The search for growth stocks at reasonable prices is a foundation of many investment plans, trying to gain the upside of developing companies without paying too much. One way to find these chances is through an "Affordable Growth" screening process, which looks for companies with solid growth paths while also having good fundamental condition, acceptable profitability, and a valuation that is not extreme. This even-handed method tries to lower risk by steering clear of companies where future growth is already completely reflected in the stock price, concentrating on those where the basics support more increase. Workday Inc-Class A (NASDAQ:WDAY) appears as a candidate from such a filter, justifying a more detailed look at its investment characteristics.

Growth Path

A main need for an affordable growth stock is a clearly solid and maintainable growth model. Workday's fundamentals show a company in a strong development stage, which is important for pushing future earnings and, as a result, share price movement.

- Historical Performance: The company has produced notable historical growth, with Earnings Per Share (EPS) increasing at an average pace of 30.89% over recent years and Revenue increasing at an average of 18.42%.

- Recent Momentum: This solid historical pattern is backed by recent results, including a 25.19% EPS increase and a 13.94% Revenue increase over the last year.

- Future Expectations: Analyst projections indicate a continued, though somewhat slower, solid growth direction, with EPS anticipated to increase at 17.80% and Revenue at 12.58% on an annualized basis moving ahead.

This steady history of top-line and bottom-line growth is precisely what growth investors look for. While future growth rates are forecast to be less than the outstanding historical speed, they stay firmly in the "quite solid" group, indicating the company's growth driver is still operating well.

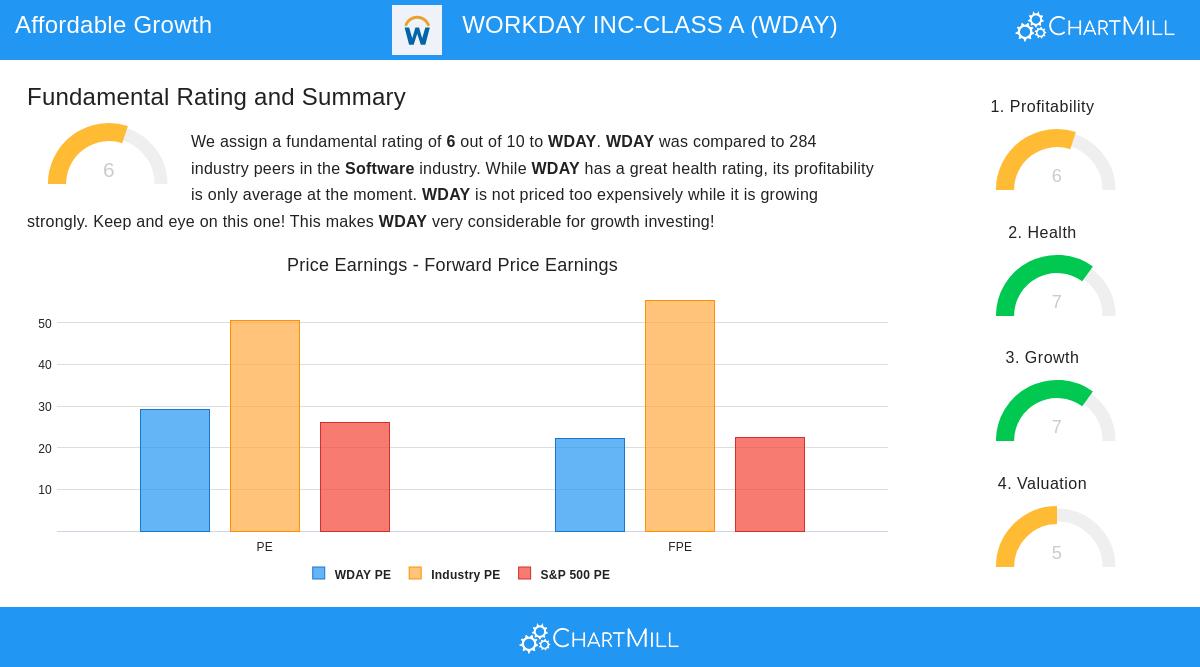

Valuation Check

For a stock to be seen as "affordable," its valuation should not be extreme compared to its growth possibilities and the wider market. Workday shows a varied but finally acceptable valuation image when viewed inside its industry and growth outline.

- Absolute vs. Relative Metrics: Workday's Price/Earnings (P/E) ratio of 29.08 seems high on its own and is a bit above the S&P 500 average. However, measured against its peers in the software industry, where average P/E ratios are much higher, Workday is less expensive than about 68% of the industry.

- Cash Flow and EBITDA: The valuation seems more attractive through other views. Judging by its Enterprise Value to EBITDA and Price/Free Cash Flow ratios, Workday is more affordable than 66% and 75% of its industry rivals, in that order.

- Growth Compensation: The Price/Earnings to Growth (PEG) ratio, which changes the P/E for projected earnings growth, shows a fair valuation. This implies that the present share price suitably mirrors the company's solid growth projections.

This valuation outline is key to the affordable growth idea. Investors are not paying extra for growth without condition but are getting a high-growth company at a valuation that is sensible within its field.

Financial Condition and Profitability

The affordable growth plan also requires that companies are established on a steady base, making sure they can endure economic changes and keep putting money into growth. Workday's financial condition and profitability marks give this vital support.

The company displays a solid financial condition picture, marked by high liquidity and solvency. Its Current and Quick Ratios are both at 2.10, showing more than enough means to cover short-term debts and doing better than most software industry friends. Also, its debt level is not a problem, with a low Debt-to-Free Cash Flow ratio of 1.25, indicating a solid ability to pay back debts fast.

On the profitability side, Workday shows acceptable and getting better measures. The company is profitable and creates positive operating cash flow. Its margins are especially notable, with a Gross Margin of 75.58% and an Operating Margin of 8.58%, both of which put it in the leading group of its industry. While its Return on Equity and Return on Assets are acceptable, the solid and industry-leading margins supply a high-quality earnings foundation from which future growth can be paid for.

Summary

Workday Inc. represents the features wanted by the affordable growth filtering technique. It matches a great, provable growth history with a valuation that, while not cheap, is sensible within its high-achieving sector. This pairing is supported by a solid financial condition mark and good profitability margins, lessening the operational dangers linked to its growth goals. For investors looking for companies with the possibility for continued development without extreme costs, Workday offers an attractive case for more study.

For investors curious about finding other companies that match this outline, our pre-set Affordable Growth screen can be used to find more possible chances. A more complete fundamental analysis of Workday is ready in its full fundamental report.

Disclaimer: This article is for informational purposes only and does not constitute financial advice, a recommendation, or an offer or solicitation to buy or sell any securities. The content presented is based on data believed to be reliable but is not guaranteed as to accuracy or completeness. Investors should conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.