For investors looking for a disciplined, long-term way to build wealth, few strategies are as respected as Peter Lynch’s method. The famous manager of the Fidelity Magellan Fund supported investing in what you understand, concentrating on companies with clear operations, lasting growth, and fair prices. His thinking, often called Growth at a Reasonable Price (GARP), avoids speculative trends and looks for firms increasing steadily while keeping sound finances. A filter using Lynch’s main ideas recently found one notable choice in the specialty retail sector: WILLIAMS-SONOMA INC (NYSE:WSM).

A Lynch-Type Profile: Lasting Growth and Financial Strength

Peter Lynch valued companies that increased earnings at a good, but not extreme, rate, usually between 15% and 30% each year over five years. He believed growth above that level was frequently not lasting. Williams-Sonoma’s history matches this view well. The company has reached a notable five-year earnings per share (EPS) growth rate of about 29.3%, sitting at the higher end of Lynch’s lasting range. This points to a solid, yet possibly repeatable, rise in profit. For a GARP investor, this past growth is the starting point, implying the company has done well with its plan in the home goods market.

Importantly, Lynch stated that growth must not be too expensive. His favored gauge to check this was the Price/Earnings to Growth (PEG) ratio, where a number at or under 1 implies a stock could be fairly valued compared to its growth. Williams-Sonoma does well here, with a PEG ratio from its five-year growth near 0.67. This measure is important to the Lynch method as it connects price directly to the company’s shown growth path, suggesting the market may not completely value WSM’s past results.

Looking at the Financial Foundation

Beyond growth and price, Lynch focused heavily on a company’s financial soundness and operational quality. He preferred businesses with little debt, good cash positions, and high returns on shareholder equity.

- Strong Balance Sheet: Williams-Sonoma runs with zero debt on its books, leading to a Debt/Equity ratio of 0.0. This is much better than Lynch’s liking for a ratio under 0.6 and even his tighter goal of 0.25. Having no debt offers great stability, lowering risk in weak economies and giving the company options to spend, improve, or give money back to shareholders.

- High Profitability: The company’s Return on Equity (ROE) is a notable 53.4%, well above Lynch’s 15% minimum. This shows management is very good at creating earnings from the money shareholders have provided.

- Sufficient Liquidity: With a Current Ratio of 1.43, the company meets Lynch’s need for a figure above 1.0, proving it has enough short-term assets to meet its near-term bills, a simple test of financial condition.

Broad Fundamental Review

An examination of Williams-Sonoma’s wider fundamental report supports the view from the Lynch filter. The company gets a good total score, led by high marks in profitability and financial soundness.

- Profitability is a major positive, with top-tier margins and returns on assets and capital. This matches Lynch’s interest in financially sound companies.

- Financial Soundness is solid, emphasized by the no-debt position and a good Altman-Z score, pointing to very little risk of failure.

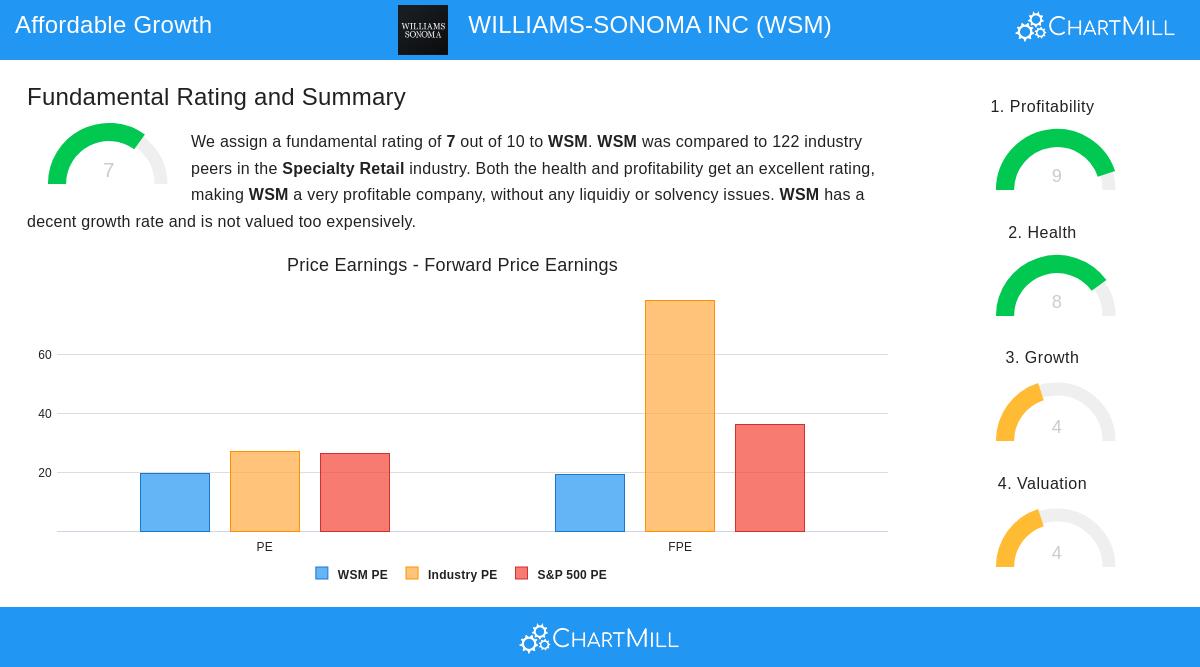

- Price looks fair compared to both its industry group and the wider S&P 500, particularly when its better profitability is noted. This backs the good PEG ratio finding.

- Growth displays a strong history but forecasts for coming years are more measured. This slowing in expected growth is something for investors to examine, as the Lynch method depends on the continuation of lasting growth. The main question is if the company can keep a high, even if somewhat reduced, growth rate in the future.

For a complete look at these figures, you can see the full fundamental analysis report for WSM here.

Final Thoughts and Next Steps

Williams-Sonoma makes a strong argument for investors who follow the Peter Lynch GARP thinking. It shows a record of good, lasting earnings growth, is priced fairly when that growth is considered (PEG < 1), and has a very strong balance sheet with no debt and high profit. While future growth projections indicate a slower speed, the company’s well-known brands, operational skill, and financial control offer a firm base for long-term wealth building.

The Lynch method is about finding more chances like this. If you want to find other companies that meet similar checks for lasting growth, fair price, and financial soundness, you can review the present results of the Peter Lynch Strategy stock screen.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of your original investment. You should do your own research and talk to a qualified financial advisor before making any investment choices.