, and a good price when growth is considered. A recent filter using these ideas has pointed to WILLIAMS-SONOMA INC (NYSE:WSM) as a possible choice for long-term investors using this method.

Matching the Lynch Standards

Williams-Sonoma seems to fit well with a number of important filters in a Peter Lynch-style screen. The method stresses companies increasing at a maintainable rate, not at speeds that are difficult to continue. It also requires financial soundness and profit generation, confirming the business is on a firm base. Lastly, it needs the stock's price to be fair compared to its growth potential. Here is how WSM compares to these particular Lynch standards:

- Maintainable Earnings Growth: A central Lynch standard is a 5-year earnings per share (EPS) increase rate between 15% and 30%. Williams-Sonoma's EPS has increased at an average yearly rate of about 29.3% over the last five years. This puts it at the high end of Lynch's chosen range, showing solid, but not unsustainably fast, past growth.

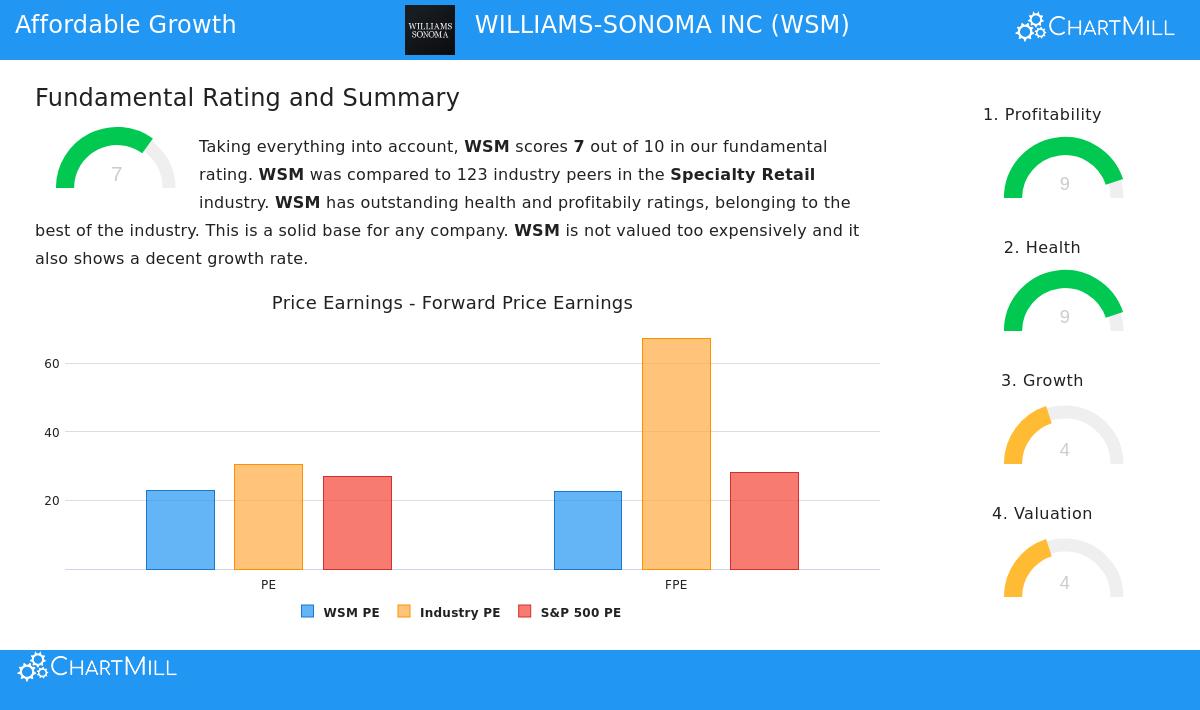

- Fair Price (PEG Ratio): Lynch was known for using the Price/Earnings to Growth (PEG) ratio to find stocks that might be priced low for their increase rate, choosing a PEG of 1 or lower. With a PEG ratio of 0.79, WSM trades at a price Lynch would see as fair, as the P/E ratio is not exceeding the company's past earnings growth.

- Strong Profit Generation (Return on Equity): Lynch searched for companies that effectively produce profits from shareholder equity, with an ROE above 15% being a good sign. Williams-Sonoma's ROE of 53.4% is very high, well past this level and showing very effective use of investor money.

- Financial Soundness (Debt/Equity & Current Ratio): A careful balance sheet was key for Lynch. He chose a Debt/Equity ratio below 0.6, and preferably under 0.25. WSM's Debt/Equity ratio is 0.0, meaning it functions with no interest-bearing debt, which is a very strong financial state. Also, its Current Ratio of 1.43 meets Lynch's need of being at least 1, indicating enough cash to meet near-term needs.

Basic Soundness and Quality

Beyond the specific filter numbers, a wider view of Williams-Sonoma's basics supports the argument for its quality. The company's basic analysis report gives it a high total score of 7 out of 10, with special force in profit generation and financial soundness.

The profit generation picture is excellent, with top-level margins and returns. The company's operating margin over 18% and profit margin close to 14% place in the best group of its specialty retail competitors. Its Return on Invested Capital (ROIC) over 31% further shows very good capital use effectiveness.

Financially, the company is on very firm ground. The lack of debt removes failure risk and gives important operational room. While some cash ratios are seen as middle level, the overall force of the balance sheet and cash flows lessens worries. The company also has a record of giving money back to shareholders through a steady, increasing dividend and stock buybacks—another trait Lynch liked.

Growth at a Reasonable Price View

For GARP investors, the meeting point of quality, growth, and price is most important. Williams-Sonoma shows a strong profile: it has provided top-level profit generation and solid past earnings growth while keeping a clean balance sheet. The present price, as shown by the below-1 PEG ratio, suggests the market may not be completely valuing this quality-growth mix, especially next to industry averages. While future growth expectations are more measured than the past five years, the company's strong brand group—including Pottery Barn and West Elm—and its leading omnichannel retail place give a base for continued, stable growth.

Locating More Choices

The Peter Lynch method is made to find companies with lasting competitive edges trading at fair prices. Williams-Sonoma acts as a clear example of the kind of business this screen tries to find. Investors wanting to look at other companies that pass similar basic filters can see the complete Peter Lynch Strategy screen results here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. The study is based on data and a set screening method; it does not look at personal investment goals or money situations. Investors should do their own complete research and talk with a qualified financial advisor before making any investment choices.