For investors looking to balance the search for growth with a degree of caution, the "Growth at a Reasonable Price" (GARP) method presents a viable middle path. This method tries to find companies that are increasing at a rate above the average but whose stock prices are not at extreme levels. It avoids the limits of pure, often costly, momentum stocks and deep-value stocks that might not have growth drivers. By concentrating on businesses with good fundamentals, including consistent profitability and a sound financial state, the method tries to reduce risk while taking part in a company's progress. One stock that recently appeared from this type of filtering process is Workday Inc-Class A (NASDAQ:WDAY), a top supplier of enterprise cloud applications for finance and human resources.

Growth Path and Momentum

The central idea of any affordable growth method is, expectedly, growth. Workday displays a good history and positive near-term movement here. The company's fundamental report shows a ChartMill Growth Rating of 7 out of 10, signaling good performance compared to other software industry companies. This score is supported by notable past numbers and good future forecasts.

- Past Performance: In the last year, Workday increased its Earnings Per Share (EPS) by 26.44%, while revenue rose by 13.09%. The five-year average yearly EPS growth is a very good 26.32%, with revenue increasing at an average of 17.21% each year over the same time.

- Future Forecasts: Analysts predict this growth will persist, though at a slower speed. The EPS is predicted to grow by an average of 10.94% each year in the next few years, with revenue estimated to rise by 10.75% yearly. While this is a slowdown from the high past rates, it remains a sound and above-average growth view that creates a believable foundation for future valuation.

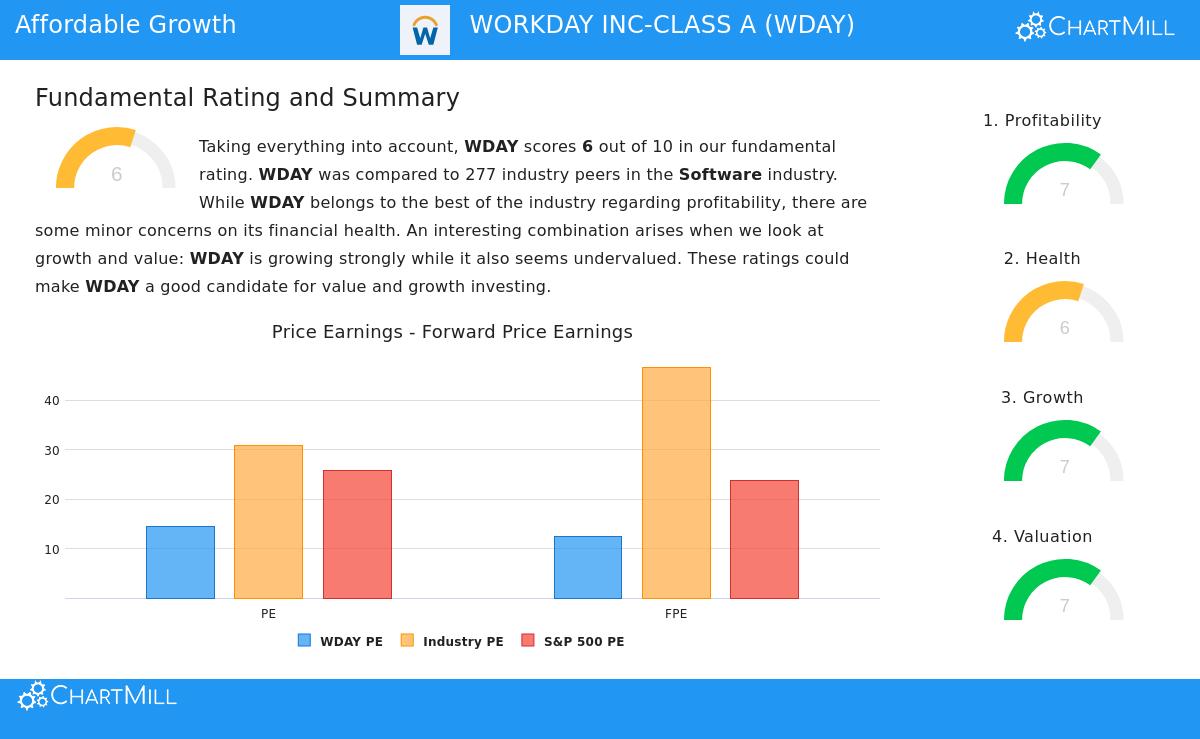

Valuation: The "Reasonable Price" Idea

A stock cannot be seen as "affordable growth" if its valuation is high. This is where Workday offers an interesting situation. The company receives a ChartMill Valuation Rating of 7, hinting its current share price may not completely account for its growth and profit profile when measured against the wider market and its industry.

- Good Multiples: Workday's Price-to-Earnings (P/E) ratio of 14.53 is significantly below the industry average of about 30.8. This means more than 81% of its software industry peers trade at a higher earnings multiple. Its forward P/E ratio of 12.49 is also lower than the industry and the wider S&P 500.

- Cash Flow and EBITDA: The valuation picture goes beyond earnings. Judging by its Price-to-Free Cash Flow and Enterprise Value-to-EBITDA ratios, Workday is priced more affordably than about 84% of its industry rivals. This suggests the market might be using a cautious view, possibly opening a chance for investors who trust the strength of its business model.

Supporting Fundamentals: Profitability and Financial State

For a GARP investment to last, growth must be supported by reliable operations and a firm balance sheet. Workday's scores in profitability and financial condition give this important support.

- Good Profitability (Rating: 7): The company is very profitable, with main measures doing better than most competitors. Its Return on Invested Capital (ROIC) of 10.27% is very good, putting it in the top 14% of the industry. Both its operating margin (16.64%) and profit margin (13.19%) are solid, showing efficient management and pricing ability.

- Acceptable Financial State (Rating: 6): Workday's financial position is firm, with some small points to observe. Its solvency is a positive, with a very low debt-to-free-cash-flow ratio of 1.08, meaning it could pay off all debt in just over a year from its cash flow. While its Altman-Z score and current ratio are acceptable, the report mentions that its return on invested capital is now below its cost of capital, an area for management to improve to increase shareholder value creation.

Conclusion and Additional Study

Workday Inc. shows the kind of company an affordable growth filter aims to find: one with a clear history of good growth, a fair valuation compared to that growth, and the fundamental profitability and financial condition to back its future goals. The mix of double-digit revenue growth forecasts, industry-leading profitability margins, and a valuation that is below sector averages makes WDAY a notable option for investors using a GARP method.

It is vital to recall that filtering is a first step for more detailed study. Elements like competitive forces in the enterprise software market, performance on future growth plans, and wider economic factors affecting IT spending should all be reviewed. For a complete look at all fundamental measures, you can see the full fundamental analysis report for Workday.

If you want to find other businesses that match this description, you can see the complete list of results from the "Affordable Growth" filter here.

Disclaimer: This article is for information only and is not financial advice, a suggestion, or an offer to buy or sell any security. Investing has risk, including the possible loss of principal. You should do your own study and talk with a qualified financial advisor before making any investment choices.